It has been called the largest financial scandal in history, a web of alleged white-collar malfeasance spanning several continents while hitting portfolios and pocketbooks from Wall Street to Main Street.

But U.S. prosecutors may be hesitant to launch criminal proceedings against large financial institutions for alleged manipulation of the Libor, a key interbank borrowing rate that affects an estimated $360 trillion in financial contracts worldwide, economists and securities experts say.

Ever since the crash of Lehman Brothers four years ago prompted the U.S. government to rescue the country’s largest financial institutions with taxpayer money, U.S. authorities are hesitant to “do something that might make one of these banks fail,” said Stephen Bainbridge, a securities regulation expert at UCLA Law School.

All eyes in the financial world on Friday will be trained on London, where Martin Wheatley, Britain’s top financial regulator, is set to issue recommendations for regulatory reforms to prevent manipulation of the Libor, which is used by lenders to set interest rates for all manner of investments, from municipal bonds to mortgages to credit cards.

“Anybody who has any investment in financial markets has been affected by the Libor fraud,” Bainbridge said. “Over half of the American population own stocks—whether directly or through a mutual fund—so it has affected most people.”

The London Interbank Offered Rate, or Libor, is the average interest rate at which top banks estimate they would borrow money from other banks. This rate, which is adjusted daily, is used as the benchmark used to set interest rates for a wide range of financial products and commercial markets across the globe.

Wheatley’s announcement comes after months of allegations, resignations, and lurid evidence pointing at possible collusion among the banks to manipulate the rate in order benefit their trading arms.

British bank Barclays in June admitted that its traders had encouraged the bank to rig the rate in order to benefit their financial positions, paying a $470 million fine to U.S. and British authorities to settle the charges.

Wheatley’s report Friday is unlikely to include scores of smoking guns pointing to such collusion, but if it does contain instances of “trader-to-trader contact in which one is asking the other to help him push Libor up or down, that would be of great interest to U.S. criminal authorities,” said John Coffee, a prominent securities law expert at Columbia Law School.

The 18 banks that set the Libor for the U.S. dollar include financial behemoths such as Bank of America, Citibank, JP Morgan Chase, and Deutsche Bank.

Should evidence of collusion to rig rates at these institutions emerge, the U.S. Justice Department may target individual executives for criminal prosecution rather than go after the financial entity itself, said Robert Shapiro, a former undersecretary of commerce for economic affairs under the administration of U.S. President Bill Clinton.

“So far the Justice Department has not been willing to put any of the large financial institutions in that particular box,” Shapiro said. “I’d be surprised.”

Opting to forgo criminal prosecution if there is clear evidence of wrongdoing risks sending a “wrong signal that if an institution is large enough, and important enough, it’s not going to be criminally charged,” said Rosa M. Abrantes-Metz, a financial regulation expert with Global Economics Group in New York City and an adjunct associate professor at New York University’s Leonard N. Stern School of Business.

But “criminally charging institutions, particularly in the financial sector—given the instability there—can be very complicated,” she said.

Even in the absence of criminal charges, the largest U.S. financial players face a possible avalanche of civil litigation over the Libor-rigging accusations.

In July, New York-based Berkshire Bank filed a complaint in federal court against more than a dozen banks in connection with the allegations, citing the “tens, if not hundreds, of billions of dollars of loans” that “are originated or sold within this state each year with rates tied to Libor.”

Dozens of other suits have been filed in the United States in connection with the alleged rate-fixing. Plaintiffs in these cases, however, will have to do the math on whether the eventual payoff is worth the effort.

The banks involved in setting Libor “have enormous resources to fight these suits,” Shapiro said.

Source

DAILY BUSINESS REPORT - Financial Updates, International Markets and Business News

September 28, 2012

September 27, 2012

RBS traders boasted of Libor 'cartel'

Senior traders at Royal Bank of Scotland boasted about operating a “cartel” that made “amazing” amounts of money by rigging interest rates, it has been disclosed.

Internal messages revealed in court documents apparently show how traders claimed they could manipulate Libor, which is used to set borrowing costs for millions of businesses, consumers and investors.

The messages, some sent just months before the taxpayer was forced to bail out RBS at a cost of more than £40bn, suggest the practice was condoned and encouraged by senior executives at the bank, and have now dragged the taxpayer-backed lender to the heart of the Libor scandal.

MPs have warned that the scale of RBS’s involvement in the scandal means it could face an even bigger fine than Barclays, which paid a record £290m in July after admitting attempting to manipulate Libor. The bank could also be hit with billions of pounds in damages claims.

Tan Chi Min, a former senior trader at RBS’s global banking and markets division in Singapore, has alleged that managers “condoned collusion” between staff to maximise profits by rigging Libor.

Mr Tan, who worked for RBS from August 2006 to November 2011, was eventually sacked for gross misconduct, but claims the bank made him a “scapegoat” for malpractice condoned by managers.

Internal messages revealed in court documents apparently show how traders claimed they could manipulate Libor, which is used to set borrowing costs for millions of businesses, consumers and investors.

The messages, some sent just months before the taxpayer was forced to bail out RBS at a cost of more than £40bn, suggest the practice was condoned and encouraged by senior executives at the bank, and have now dragged the taxpayer-backed lender to the heart of the Libor scandal.

MPs have warned that the scale of RBS’s involvement in the scandal means it could face an even bigger fine than Barclays, which paid a record £290m in July after admitting attempting to manipulate Libor. The bank could also be hit with billions of pounds in damages claims.

Tan Chi Min, a former senior trader at RBS’s global banking and markets division in Singapore, has alleged that managers “condoned collusion” between staff to maximise profits by rigging Libor.

Mr Tan, who worked for RBS from August 2006 to November 2011, was eventually sacked for gross misconduct, but claims the bank made him a “scapegoat” for malpractice condoned by managers.

September 26, 2012

QE4? The Big Wall Street Banks Are Already Complaining That QE3 Is Not Enough

QE3 has barely even started and some folks on Wall Street are already clamoring for QE4. In fact, as you will read below, one equity strategist at Morgan Stanley says that he would not be "surprised" if the Federal Reserve announced another new round of money printing by the end of the year. But this is what tends to happen when a financial system starts becoming addicted to easy money. There is always a deep hunger for another "hit" of "currency meth". Federal Reserve Chairman Ben Bernanke was probably hoping that QE3 would satisfy the wolves on Wall Street for a while. His promise to recklessly print 40 billion dollars a month and use it to buy mortgage-backed securities is being called "QEInfinity" by detractors. During QE3, nearly half a trillion dollars a year will be added to the financial system until the Fed decides that it is time to stop. This is so crazy that even former Federal Reserve officials are speaking out against it. For example, former Federal Reserve chairman Paul Volcker says that QE3 is the "most extreme easing of monetary policy" that he could ever remember. But the big Wall Street banks are never going to be satisfied. If QE4 is announced, they will start calling for QE5. As I noted in a previous article, quantitative easing tends to pump up the prices of financial assets such as stocks and commodities, and that is very good for Wall Street bankers. So of course they want more quantitative easing. They always want bigger profits and bigger bonus checks at the end of the year.

But at this point the Federal Reserve has already "jumped the shark". If you don't know what "jumping the shark" means, you can find a definition on Wikipedia right here. Whatever shreds of credibility the Fed had left are being washed away by a flood of newly printed money.

Those running the Fed have essentially used up all of their bullets and the next great financial crisis has not even fully erupted yet.

So what is the Fed going to do if the stock market crashes and the credit market freezes up like we saw back in 2008?

How much more extreme can the Fed go?

One can just picture "Helicopter Ben" strapping on a pair of water skis and making the following promise....

"We are going to print so much money that we'll make Zimbabwe and the Weimar Republic look like wimps!"

Sadly, the truth is that money printing is not a "quick fix" and it never has been. Just look at Japan. The Bank of Japan is on round 8 of their quantitative easing strategy, and yet things in Japan continue to get even worse.

But that is not going to stop the folks on Wall Street from calling for even more quantitative easing.

For example, the top U.S. equity strategist for Morgan Stanley, Adam Parker, made headlines all over the world this week by writing the following....

"QE3 will likely be insufficient to significantly boost equity markets and we wouldn’t be at all surprised to see the Fed dramatically augment this program (i.e., QE4) before year-end, particularly if economic and corporate news continue to deteriorate as they have over the past few weeks." Did you get what he is saying there?

He says that QE3 is not going to be enough to boost equity markets (the stock market) so more money printing will be necessary.

But wasn't QE3 supposed to be about creating jobs and helping the middle class?

I can almost hear many of you laughing out loud already.

As I have written about before, QE3 is unlikely to change the employment picture in any significant way, but what it will do is create more inflation which will squeeze the poor, the middle class and the elderly.

The truth is that quantitative easing has always been about bailing out the banks, and the hope is that this will trickle down to the folks on Main Street as well, but that never seems to happen.

Wall Street is not calling for even more quantitative easing because it would be good for you and I. Rather, Wall Street is calling for even more quantitative easing because it would be good for them.

A CNBC article entitled "Fed May Need to Boost QE 'Dramatically' This Year: Pros" discussed Wall Street's desire for even more money printing....

The Federal Reserve's latest easing move has been nicknamed everything from "QE3" to "QE Infinity" to "QEternal," but some on Wall Street question whether the unprecedented move will be QEnough.

And of course everyone pretty much understands that QE3 is definitely not going to fix our economic problems. Even most of those on Wall Street will admit as much. In the CNBC article mentioned above, a couple of economists named Paul Ashworth and Paul Dales at Capital Economics were quoted as saying the following....

"The Fed can commit to deliver whatever economic outcome it likes, but the problem is that the crisis in the euro-zone and/or a stand-off in negotiations to avert the fiscal cliff in the U.S. may well reveal it to be like the proverbial Emperor with no clothes"

An emperor with no clothes?

I think the analogy fits.

The Federal Reserve is going to keep printing and printing and printing and things are not going to get any better.

At this point, economists at Goldman Sachs are already projecting that QE3 will likely stretch into 2015....

The Federal Reserve's QE3 bond buying program announced earlier this month could last until the middle of 2015 and eventually reach $2 trillion, according to an estimate from economists at Goldman Sachs.

The Goldman economists also wrote in a report that they believe the Fed will not raise the federal funds rate until 2016. This rate, which is used as a benchmark for a wide variety of consumer and business loans, has been near 0% since December 2008. The Fed said in its last statement that it expected rates would remain low until mid-2015. So why is Wall Street whining and complaining so loudly right now?

Well, even with all of the bailouts and even with all of the help from the first two rounds of quantitative easing, things are still tough for them.

For example, Bank of America recently announced that they will be laying off 16,000 workers.

In addition, there are rumors that 100 highly paid partners at Goldman Sachs are going to be getting the axe. It is said that Goldman will save 2 billion dollars with such a move.

We haven't even reached the next great financial crisis and the pink slips are already flying on Wall Street. Meredith Whitney says that she has never seen anything quite like this....

"The industry is as bad as I've seen it. So it's certainly not a great time to be on Wall Street."

But of course Wall Street is not going to get much sympathy from the rest of America. The truth is that things have been far rougher for most of the rest of us than things have been for them.

When the last crisis hit, they got trillions of dollars in bailout money and we got nothing.

So most people are not really in a mood to shed any tears for Wall Street.

But of course the Federal Reserve is definitely hoping to help their friends on Wall Street out by printing lots of money.

You never know, by the time this is all over we may see QE4, QE5, QE Reloaded, QE With A Vengeance and QE The Return Of The Bernanke.

Meanwhile, Europe is gearing up to print money like crazy too.

A couple months ago, European Central Bank President Mario Draghi made the following pledge....

"Within our mandate, the European Central Bank is ready to do whatever it takes to preserve the euro, and believe me, it will be enough." And of course the Bank of Japan has joined the money printing party too. The following is from a recent article by David Kotok....

The recently announced additional program by the BOJ includes a fifty-percent allocation to the purchase of ten-year Japanese government bonds. The other fifty percent will buy shorter-term government securities. Thus, the BOJ is applying half of its additional QE stimulus to extracting long duration from the government bond market, denominated in Japanese yen.

All of the central banks seem to be getting on the QE bandwagon.

But will this fix anything?

Unfortunately it will not, at least according to Paul Volcker....

“Another round of QE is understandable – but it will fail to fix the problem. There is so much liquidity in the market that adding more is not going to change the economy.” Sadly, most Americans have a ton of faith in the people running our system, but the truth is that they really do not know what they are doing. Just check out what Dallas Fed President Richard Fisher said the other day....

"The truth, however, is that nobody on the committee, nor on our staffs at the Board of Governors and the 12 Banks, really knows what is holding back the economy. Nobody really knows what will work to get the economy back on course. And nobody – in fact, no central bank anywhere on the planet – has the experience of successfully navigating a return home from the place in which we now find ourselves. No central bank – not, at least, the Federal Reserve – has ever been on this cruise before." Can you imagine the head coach of a football team coming in at halftime and telling his players the following....

"Nobody on the coaching stuff really has any idea what will work."

That sure would not inspire a lot of confidence, would it?

Perhaps the Fed should be open to some input from the rest of us.

Actually, back on September 14th the Federal Reserve Bank of San Francisco posted a poll on Facebook that asked the following question....

What effect do you think QE3 will have on the U.S. economy?

The following are the 5 answers that got the most votes....

-"Long term, disastrous"

-"Negative"

-"Thanks for $5 gas"

-"I can't believe you think this will work!"

-"Fire Bernanke"

So what do you think about the quantitative easing that the Federal Reserve is doing?

Please feel free to post a comment with your thoughts below....

Read the entire article

But at this point the Federal Reserve has already "jumped the shark". If you don't know what "jumping the shark" means, you can find a definition on Wikipedia right here. Whatever shreds of credibility the Fed had left are being washed away by a flood of newly printed money.

Those running the Fed have essentially used up all of their bullets and the next great financial crisis has not even fully erupted yet.

So what is the Fed going to do if the stock market crashes and the credit market freezes up like we saw back in 2008?

How much more extreme can the Fed go?

One can just picture "Helicopter Ben" strapping on a pair of water skis and making the following promise....

"We are going to print so much money that we'll make Zimbabwe and the Weimar Republic look like wimps!"

Sadly, the truth is that money printing is not a "quick fix" and it never has been. Just look at Japan. The Bank of Japan is on round 8 of their quantitative easing strategy, and yet things in Japan continue to get even worse.

But that is not going to stop the folks on Wall Street from calling for even more quantitative easing.

For example, the top U.S. equity strategist for Morgan Stanley, Adam Parker, made headlines all over the world this week by writing the following....

"QE3 will likely be insufficient to significantly boost equity markets and we wouldn’t be at all surprised to see the Fed dramatically augment this program (i.e., QE4) before year-end, particularly if economic and corporate news continue to deteriorate as they have over the past few weeks." Did you get what he is saying there?

He says that QE3 is not going to be enough to boost equity markets (the stock market) so more money printing will be necessary.

But wasn't QE3 supposed to be about creating jobs and helping the middle class?

I can almost hear many of you laughing out loud already.

As I have written about before, QE3 is unlikely to change the employment picture in any significant way, but what it will do is create more inflation which will squeeze the poor, the middle class and the elderly.

The truth is that quantitative easing has always been about bailing out the banks, and the hope is that this will trickle down to the folks on Main Street as well, but that never seems to happen.

Wall Street is not calling for even more quantitative easing because it would be good for you and I. Rather, Wall Street is calling for even more quantitative easing because it would be good for them.

A CNBC article entitled "Fed May Need to Boost QE 'Dramatically' This Year: Pros" discussed Wall Street's desire for even more money printing....

The Federal Reserve's latest easing move has been nicknamed everything from "QE3" to "QE Infinity" to "QEternal," but some on Wall Street question whether the unprecedented move will be QEnough.

And of course everyone pretty much understands that QE3 is definitely not going to fix our economic problems. Even most of those on Wall Street will admit as much. In the CNBC article mentioned above, a couple of economists named Paul Ashworth and Paul Dales at Capital Economics were quoted as saying the following....

"The Fed can commit to deliver whatever economic outcome it likes, but the problem is that the crisis in the euro-zone and/or a stand-off in negotiations to avert the fiscal cliff in the U.S. may well reveal it to be like the proverbial Emperor with no clothes"

An emperor with no clothes?

I think the analogy fits.

The Federal Reserve is going to keep printing and printing and printing and things are not going to get any better.

At this point, economists at Goldman Sachs are already projecting that QE3 will likely stretch into 2015....

The Federal Reserve's QE3 bond buying program announced earlier this month could last until the middle of 2015 and eventually reach $2 trillion, according to an estimate from economists at Goldman Sachs.

The Goldman economists also wrote in a report that they believe the Fed will not raise the federal funds rate until 2016. This rate, which is used as a benchmark for a wide variety of consumer and business loans, has been near 0% since December 2008. The Fed said in its last statement that it expected rates would remain low until mid-2015. So why is Wall Street whining and complaining so loudly right now?

Well, even with all of the bailouts and even with all of the help from the first two rounds of quantitative easing, things are still tough for them.

For example, Bank of America recently announced that they will be laying off 16,000 workers.

In addition, there are rumors that 100 highly paid partners at Goldman Sachs are going to be getting the axe. It is said that Goldman will save 2 billion dollars with such a move.

We haven't even reached the next great financial crisis and the pink slips are already flying on Wall Street. Meredith Whitney says that she has never seen anything quite like this....

"The industry is as bad as I've seen it. So it's certainly not a great time to be on Wall Street."

But of course Wall Street is not going to get much sympathy from the rest of America. The truth is that things have been far rougher for most of the rest of us than things have been for them.

When the last crisis hit, they got trillions of dollars in bailout money and we got nothing.

So most people are not really in a mood to shed any tears for Wall Street.

But of course the Federal Reserve is definitely hoping to help their friends on Wall Street out by printing lots of money.

You never know, by the time this is all over we may see QE4, QE5, QE Reloaded, QE With A Vengeance and QE The Return Of The Bernanke.

Meanwhile, Europe is gearing up to print money like crazy too.

A couple months ago, European Central Bank President Mario Draghi made the following pledge....

"Within our mandate, the European Central Bank is ready to do whatever it takes to preserve the euro, and believe me, it will be enough." And of course the Bank of Japan has joined the money printing party too. The following is from a recent article by David Kotok....

The recently announced additional program by the BOJ includes a fifty-percent allocation to the purchase of ten-year Japanese government bonds. The other fifty percent will buy shorter-term government securities. Thus, the BOJ is applying half of its additional QE stimulus to extracting long duration from the government bond market, denominated in Japanese yen.

All of the central banks seem to be getting on the QE bandwagon.

But will this fix anything?

Unfortunately it will not, at least according to Paul Volcker....

“Another round of QE is understandable – but it will fail to fix the problem. There is so much liquidity in the market that adding more is not going to change the economy.” Sadly, most Americans have a ton of faith in the people running our system, but the truth is that they really do not know what they are doing. Just check out what Dallas Fed President Richard Fisher said the other day....

"The truth, however, is that nobody on the committee, nor on our staffs at the Board of Governors and the 12 Banks, really knows what is holding back the economy. Nobody really knows what will work to get the economy back on course. And nobody – in fact, no central bank anywhere on the planet – has the experience of successfully navigating a return home from the place in which we now find ourselves. No central bank – not, at least, the Federal Reserve – has ever been on this cruise before." Can you imagine the head coach of a football team coming in at halftime and telling his players the following....

"Nobody on the coaching stuff really has any idea what will work."

That sure would not inspire a lot of confidence, would it?

Perhaps the Fed should be open to some input from the rest of us.

Actually, back on September 14th the Federal Reserve Bank of San Francisco posted a poll on Facebook that asked the following question....

What effect do you think QE3 will have on the U.S. economy?

The following are the 5 answers that got the most votes....

-"Long term, disastrous"

-"Negative"

-"Thanks for $5 gas"

-"I can't believe you think this will work!"

-"Fire Bernanke"

So what do you think about the quantitative easing that the Federal Reserve is doing?

Please feel free to post a comment with your thoughts below....

Read the entire article

September 25, 2012

Richman v. Goldman Sachs Group: CDOs and Wells Notices

In Richman v. Goldman Sachs Group, Inc., WL 2362539 (S.D.N.Y. June 21, 2012), the court dismissed Plaintiffs' claim regarding Goldman Sachs Group, Inc.’s (“Goldman”) failure to disclose its receipt of Wells Notices but denied Defendants’ motion to dismiss claims pertaining to Goldman’s alleged conflicts of interest in several Collateralized Debt Obligation ("CDOs") placements.

Plaintiffs are purchasers of Goldman's common stock between February 5, 2007 and June 10, 2010 (“Plaintiffs”). Defendants are Goldman Sachs & Co (“Goldman”), Goldman Chairman and CEO Lloyd C. Blankfein, Goldman CFO David Viniar and Goldman COO Gary D. Cohn (“Individual Defendants.”) Plaintiffs claimed that Defendants made misstatements and omissions about Wells Notices the company received from the Securities and Exchange Commission (“SEC”), and about the conflicts of interest arising out of Goldman's role in structuring the CDOs known as Abacus, Hudson Mezzanine Funding ("Hudson"), Anderson Mezzanine Funding ("Anderson") and Timberwolf I.

In the Abacus transaction, for example, Goldman allegedly allowed one of its favored hedge fund clients, Paulson & Co., to select assets for inclusion in the CDO. At the same time, however, Goldman falsely identified ACA Management as the sole portfolio selection agent for the transaction. Goldman also allegedly told investors that it had "aligned itself with the Hudson program by investing in a portion of equity," while at the same time it failed to disclose that it had the entire short position on the deal (in other words, Goldman did not disclose that its $6 million equity holding in the CDO was dwarfed by the $2 billion short position held in it). Plaintiffs also alleged other examples of undisclosed conflicts.

The court found that Plaintiffs plausibly alleged that Goldman made material omissions regarding its arrangement with Paulson & Co. in the Abacus transaction because Defendants "knowingly allowed Paulson to select the assets for the Abacus CDO, and knew that Paulson was selecting assets that it believed would perform poorly or fail." Similarly, the court found that Plaintiffs plausibly alleged that in the Hudson, Anderson, and Timberwolf I CDO transactions, Goldman represented that it held a long position in the equity tranches and did not disclose its substantial short positions. As the court said:

"having allegedly affirmatively represented [Goldman] had a particular investment interest in [these synthetic CDOs]—that it was long—in order to be both accurate and complete, Goldman ... had a duty to disclose [it] had a [greater] investment interest [from its] short [position] ... [because that was] a fact that, if disclosed, would significantly alter the ‘total mix’ of available information."

Finding that Plaintiffs established duty, the court turned to the scienter analysis. Scienter could be inferred when defendants "knew facts or had access to information suggesting that their public statements were not accurate." Here, Defendants allegedly assured shareholders that Goldman complied with the law and that it had "procedures in place to address 'potential conflicts of interest.'" Alternately, Goldman allegedly fostered a conflict of interest in the Abacus CDO and acted against investor interest in Hudson, Anderson and Timberwolf I. The court found that "Goldman knew or should have known that its statements about complying with the letter and spirit of the law, and its disclaimers regarding ‘potential’ conflicts of interest were inaccurate and incomplete." The court agreed with Plaintiffs that a strong inference of scienter could be drawn from Goldman's actions in the four CDO deals.

The court also found that Plaintiffs had sufficiently alleged loss causation and claims against the Individual Defendants. The Individual Defendants allegedly helped prepare the SEC filings at issue. Moreover, scienter was established through allegations that the Individual Defendants actively monitored the status of the relevant CDO assets and were intimately acquainted with the CDO operations.

With respect to the Wells Notices, Goldman, according to Plaintiffs, failed to disclose the receipt of the Wells Notices from the SEC in connection with the investigation of the Abacus transaction. Plaintiffs asserted that Defendants' disclosures about governmental investigations triggered a duty to disclose receipt of Wells Notices, and that by failing to do so caused the public to mistakenly believe that “no significant developments had occurred which made the investigation more likely to result in formal charges." The court noted that the delivery of a Wells Notice, while reflecting the SEC Enforcement Division’s determination on bringing charges, did not necessarily mean that charges would be filed. The court found that failure to disclose receipt of the Wells Notices did not render Goldman’s statement misleading and that Defendants' violation of FINRA's Wells Notice disclosure requirement was not grounds upon which a section 10(b) or Rule 10b-5 claim could be based. The court also rejected the argument that a FINRA rule requiring disclosure of a wells notice triggered a duty to disclose under the antifraud provisions.

The primary materials for this case may be found on the DU Corporate Governance website

Plaintiffs are purchasers of Goldman's common stock between February 5, 2007 and June 10, 2010 (“Plaintiffs”). Defendants are Goldman Sachs & Co (“Goldman”), Goldman Chairman and CEO Lloyd C. Blankfein, Goldman CFO David Viniar and Goldman COO Gary D. Cohn (“Individual Defendants.”) Plaintiffs claimed that Defendants made misstatements and omissions about Wells Notices the company received from the Securities and Exchange Commission (“SEC”), and about the conflicts of interest arising out of Goldman's role in structuring the CDOs known as Abacus, Hudson Mezzanine Funding ("Hudson"), Anderson Mezzanine Funding ("Anderson") and Timberwolf I.

In the Abacus transaction, for example, Goldman allegedly allowed one of its favored hedge fund clients, Paulson & Co., to select assets for inclusion in the CDO. At the same time, however, Goldman falsely identified ACA Management as the sole portfolio selection agent for the transaction. Goldman also allegedly told investors that it had "aligned itself with the Hudson program by investing in a portion of equity," while at the same time it failed to disclose that it had the entire short position on the deal (in other words, Goldman did not disclose that its $6 million equity holding in the CDO was dwarfed by the $2 billion short position held in it). Plaintiffs also alleged other examples of undisclosed conflicts.

The court found that Plaintiffs plausibly alleged that Goldman made material omissions regarding its arrangement with Paulson & Co. in the Abacus transaction because Defendants "knowingly allowed Paulson to select the assets for the Abacus CDO, and knew that Paulson was selecting assets that it believed would perform poorly or fail." Similarly, the court found that Plaintiffs plausibly alleged that in the Hudson, Anderson, and Timberwolf I CDO transactions, Goldman represented that it held a long position in the equity tranches and did not disclose its substantial short positions. As the court said:

"having allegedly affirmatively represented [Goldman] had a particular investment interest in [these synthetic CDOs]—that it was long—in order to be both accurate and complete, Goldman ... had a duty to disclose [it] had a [greater] investment interest [from its] short [position] ... [because that was] a fact that, if disclosed, would significantly alter the ‘total mix’ of available information."

Finding that Plaintiffs established duty, the court turned to the scienter analysis. Scienter could be inferred when defendants "knew facts or had access to information suggesting that their public statements were not accurate." Here, Defendants allegedly assured shareholders that Goldman complied with the law and that it had "procedures in place to address 'potential conflicts of interest.'" Alternately, Goldman allegedly fostered a conflict of interest in the Abacus CDO and acted against investor interest in Hudson, Anderson and Timberwolf I. The court found that "Goldman knew or should have known that its statements about complying with the letter and spirit of the law, and its disclaimers regarding ‘potential’ conflicts of interest were inaccurate and incomplete." The court agreed with Plaintiffs that a strong inference of scienter could be drawn from Goldman's actions in the four CDO deals.

The court also found that Plaintiffs had sufficiently alleged loss causation and claims against the Individual Defendants. The Individual Defendants allegedly helped prepare the SEC filings at issue. Moreover, scienter was established through allegations that the Individual Defendants actively monitored the status of the relevant CDO assets and were intimately acquainted with the CDO operations.

With respect to the Wells Notices, Goldman, according to Plaintiffs, failed to disclose the receipt of the Wells Notices from the SEC in connection with the investigation of the Abacus transaction. Plaintiffs asserted that Defendants' disclosures about governmental investigations triggered a duty to disclose receipt of Wells Notices, and that by failing to do so caused the public to mistakenly believe that “no significant developments had occurred which made the investigation more likely to result in formal charges." The court noted that the delivery of a Wells Notice, while reflecting the SEC Enforcement Division’s determination on bringing charges, did not necessarily mean that charges would be filed. The court found that failure to disclose receipt of the Wells Notices did not render Goldman’s statement misleading and that Defendants' violation of FINRA's Wells Notice disclosure requirement was not grounds upon which a section 10(b) or Rule 10b-5 claim could be based. The court also rejected the argument that a FINRA rule requiring disclosure of a wells notice triggered a duty to disclose under the antifraud provisions.

The primary materials for this case may be found on the DU Corporate Governance website

September 24, 2012

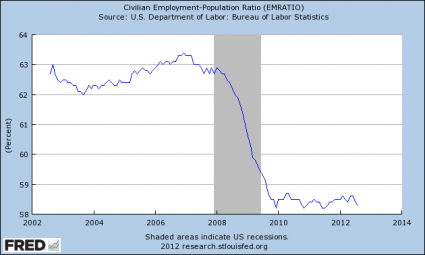

The Disheartening State of American Incomes

Doug Short at Global Economic

Intersection has a must-read post that pulls together some Census Report data on US incomes since 1967 and draws some conclusions. He looks first at real, rather than nominal, incomes, and shows how income in the top 5% and top quintile have grown faster than for the rest of the population:

And he includes an analysis that shows that people in all these cohorts are on average worse off than they

And he includes an analysis that shows that people in all these cohorts are on average worse off than they

He also provides an analysis of income trends by age cohort, and captures one of the things I’ve commented on, how many people in their 40s and 50s take a big dive income-wise when they lose their jobs. Remember, 45-54 is historically the peak earning years for household heads:

I suggest you read his post pronto. He has more good, if depressing, charts and accompanying discussion. Bottom line: anyone who gets optimistic about growth trend in the US needs to confront the fact that the seeming prosperity before the global crisis was fueled by rising household debt, not growing incomes. And even if the powers that be prevent further deleveraging by lowering borrowing costs on outstanding debt, that still fails to set the foundation for anything other than lackluster growth. Expecting consumers to lever up even further is not a way out of the stagnant incomes box.

September 21, 2012

The Commodity Matrix: What Is The Resource Of Tomorrow, And Who Will Benefit From It?

While it is impossible to predict where the S&P will be in 10 years (or even

1), one can safely make some assumptions about what the world will look like in

a decade (assuming of course it hasn't blown up by then). It will be hungry, it

will be thirsty, it will demand resources, and it will be crowded (and it will

certainly have lots and lots of wheelbarrows carrying pieces of paper to and fro

the local bakery). Implicitly then, countries which control the production and

export of various key natural resources and commodities channels will become

increasingly more strategic and important. However, for some economies, such as

the Middle East, whose entire export-based welfare is reliant on a core set of

commodities, this export-benefit may be a doubled-edged sword, should it lead to

militant antagonism by one time friends and outright enemies, and/or complacency

leading to lack of revenue stream diversity. In order to determine who the key

resource players in the future will be, we present the below commodity trade

matrix which answers two questions: how important is a commodity to a country,

and how important is a country to a commodity. As GS notes, those on the riskier

side of this equation are economies that are heavily reliant on oil, such as the

Middle East or even Russia (which albeit scores better on other hard

commodities). On the other hand, food exporters enjoy relatively better

diversity in their trade portfolios. We highlight the LatAm economies here,

while Canada and the US also look healthy. Will food (and water) be the oil of

the future, and will the next resource war be not over black, or even yellow,

gold, but, pardon the pun, edible gold?

Some additional observations via Goldman:

Some additional observations via Goldman:

Not all countries are blessed with abundant resources, and even among those that are, some countries have benefitted a great deal more than others as a result of the quality of their institutions. Indeed, resource wealth can, and has, tempted institutions to retain the revenues narrowly, rather than distribute them broadly or develop others parts of the economy. This is the reason why the presence of resources hasn’t historically guaranteed economic success. Australia, Canada, Russia, Brazil and South Africa are countries that have high levels of hard commodities per capita, while Argentina and the US should be added to the list if soft commodities are included.

But what are the resources of the future? We think it very likely that food, water and therefore land, will become increasingly important, tilting the advantage in favour of those capable of feeding the next billion people. As two of the world’s largest populations industrialise (hence producing less of their own food) and become wealthier (and hence hungrier), the way food flows around the world is likely to change significantly. Russia, South Korea, Japan and much of Western Europe are major food importers currently, while Brazil, Argentina, the US, Australia, Thailand and Canada sit on the other end of food trade. Here we have to mention Africa and India as regions with huge potential, but in need of greater institutional support to deliver it.

The current debate on the resources curse (the potential for resource-rich countries to become imbalanced) is also important. Being heavily reliant on a particularly commodity is risky as a result of the possibility of big shifts in the global economy, innovation-led substitutes or new discoveries. It is not implausible, for example, to imagine EM consumers extinguishing their demand for cigarettes just like their health conscious Western brethren did a few decades ago. This puts tobacco-heavy African economies like Zimbabwe at significant risk. Above is a commodity trade matrix to answer two entwined questions: how important is a commodity to a country, and how important is a country to a commodity? As expected, those on the riskier side of this equation are economies that are heavily reliant on oil, such as the Middle East or even Russia (which albeit scores better on other hard commodities). On the other hand, food exporters enjoy relatively better diversity in their trade portfolios. We highlight the LatAm economies here, while Canada and the US also look healthy.

The last question is which countries have succeeded despite resource deficits? Japan and South Korea stand out here, which cements our argument that necessity, in this case driven by constraints, is the mother of innovation.

Not all countries are blessed with abundant resources, and even among those that are, some countries have benefitted a great deal more than others as a result of the quality of their institutions. Indeed, resource wealth can, and has, tempted institutions to retain the revenues narrowly, rather than distribute them broadly or develop others parts of the economy. This is the reason why the presence of resources hasn’t historically guaranteed economic success. Australia, Canada, Russia, Brazil and South Africa are countries that have high levels of hard commodities per capita, while Argentina and the US should be added to the list if soft commodities are included.

But what are the resources of the future? We think it very likely that food, water and therefore land, will become increasingly important, tilting the advantage in favour of those capable of feeding the next billion people. As two of the world’s largest populations industrialise (hence producing less of their own food) and become wealthier (and hence hungrier), the way food flows around the world is likely to change significantly. Russia, South Korea, Japan and much of Western Europe are major food importers currently, while Brazil, Argentina, the US, Australia, Thailand and Canada sit on the other end of food trade. Here we have to mention Africa and India as regions with huge potential, but in need of greater institutional support to deliver it.

The current debate on the resources curse (the potential for resource-rich countries to become imbalanced) is also important. Being heavily reliant on a particularly commodity is risky as a result of the possibility of big shifts in the global economy, innovation-led substitutes or new discoveries. It is not implausible, for example, to imagine EM consumers extinguishing their demand for cigarettes just like their health conscious Western brethren did a few decades ago. This puts tobacco-heavy African economies like Zimbabwe at significant risk. Above is a commodity trade matrix to answer two entwined questions: how important is a commodity to a country, and how important is a country to a commodity? As expected, those on the riskier side of this equation are economies that are heavily reliant on oil, such as the Middle East or even Russia (which albeit scores better on other hard commodities). On the other hand, food exporters enjoy relatively better diversity in their trade portfolios. We highlight the LatAm economies here, while Canada and the US also look healthy.

The last question is which countries have succeeded despite resource deficits? Japan and South Korea stand out here, which cements our argument that necessity, in this case driven by constraints, is the mother of innovation.

September 20, 2012

New Study Finds “Severe Toxic Effects” of Pervasively Used Monsanto Herbicide Roundup and Roundup Ready GM Corn

Although I generally refrain from posting on Big Ag and relegate the topic to Links, I have a special interest in Monsanto. Last year, I had wanted to devise a list or ranking of top predatory companies, but could not find a way to make the tally sufficiently objective to be as useful in calling them out as it ought to be. Nevertheless, no matter how many ways I looked at the issue, it was clear that any ranking would put Monsanto as number 1. Monsanto has (among other things) genetically engineered seeds so that they can’t reproduce, denying farmers the ability to save seeds and have a measure of financial independence. In 2009, Vandana Shiva estimated that 200,000 farmers in India had committed suicide since 1997, and Monsanto was a major culprit:

I also know a wee bit about Monsanto because I was on its client team as a very junior investment banker at Goldman in the early 1980s. It was then a specialty chemical company, with the herbicide Roundup as the driver of its profits. The Goldman bankers and analysts were aware that Monsanto was effectively a one-trick pony, and that the St. Louis company was exposed both to the end of its patent and the possibility of Roundup-resistant weeds developing. Monsanto managed to extend the life of its patent both legally and far more important, practically, via the genetic engineering described above. The result is that Roundup has been far and away the most widely used herbicide in the US for over 30 years.

And that little fact makes a newly-released study particularly troubling. The study, by Dr. Joel Spiroux and Professor Gilles-Eric Seralini, was published in Food and Chemical Toxicology as “Long term toxicity of a herbicide Roundup and Roundup-tolerant genetically has modified maize.” The authors are both members of CRIIGEN (Committee for Research and Independent Information). Per the summary on the CRIIGEN website (furzy mouse):

But from my perspective, the more troubling part is the finding of Roundup toxicity. As the study suggests, Roundup is pervasive, it’s even in the water. If it is toxic to the degree this analysis suggests, we may be at the beginning of a large scale legal battle, similar to the suits against Big Tobacco, where the science was initially disputed but the link between smoking and lung cancer was eventually confirmed.

The problem is that if the study’s findings are valid, it will be hard to stuff this evil genie back in the bottle. But Europeans, particularly the French, have long been leery of GMOs and Big Ag generally, and this study may be the opening salvo in a serious pushback effort.

Update 4:30 AM: Below is the published article. Be sure to look at the photos.

Long Term Toxicity of Roundup Herbicide…

Read more

In 1998, the World Bank’s structural adjustment policies forced India to open up its seed sector to global corporations like Cargill, Monsanto and Syngenta. The global corporations changed the input economy overnight. Farm saved seeds were replaced by corporate seeds, which need fertilizers and pesticides and cannot be saved.Monsanto’s seeds can also sterilize wild crops via contamination. And Monsanto routinely sues farmers who wind up having some Monsanto seeds by virtue of seeds from neighboring farms blowing onto their property.

Corporations prevent seed savings through patents and by engineering seeds with non-renewable traits. As a result, poor peasants have to buy new seeds for every planting season and what was traditionally a free resource, available by putting aside a small portion of the crop, becomes a commodity. This new expense increases poverty and leads to indebtness.

The shift from saved seed to corporate monopoly of the seed supply also represents a shift from biodiversity to monoculture in agriculture. The district of Warangal in Andhra Pradesh used to grow diverse legumes, millets, and oilseeds. Now the imposition of cotton monocultures has led to the loss of the wealth of farmer’s breeding and nature’s evolution.

Monocultures and uniformity increase the risk of crop failure, as diverse seeds adapted to diverse to eco-systems are replaced by the rushed introduction of uniform and often untested seeds into the market. When Monsanto first introduced Bt Cotton in 2002, the farmers lost 1 billion rupees due to crop failure. Instead of 1,500 kilos per acre as promised by the company, the harvest was as low as 200 kilos per acre. Instead of incomes of 10,000 rupees an acre, farmers ran into losses of 6,400 rupees an acre. In the state of Bihar, when farm-saved corn seed was displaced by Monsanto’s hybrid corn, the entire crop failed, creating 4 billion rupees in losses and increased poverty for desperately poor farmers. Poor peasants of the South cannot survive seed monopolies. The crisis of suicides shows how the survival of small farmers is incompatible with the seed monopolies of global corporations.

I also know a wee bit about Monsanto because I was on its client team as a very junior investment banker at Goldman in the early 1980s. It was then a specialty chemical company, with the herbicide Roundup as the driver of its profits. The Goldman bankers and analysts were aware that Monsanto was effectively a one-trick pony, and that the St. Louis company was exposed both to the end of its patent and the possibility of Roundup-resistant weeds developing. Monsanto managed to extend the life of its patent both legally and far more important, practically, via the genetic engineering described above. The result is that Roundup has been far and away the most widely used herbicide in the US for over 30 years.

And that little fact makes a newly-released study particularly troubling. The study, by Dr. Joel Spiroux and Professor Gilles-Eric Seralini, was published in Food and Chemical Toxicology as “Long term toxicity of a herbicide Roundup and Roundup-tolerant genetically has modified maize.” The authors are both members of CRIIGEN (Committee for Research and Independent Information). Per the summary on the CRIIGEN website (furzy mouse):

For the first time, the health impact of a GMO and a widely used pesticide have been comprehensively assessed * in a long term animal feeding trial of greater duration and with more detailed analyses than any previous studies, by environmental and food agencies, governments, industries or researchers institutes.The difference between this study and most studies of toxicity is the duration of the exposure. Analyses for regulatory purposes are only 3 months in length, while this was two years (which is pretty close to a normal rat lifespan, or at least for rats as pets). The sample size, 200 animals, is large enough that the findings can’t be dismissed casually. CRIIGEN, a not for profit with a large roster of scientific advisors, is making an aggressive push and launching a related book and documentary. But CRIIGEN can’t be depicted as knee jerk anti GMO. In an interview, Dr. Spiroux stressed that he approved of the use of transgenic GMOs to produce medication, such as insulin, but that he and other CRIIGEN members are opposed to “pesticides plants that are agricultural GMOs and above all are poorly evaluated.” And he is far from alone. A burger eating buddy (as in no sanctimonious health foodie) who is a biomedical engineer whose first job was with the NIH would get agitated on the subject of GMOs, complaining it was a mass scale, uncontrolled experiment on the public at large. He even tried avoiding GMOs but found it too difficult and gave up.

The two tested products are in very common use : (i) a transgenic maize made tolerant to Roundup, the characteristic shared by over 80% of food and animal feed GMOs, and (ii) Roundup itself, the most widely used herbicide on the planet. The regulatory approval process requires these products to be tested on rats as a surrogate for humans.

The new research took the form of a two year feeding trial on 200 rats, monitored for outcomes against more than 100 parameters. The doses were consistent with typical dietary/ environmental exposure (from 11% GMO in the diet, and 0.1 ppb in water).

The results, which are of serious concern, included increased and more rapid mortality, coupled with hormonal non linear and sex related effects. Females developed significant and numerous mammary tumours, pituitary and kidney problems. Males died mostly from severe hepatorenal chronic deficiencies. Professor Seralini’s team in the University of Caen is publishing this detailed study in one of the leading scientific international peer-reviewed journals of food toxicology, on line on Sept. 19, 2012.

The implications are extremely serious. They demonstrate the toxicity, both of a GMO with the most widely spread transgenic character and of the most widely used herbicide, even when ingested at extremely low levels, (corresponding to those found in surface or tap water). In addition, these results call into question the adequacy of the current regulatory process, used throughout the world by agencies involved in the assessment of health, food and chemicals, and industries seeking commercialisation of products.

But from my perspective, the more troubling part is the finding of Roundup toxicity. As the study suggests, Roundup is pervasive, it’s even in the water. If it is toxic to the degree this analysis suggests, we may be at the beginning of a large scale legal battle, similar to the suits against Big Tobacco, where the science was initially disputed but the link between smoking and lung cancer was eventually confirmed.

The problem is that if the study’s findings are valid, it will be hard to stuff this evil genie back in the bottle. But Europeans, particularly the French, have long been leery of GMOs and Big Ag generally, and this study may be the opening salvo in a serious pushback effort.

Update 4:30 AM: Below is the published article. Be sure to look at the photos.

Long Term Toxicity of Roundup Herbicide…

Read more

September 19, 2012

Matt Taibbi: The People Vs. Goldman Sachs

To fully grasp the case against Goldman, one first needs to understand that the financial crime wave described in the Levin report came on the heels of a decades-long lobbying campaign by Goldman and other titans of Wall Street, who pleaded over and over for the right to regulate themselves.

Before that campaign, banks were closely monitored by a host of federal regulators, including the Office of the Comptroller of the Currency, the FDIC and the Office of Thrift Supervision. These agencies had examiners poring over loans and other transactions, probing for behavior that might put depositors or the system at risk. When the examiners found illegal or suspicious behavior, they built cases and referred them to criminal authorities like the Justice Department.

This system of referrals was the backbone of financial law enforcement through the early Nineties. William Black was senior deputy chief counsel at the Office of Thrift Supervision in 1991 and 1992, the last years of the S&L crisis, a disaster whose pansystemic nature was comparable to the mortgage fiasco, albeit vastly smaller. Black describes the regulatory MO back then. "Every year," he says, "you had thousands of criminal referrals, maybe 500 enforcement actions, 150 civil suits and hundreds of convictions."

But beginning in the mid-Nineties, when former Goldman co-chairman Bob Rubin served as Bill Clinton's senior economic-policy adviser, the government began moving toward a regulatory system that relied almost exclusively on voluntary compliance by the banks. Old-school criminal referrals disappeared down the chute of history along with floppy disks and scripted television entertainment. In 1995, according to an independent study, banking regulators filed 1,837 referrals. During the height of the financial crisis, between 2007 and 2010, they averaged just 72 a year.

But spiking almost all criminal referrals wasn't enough for Wall Street. In 2004, in an extraordinary sequence of regulatory rollbacks that helped pave the way for the financial crisis, the top five investment banks — Goldman, Merrill Lynch, Morgan Stanley, Lehman Brothers and Bear Stearns — persuaded the government to create a new, voluntary approach to regulation called Consolidated Supervised Entities. CSE was the soft touch to end all soft touches. Here is how the SEC's inspector general described the program's regulatory army: "The Office of CSE Inspections has only two staff in Washington and five staff in the New York regional office."

Among the bankers who helped convince the SEC to go for this ludicrous program was Hank Paulson, Goldman's CEO at the time. And in exchange for "submitting" to this new, voluntary regime of law enforcement, Goldman and other banks won the right to lend in virtually unlimited amounts, regardless of their cash reserves — a move that fueled the catastrophe of 2008, when banks like Bear and Merrill were lending out 35 dollars for every one in their vaults.

Goldman's chief financial officer then and now, a fellow named David Viniar, wrote a letter in February 2004, commending the SEC for its efforts to develop "a regulatory framework that will contribute to the safety and soundness of financial institutions and markets by aligning regulatory capital requirements more closely with well-developed internal risk-management practices." Translation: Thanks for letting us ignore all those pesky regulations while we turn the staid underwriting business into a Charlie Sheen house party.

Goldman and the other banks argued that they didn't need government supervision for a very simple reason: Rooting out corruption and fraud was in their own self-interest. In the event of financial wrongdoing, they insisted, they would do their civic duty and protect the markets. But in late 2006, well before many of the other players on Wall Street realized what was going on, the top dogs at Goldman — including the aforementioned Viniar — started to fear they were sitting on a time bomb of billions in toxic assets. Yet instead of sounding the alarm, the very first thing Goldman did was tell no one. And the second thing it did was figure out a way to make money on the knowledge by screwing its own clients. So not only did Goldman throw a full-blown "bite me" on its own self-righteous horseshit about "internal risk management," it more or less instantly sped way beyond inaction straight into craven manipulation.

"This is the dog that didn't bark," says Eliot Spitzer, who tangled with Goldman during his years as New York's attorney general. "Their whole political argument for a decade was 'Leave us alone, trust us to regulate ourselves.' They not only abdicated that responsibility, they affirmatively traded against the entire market."

Read the entire artire

Before that campaign, banks were closely monitored by a host of federal regulators, including the Office of the Comptroller of the Currency, the FDIC and the Office of Thrift Supervision. These agencies had examiners poring over loans and other transactions, probing for behavior that might put depositors or the system at risk. When the examiners found illegal or suspicious behavior, they built cases and referred them to criminal authorities like the Justice Department.

This system of referrals was the backbone of financial law enforcement through the early Nineties. William Black was senior deputy chief counsel at the Office of Thrift Supervision in 1991 and 1992, the last years of the S&L crisis, a disaster whose pansystemic nature was comparable to the mortgage fiasco, albeit vastly smaller. Black describes the regulatory MO back then. "Every year," he says, "you had thousands of criminal referrals, maybe 500 enforcement actions, 150 civil suits and hundreds of convictions."

But beginning in the mid-Nineties, when former Goldman co-chairman Bob Rubin served as Bill Clinton's senior economic-policy adviser, the government began moving toward a regulatory system that relied almost exclusively on voluntary compliance by the banks. Old-school criminal referrals disappeared down the chute of history along with floppy disks and scripted television entertainment. In 1995, according to an independent study, banking regulators filed 1,837 referrals. During the height of the financial crisis, between 2007 and 2010, they averaged just 72 a year.

But spiking almost all criminal referrals wasn't enough for Wall Street. In 2004, in an extraordinary sequence of regulatory rollbacks that helped pave the way for the financial crisis, the top five investment banks — Goldman, Merrill Lynch, Morgan Stanley, Lehman Brothers and Bear Stearns — persuaded the government to create a new, voluntary approach to regulation called Consolidated Supervised Entities. CSE was the soft touch to end all soft touches. Here is how the SEC's inspector general described the program's regulatory army: "The Office of CSE Inspections has only two staff in Washington and five staff in the New York regional office."

Among the bankers who helped convince the SEC to go for this ludicrous program was Hank Paulson, Goldman's CEO at the time. And in exchange for "submitting" to this new, voluntary regime of law enforcement, Goldman and other banks won the right to lend in virtually unlimited amounts, regardless of their cash reserves — a move that fueled the catastrophe of 2008, when banks like Bear and Merrill were lending out 35 dollars for every one in their vaults.

Goldman's chief financial officer then and now, a fellow named David Viniar, wrote a letter in February 2004, commending the SEC for its efforts to develop "a regulatory framework that will contribute to the safety and soundness of financial institutions and markets by aligning regulatory capital requirements more closely with well-developed internal risk-management practices." Translation: Thanks for letting us ignore all those pesky regulations while we turn the staid underwriting business into a Charlie Sheen house party.

Goldman and the other banks argued that they didn't need government supervision for a very simple reason: Rooting out corruption and fraud was in their own self-interest. In the event of financial wrongdoing, they insisted, they would do their civic duty and protect the markets. But in late 2006, well before many of the other players on Wall Street realized what was going on, the top dogs at Goldman — including the aforementioned Viniar — started to fear they were sitting on a time bomb of billions in toxic assets. Yet instead of sounding the alarm, the very first thing Goldman did was tell no one. And the second thing it did was figure out a way to make money on the knowledge by screwing its own clients. So not only did Goldman throw a full-blown "bite me" on its own self-righteous horseshit about "internal risk management," it more or less instantly sped way beyond inaction straight into craven manipulation.

"This is the dog that didn't bark," says Eliot Spitzer, who tangled with Goldman during his years as New York's attorney general. "Their whole political argument for a decade was 'Leave us alone, trust us to regulate ourselves.' They not only abdicated that responsibility, they affirmatively traded against the entire market."

Read the entire artire

September 18, 2012

Faber's 'Fed Counterfeiting' Remark is Unusual but Not Extreme These Days

Marc Faber: If I Were Bernanke, I Would Resign ... Central bankers are "counterfeit money printers" and Federal Reserve Chairman Ben Bernanke should resign for messing up the U.S. economy so badly, Marc Faber, author of the Gloom, Doom and Boom, told CNBC on Friday. He said Bernanke was one of the main proponents of an ultra-expansionist economic monetary policy that was to blame for the latest financial crisis. "If I had messed up as badly as Bernanke I would for sure resign. The mandate of the Fed to boost asset prices and thereby create wealth is ludicrous — it doesn't work that way. It's a temporary boost followed by a crash," Faber said. – CNBC

Dominant Social Theme: The Fed is triumphing slowly but surely.

Free-Market Analysis: This is fairly unprecedented. A so-called mainstream economist and investor, Marc Faber, has accused the Federal Reserve of "counterfeiting."

While Faber is certainly on the conservative/libertarian side of the spectrum, his views have been popularly disseminated by the mainstream media for years.

For us, such statements confirm the crumbling of the elite's central banking dominant social theme. We predicted several years ago now that the Fed had lost any claim to the moral high ground.

Once it became clear to people that Fed officials were printing TRILLIONS during a time of great financial pain for ordinary people, the Fed, we believed, would become an object of popular anger.

That process is well underway. To see some previous articles on this issue, search the Internet for "Daily Bell" along with the terms "Fed" and "morality" and "inspector general."

This unraveling must be of great concern to the power elite that relies on central banking to fund its push toward one-world government. But we have also predicted that within the context of what we call the Internet Reformation, there would be nothing much the elites could do about it.

We do believe that the power elite has, perhaps, cleverly launched a pure fiat counterattack, acknowledging that the public/private Fed model is probably done for and seeking to sway public opinion toward an entirely government focused option.

The elites, in our view, don't care whether or not monopoly fiat central banking is conducted "privately" or by government entities. Via mercantilism they will control the process of money printing either way.

Nonetheless, an elite meme – the necessity of monopoly fiat central banking – is becoming increasingly hard to sustain. Faber's attacks, while extreme, are merely a symptom of that.

Again, Faber is not to be considered an outlier. He is a man with significant mainstream credentials. Here's a bit of background on Faber.

Dr. Marc Faber was born in Zurich, Switzerland. He went to school in Geneva and Zurich and finished high school with the Matura. He studied Economics at the University of Zurich and, at the age of 24 obtained a PhD in Economics magna cum laude.

Between 1970 and 1978, Dr. Faber worked for White Weld & Company Limited in New York, Zurich and Hong Kong. Since 1973, he has lived in Hong Kong. From 1978 to February 1990 he was the Managing Director of Drexel Burnham Lambert (HK) Ltd.

In June 1990 he set up his own business, MARC FABER LIMITED, which acts as an investment advisor, fund manager and broker/dealer. Dr. Faber publishes a widely read monthly investment newsletter "THE GLOOM, BOOM & DOOM" report which highlights unusual investment opportunities.

This bio was posted with an interview we did with Dr. Faber in June 2011. You can see the interview here:

Marc Faber on 21st Century Investing, Why It's Too Late for the Dollar and Why Emerging Markets Look Good

The article excerpted above reminds us that Dr. Faber's perspective on finance and monetary stimulation has reaped rewards for investors as far back as 1987, when he received media credit for predicting the 1987 stock market crash.

What's unusual about Faber's stance is that he's chosen to be even more outspoken than usual. For anyone in the "mainstream" to characterize central banking operations as counterfeiting is newsworthy. But Faber didn't stop there. Here's some more from the article:

"This unlimited QE (quantitative easing), buying mortgage-backed securities (MBS) and continuing operation twist has the implication of simply having asset prices go up and the money flows down to the Mayfair economy," Faber said.

A Mayfair economy is one which benefits the wealthier and better off in society. Faber said this latest round of QE would not help the "man on the street".

"QE helps rich people whose asset prices go up and whose net worth then increases but it doesn't flow to the man on the street who is faced with higher costs of living with price rises. You just have a small economy that is booming but the majority of the economy is damaged by QE," he said.

This is strong stuff because Faber is essentially explaining that Ben Bernanke's approach to the market is not helpful for ordinary citizens. Usually, mainstream pundits go along with the idea that central bank price-fixing provides valuable support for the economy as a whole.

The proximate cause of Faber's statements is the announcement by Bernanke that the Fed would buy $40 billion a month in MBS, in order to unfreeze the mortgage market and give homeowners the chance to refinance.

Surprisingly, Bernanke's announcement has been met with some skepticism within the mainstream. Sorting through the commentary, one is struck by the increasing resistance to portray the Fed as being helpful to the larger economy.

Perhaps the media is merely acknowledging public sentiment, or perhaps mainstream participants themselves are growing impatient.

It is widely acknowledged that the Fed's money printing has boosted stock prices, which have more than doubled in aggregate within the US. But tens of millions are out of work. As much as 30 or even 40 percent of the US workforce probably suffers from lack of employment or unemployment.

Within this context, Faber's statements are unusual but not radical. His sentiments are increasingly echoed by others despite their forceful nature.

"The money printers are responsible for this crisis. If we continue with this expansionist monetary policy we won't be facing a fiscal cliff it will be a fiscal grand canyon," he added.

We try to chart reactions to dominant social themes because they can reveal larger potential changes when it comes to the economy and what actions the top elites may take. It seems to us that the militarism now spreading around the world is a direct elite reaction to the challenges to the modern central banking system and to modern economies generally.

There are various other reactions, too, including perhaps surreptitious elite encouragement of pure fiat, alternative money systems. Analyze elite dominant social themes to support a larger comprehension about where the world may be headed. These memes are the building blocks of directed history.

Conclusion: They are not the only tools that one needs to use but they surely deserve to be part of a larger toolkit as elite memes continue to unravel.

Dominant Social Theme: The Fed is triumphing slowly but surely.

Free-Market Analysis: This is fairly unprecedented. A so-called mainstream economist and investor, Marc Faber, has accused the Federal Reserve of "counterfeiting."

While Faber is certainly on the conservative/libertarian side of the spectrum, his views have been popularly disseminated by the mainstream media for years.

For us, such statements confirm the crumbling of the elite's central banking dominant social theme. We predicted several years ago now that the Fed had lost any claim to the moral high ground.

Once it became clear to people that Fed officials were printing TRILLIONS during a time of great financial pain for ordinary people, the Fed, we believed, would become an object of popular anger.

That process is well underway. To see some previous articles on this issue, search the Internet for "Daily Bell" along with the terms "Fed" and "morality" and "inspector general."

This unraveling must be of great concern to the power elite that relies on central banking to fund its push toward one-world government. But we have also predicted that within the context of what we call the Internet Reformation, there would be nothing much the elites could do about it.

We do believe that the power elite has, perhaps, cleverly launched a pure fiat counterattack, acknowledging that the public/private Fed model is probably done for and seeking to sway public opinion toward an entirely government focused option.

The elites, in our view, don't care whether or not monopoly fiat central banking is conducted "privately" or by government entities. Via mercantilism they will control the process of money printing either way.

Nonetheless, an elite meme – the necessity of monopoly fiat central banking – is becoming increasingly hard to sustain. Faber's attacks, while extreme, are merely a symptom of that.

Again, Faber is not to be considered an outlier. He is a man with significant mainstream credentials. Here's a bit of background on Faber.

Dr. Marc Faber was born in Zurich, Switzerland. He went to school in Geneva and Zurich and finished high school with the Matura. He studied Economics at the University of Zurich and, at the age of 24 obtained a PhD in Economics magna cum laude.

Between 1970 and 1978, Dr. Faber worked for White Weld & Company Limited in New York, Zurich and Hong Kong. Since 1973, he has lived in Hong Kong. From 1978 to February 1990 he was the Managing Director of Drexel Burnham Lambert (HK) Ltd.

In June 1990 he set up his own business, MARC FABER LIMITED, which acts as an investment advisor, fund manager and broker/dealer. Dr. Faber publishes a widely read monthly investment newsletter "THE GLOOM, BOOM & DOOM" report which highlights unusual investment opportunities.

This bio was posted with an interview we did with Dr. Faber in June 2011. You can see the interview here:

Marc Faber on 21st Century Investing, Why It's Too Late for the Dollar and Why Emerging Markets Look Good

The article excerpted above reminds us that Dr. Faber's perspective on finance and monetary stimulation has reaped rewards for investors as far back as 1987, when he received media credit for predicting the 1987 stock market crash.

What's unusual about Faber's stance is that he's chosen to be even more outspoken than usual. For anyone in the "mainstream" to characterize central banking operations as counterfeiting is newsworthy. But Faber didn't stop there. Here's some more from the article:

"This unlimited QE (quantitative easing), buying mortgage-backed securities (MBS) and continuing operation twist has the implication of simply having asset prices go up and the money flows down to the Mayfair economy," Faber said.

A Mayfair economy is one which benefits the wealthier and better off in society. Faber said this latest round of QE would not help the "man on the street".

"QE helps rich people whose asset prices go up and whose net worth then increases but it doesn't flow to the man on the street who is faced with higher costs of living with price rises. You just have a small economy that is booming but the majority of the economy is damaged by QE," he said.

This is strong stuff because Faber is essentially explaining that Ben Bernanke's approach to the market is not helpful for ordinary citizens. Usually, mainstream pundits go along with the idea that central bank price-fixing provides valuable support for the economy as a whole.

The proximate cause of Faber's statements is the announcement by Bernanke that the Fed would buy $40 billion a month in MBS, in order to unfreeze the mortgage market and give homeowners the chance to refinance.

Surprisingly, Bernanke's announcement has been met with some skepticism within the mainstream. Sorting through the commentary, one is struck by the increasing resistance to portray the Fed as being helpful to the larger economy.

Perhaps the media is merely acknowledging public sentiment, or perhaps mainstream participants themselves are growing impatient.

It is widely acknowledged that the Fed's money printing has boosted stock prices, which have more than doubled in aggregate within the US. But tens of millions are out of work. As much as 30 or even 40 percent of the US workforce probably suffers from lack of employment or unemployment.

Within this context, Faber's statements are unusual but not radical. His sentiments are increasingly echoed by others despite their forceful nature.

"The money printers are responsible for this crisis. If we continue with this expansionist monetary policy we won't be facing a fiscal cliff it will be a fiscal grand canyon," he added.

We try to chart reactions to dominant social themes because they can reveal larger potential changes when it comes to the economy and what actions the top elites may take. It seems to us that the militarism now spreading around the world is a direct elite reaction to the challenges to the modern central banking system and to modern economies generally.

There are various other reactions, too, including perhaps surreptitious elite encouragement of pure fiat, alternative money systems. Analyze elite dominant social themes to support a larger comprehension about where the world may be headed. These memes are the building blocks of directed history.

Conclusion: They are not the only tools that one needs to use but they surely deserve to be part of a larger toolkit as elite memes continue to unravel.

September 17, 2012

Is QE3 Yet Another Stealth Bank Bailout?

It’s difficult to puzzle out what Bernanke thinks he is accomplishing with QE3. The level of bond buying, as various commentators have pointed out, is much lower than in the earlier QE programs. And pulling out bigger guns in the past was not terribly productive. As we wrote in April 2011 in a post titled “Mirabile Dictu! Economists Agree All the Fed Has Done is Goose Financial Markets!“:

You heard it first in the blogopshere. From the New York Times: