Gary Weiss, the Wall Street writer who was ahead of his time with his comprehensive chronicle of Wall Street corruption in 2006 (Wall Street Versus America) charts a bold new course this week with the release of Ayn Rand Nation: The Hidden Struggle for America’s Soul.

Thanks to Weiss, the nation might just escape the next wave of Ayn Rand’s radical capitalism and student brainwashing by corporate money vultures fanning out across U.S. campuses.

Thanks to the trail paved in Weiss’ book, we did some further digging into the money cartel financing this “spontaneous” outpouring of campus and Tea Party interest in Rand, whose work is regularly considered by top academics to be mediocre and simpleminded.

This cartel has a striking similarity to the network of university economists set up by Big Tobacco in a money for hire scheme from 1983 to the mid 90s to blanket Congress and the media with bogus OpEds and research papers.

While it has been well known that the oil billionaire, Charles Koch, has been funneling tens of millions of dollars through his foundation into economic programs at public universities and mandating approval of faculty and curriculum in some instances, it has not heretofore been reported that a sweeping partnership in these programs has sprung up between Koch and the southern banking giant, BB&T, the latter corporation mandating that Ayn Rand’s book Atlas Shrugged is taught and distributed to students.

Koch is based in Wichita, Kansas; BB&T in Winston-Salem, North Carolina. An email request to the Charles G. Koch Foundation for information on how this partnership evolved went unanswered, despite Koch’s copious web site claiming to want to set the record straight on his past funding schemes.

Raising more eyebrows is the discovery that the so-called populous craze for Ayn Rand’s seminal work, Atlas Shrugged, is also being financed by a decidedly non-populist pact of deep-pocketed hedge fund operators.

As we reported yesterday in this space, the Ayn Rand Institute (ARI) has already conceded the following on its web site:

“ARI seeks to spearhead a cultural renaissance that will reverse the anti-reason, anti-individualism, anti-freedom, anti-capitalist trends in today’s culture. The major battleground in this fight for reason and capitalism is the educational institutions—high schools and, above all, the universities, where students learn the ideas that shape their lives…To date, more than 1.4 million copies of these Ayn Rand novels have been donated to 30,000 teachers in 40,000 classrooms across the United States and Canada.

“Based on a projected shelf life of five years per book, we estimate that more than 3 million young people have been introduced to Ayn Rand’s books and ideas as a result of our programs to date…partnerships have been established between ARI and the corporate community to advance Ayn Rand’s ideas in the universities. (Italics added.)

“Through ARI’s assistance, Ayn Rand’s ideas are taught and studied at more than 50 of America’s most influential institutions of higher education, including: Clemson University, Duke University, University of Virginia, University of Texas at Austin, University of Pittsburgh, University of North Carolina at Chapel Hill, Brown University, University of Kentucky, University of South Carolina, University of Florida, University of West Virginia and Wake Forest University.”

Weiss piqued our curiosity when he mentions in his book that the Ayn Rand Institute based in Irvine, California is holding its annual gala fundraiser, not on the west coast, but at the swanky St. Regis hotel in Manhattan and charging $1500 a plate. We learn further from Weiss that Arline Mann, Managing Director and Associate General Counsel of the Board of Goldman, Sachs & Company is the Co-Chair of the Ayn Rand Institute. To move the money trail along, Weiss interviews Barry Colvin, Vice Chairman of a hedge fund, Balyasny Asset Management, who just up and decides to open a New York chapter of the Ayn Rand Institute and spearhead a fund drive.

Weiss attends the 2010 St. Regis event and was stuck at an ultraconservative press table, getting a sugar high on moelleux aux chocolat, coconut sorbet and berry chutney, as the mindless clap-trap of Objectivist theory drones into the microphone.

What happened at the September 15, 2011 redux of this fundraiser, “The Atlas Shrugged Revolution,” when Weiss’ book is no doubt already in galleys, might surprise even Weiss. The hedgies are fully in control of the event, dominating the podium and raising a little more than a cool $1 million, besting the prior year’s take by $600,000.

The key speakers included Dmitry Balyasny of the hedge fund, Balyasny Asset Management, as well as Colvin, also from this hedge fund and creator of the New York chapter of the Ayn Rand Institute. Another key speaker was Scott Schweighauser, partner and chief investment officer of Aurora Investment Management, L.L.C., a fund of hedge funds managing approximately $10 billion.

The biggest donors at the event who would allow their names to be published, included the following:

$50,000: Balyasny Asset Management

$25,000: Christopher (Chris) Asness, managing principal and co-founder of hedge fund AQR Capital Management. Asness is a former managing director at Goldman, Sachs & Co.

$25,000: Eric Brooks and Jeff Yass of hedge fund and private equity firm Susquehanna International Group.

$25,000: Jim Brown of hedge fund, Brandes Investment Partners.

$25,000: Scott Schweighauser of fund of hedge funds, Aurora Investment Management, L.L.C.

There are two simple words that sum up why hedge funds would be bankrolling the resurrection of a woman who’s been dead for thirty years: Dodd-Frank, the financial reform legislation that Wall Street is desperately trying to kill.

While the hedgies are financing the flood of books to high schools and campus, Koch and BB&T are taking care of business with the professors.

Among the multitude of co-opted campuses – three stand out as taking on the aura of right-wing flacks gone bonkers rather than a serious economic course.

Check out the web site for Florida Gulf Coast University’s Distinguished Professorship of Free Enterprise:

Here’s a few choice phrases from the BB&T/Koch jointly funded program: “students continued to develop a local chapter of Students for Liberty…Edson attended the CATO University sponsored in Washington, D.C. by the Cato Institute [founded by Charles Koch]…He was accepted into the Koch internship program…he is currently attending the graduate school of economics at George Mason University [effectively owned lock stock and barrel by Koch according to media reports]…Brandon [Wasicsko] will serve an internship this summer at the Ayn Rand Institute…Traivis Leicht…will be the first FGCU student to attend the Koch Associates Program…Brian Mitterko will serve a summer Koch internship with the Charles G. Koch Charitable Foundation…Cifuentes attended a special seminar program co-sponsored by The Liberty Fund and the Charles G. Koch Charitable Foundation in Washington, D.C…All Economics and Finance majors receive a copy of Atlas Shrugged in Intermediate Price Theory (a required course for both majors ). Professor Hobbs teaches a course employing this text – ECP 3009: The Moral Foundations of Capitalism – as part of the BB&T gift. The book has also been given to a number of other students who show an interest and to students who wish to give a copy to a friend or family member.”

That every exit door from this program leads to a Koch funded group or an Ayn Rand text is spine chilling. Where are the advocates for these impressionable young minds at this institution of higher learning? Forget about the nonsensical “Moral Foundations of Capitalism,” this whole program is a moral outrage.

Similarly conflicted is the Initiative for Public Choice and Market Process at the College of Charleston (SC), which was founded in the fall of 2008 with gifts from BB&T Charitable Foundation and the Charles G. Koch Charitable Foundation. With only minor exceptions, the internships are either directly run by Koch, nonprofits created by Koch or funded by Koch.

And then there is Troy University, a state-funded school in Alabama. Troy University was odd enough before BB&T and Koch emerged on campus. The Troy web site explains: “Troy University (TROY) in partnership with Federal Bureau of Investigation (FBI) provides opportunities for its employees to achieve personal and professional growth through TROY’s undergraduate and graduate degree programs…In 1973, the University opened sites at military bases in Florida. Today, TROY Global Campus operates more than 60 sites in 17 U.S. states and 11 nations.”

On September 10, 2010, Troy University announced that $3.6 million had been donated by BB&T, the Charles G. Koch Foundation, and a former graduate, Manuel H. Johnson. The funds would create the Manuel H. Johnson Center for Political Economy. (“Political economy,” “morality of capitalism,” “free enterprise,” these are buzz words strongly suggesting that if you pull back the curtain, you’ll find right wing corporate operatives skulking in the wings.)

The entire faculty of the program has a previous money link to Koch or BB&T:

The Executive Director, Dr. Scott A. Beaulier, was previously the BB&T Distinguished Professor of Capitalism at Mercer University. Dr. George R. Crowley, the Assistant Professor of Economics, previously received two research grants from the Mercatus Center (a Koch funded front group) and was awarded a Charles G. Koch Doctoral Fellowship while at West Virginia University. Dr. Daniel J. Smith, Assistant Professor of Economics, received awards and/or fellowships from the Institute for Humane Studies and the Mercatus Center, both long-term Koch funded programs at George Mason University, which has received over $30 million from Koch foundations. Dr. Daniel S. Sutter, the Charles G. Koch Professor of Economics, is also a senior affiliated scholar at Mercatus. Both Smith and Sutter received their Ph.D.s in Economics from George Mason University.

The concentration of Koch money and influence at Troy is a disgrace at a publicly funded institute of higher education. That it is occurring under the nose of an institution with an FBI partnership tells one a great deal about corporate money and Washington today.

DAILY BUSINESS REPORT - Financial Updates, International Markets and Business News

February 29, 2012

February 28, 2012

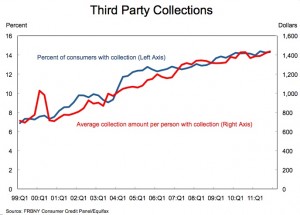

Towards a Creditor State – One in Seven Americans Pursued by Debt Collectors

I went through the Federal Reserve’s Quarterly Release on Household Debt and Credit released today, and there were two notable trends. One is that the amount of consumer debt is declining, but that delinquency rates are stabilizing above what they were before the crisis. And the second is in this graph, which is that the number of people subject to third party collections has doubled since 2000, from a little less than 7% to a little over 14% of consumers. Ten years ago, one in fourteen American consumers were pursued by debt collectors. Today it’s one in seven.

The experience of debt collection can be chilling, as this 2007 ABC News report suggests.

Consumers around the country have taped threatening phone calls from collectors who have called in the middle of the night, used abusive language and have threatened to have people fired from work or thrown in jail. All of these tactics are illegal under federal law.

One of the characteristics of the new social contract ushered in by both George W. Bush and Barack Obama is the increasing power of creditors to govern outright, from tax farming by banks to the use of credit checks to access employment opportunities.

There are now thousands of people legally jailed because they aren’t paying their bills, ie. debtor’s prisons have returned. Occasionally elites let it slip that this is not an accident, but is their goal – former Comptroller General David Walker has wistfully pined for debtor’s prisons overtly (on CNBC, no less).

This may be somewhat mediated by government action, as the CFPB is beginning to make noise around debt collection and credit ratings, and Illinois Attorney General Lisa Madigan is working to stop debt-related arrest warrants. But only somewhat, only where the government can protect you and only when there is the political will to do so. Increasingly, creditors are coming to set up the institutional structures for financial surveillance, state-sponsored enforcement of their claims through tightened bankruptcy laws and the selective use of jail, and the denial of economic opportunity based on one’s interaction with the financial system.

This is part of the new social contract. The sheer percentage of consumers with third party collections in pursuit is striking. Additionally, the uptrend through both Bush boom and Obama bust years of the percentage of people being tracked down by third party collection agencies suggests we live in a different country than we did just ten years ago.

Again, ten years ago, one in fourteen Americans were pursued by debt collectors. Today it’s one in seven. I suspect this number will keep going up. And though debt collection is a highly competitive field, it’s also a growth industry.

February 27, 2012

G20 Wants to Push European Bailout Fund to $2 Trillion

This just out from Reuters:

•G20 Finance leaders push to increase European bailout fund to $2 Trillion

•Want to combine ESM & EFSF, creating ~$1 Trillion dollar fund

•IMF to request $500 - $600 Billion in "new resources", which combined with current funds puts it at ~$1 Trillion dollars

•Germany remains the thorn in the socialists Eurozone's side

◦Schaeuble: "It does not make any economic sense to follow the calls for proposals which would be mutualizing the interest risk in the euro zone, nor in pumping money into rescue funds, nor in starting up the ECB printing press"

So this is on top of Wednesday's $600B LTRO? Sweet.

As I pointed out here, U.S. contributes 17% of the total funds to the IMF. How much did Obama put into his contingency slush fund in his 2013 budget - hopefully $102 Billion.

And someone please tell Wolfgang that he's too late:

•G20 Finance leaders push to increase European bailout fund to $2 Trillion

•Want to combine ESM & EFSF, creating ~$1 Trillion dollar fund

•IMF to request $500 - $600 Billion in "new resources", which combined with current funds puts it at ~$1 Trillion dollars

•Germany remains the thorn in the socialists Eurozone's side

◦Schaeuble: "It does not make any economic sense to follow the calls for proposals which would be mutualizing the interest risk in the euro zone, nor in pumping money into rescue funds, nor in starting up the ECB printing press"

So this is on top of Wednesday's $600B LTRO? Sweet.

As I pointed out here, U.S. contributes 17% of the total funds to the IMF. How much did Obama put into his contingency slush fund in his 2013 budget - hopefully $102 Billion.

And someone please tell Wolfgang that he's too late:

February 26, 2012

Foreclosure settlement a failure of law, a triumph for bank attorneys

After many months of wrangling, a foreclosure settlement has been reached between 49 state attorneys general and a consortium of banks.

It is an epic failure of law and a triumph for bank attorneys.

It will accomplish little of value, as I’ll explain. First, let’s recall what the “robosigning” foreclosure scandal was all about.

Foreclosure is an extremely serious issue in American jurisprudence. As a nation of laws with strong respect for property rights, we have always treated this process appropriately. After all, having a sheriff forcibly evict a family that typically made a down payment, moved into a home, lived there for some years, made payments, etc., is disruptive — for the family, the lender and the neighborhood.

Foreclosure laws vary from state to state. However, all are specific and precise as to the legal steps that must be followed, from the homeowner’s initial delinquency onward. There are benefits to giving the homeowner a chance to “cure their default.” It is in everyone’s interest for the homeowner to catch up if possible.

We never want to see an innocent party “accidentally” evicted from a home. The legal system has evolved so this has become a “legal impossibility.” Imagine returning home from work or vacation to find the front door padlocked, the belongings strewn all over the block, a big orange sticker screaming “FORECLOSED” on the garage door, with an auction sign in the front lawn. Now imagine that this occurred even though you are not in default or even delinquent on payments. Thanks to the robosigning banks, this legal impossibility has happened repeatedly, even to homeowners who paid cash for their houses and had no mortgages. Imagine that — foreclosed with no mortgage.

Before any foreclosure can proceed, a lender must run through a checklist of specifics for the court to move forward. This review can take 45 to 120 minutes per file and addresses, for instance:

●When was the original loan made, and for how much?

●Who is the borrower? Who is the original lender?

●What is the address of the property?

●Which bank holds the mortgage note? Was the note transferred? When?

●When was the last payment made?

●How much is owed on the loan?

●Was the borrower notified of the delinquency? Default?

●Has the borrower been served notice? When, where and how?

Banks review these details to make sure there was not an administrative error. (Oops! We applied payments to wrong account!)

The banker who reviewed these files fills out and signs an affidavit, which is then notarized. It is the written equivalent of sworn testimony in court. Judges take affidavits extremely seriously. False affidavits bypass the entire fact-finding and legal process, and the result can be a miscarriage of justice. Anyone who lies on one commits perjury, a felony punishable by jail time.

At least, they used to get jail time.

Before the settlement, we learned that nearly every aspect of the robosigned documents was false. None of the details were ever reviewed. The signatures attesting to the review of the documents were fabricated — made by someone other than the person whose name was on the document. Neither person — the supposed signatory to the document nor the hired forger — ever validated the facts of each case. All of the safeguards put in place to make sure foreclosures were done correctly and legally were bypassed. Even the notary stamps were bogus — they were not real, and not signed by a notary to validate that the signer and the signature matched.

It is an epic failure of law and a triumph for bank attorneys.

It will accomplish little of value, as I’ll explain. First, let’s recall what the “robosigning” foreclosure scandal was all about.

Foreclosure is an extremely serious issue in American jurisprudence. As a nation of laws with strong respect for property rights, we have always treated this process appropriately. After all, having a sheriff forcibly evict a family that typically made a down payment, moved into a home, lived there for some years, made payments, etc., is disruptive — for the family, the lender and the neighborhood.

Foreclosure laws vary from state to state. However, all are specific and precise as to the legal steps that must be followed, from the homeowner’s initial delinquency onward. There are benefits to giving the homeowner a chance to “cure their default.” It is in everyone’s interest for the homeowner to catch up if possible.

We never want to see an innocent party “accidentally” evicted from a home. The legal system has evolved so this has become a “legal impossibility.” Imagine returning home from work or vacation to find the front door padlocked, the belongings strewn all over the block, a big orange sticker screaming “FORECLOSED” on the garage door, with an auction sign in the front lawn. Now imagine that this occurred even though you are not in default or even delinquent on payments. Thanks to the robosigning banks, this legal impossibility has happened repeatedly, even to homeowners who paid cash for their houses and had no mortgages. Imagine that — foreclosed with no mortgage.

Before any foreclosure can proceed, a lender must run through a checklist of specifics for the court to move forward. This review can take 45 to 120 minutes per file and addresses, for instance:

●When was the original loan made, and for how much?

●Who is the borrower? Who is the original lender?

●What is the address of the property?

●Which bank holds the mortgage note? Was the note transferred? When?

●When was the last payment made?

●How much is owed on the loan?

●Was the borrower notified of the delinquency? Default?

●Has the borrower been served notice? When, where and how?

Banks review these details to make sure there was not an administrative error. (Oops! We applied payments to wrong account!)

The banker who reviewed these files fills out and signs an affidavit, which is then notarized. It is the written equivalent of sworn testimony in court. Judges take affidavits extremely seriously. False affidavits bypass the entire fact-finding and legal process, and the result can be a miscarriage of justice. Anyone who lies on one commits perjury, a felony punishable by jail time.

At least, they used to get jail time.

Before the settlement, we learned that nearly every aspect of the robosigned documents was false. None of the details were ever reviewed. The signatures attesting to the review of the documents were fabricated — made by someone other than the person whose name was on the document. Neither person — the supposed signatory to the document nor the hired forger — ever validated the facts of each case. All of the safeguards put in place to make sure foreclosures were done correctly and legally were bypassed. Even the notary stamps were bogus — they were not real, and not signed by a notary to validate that the signer and the signature matched.

February 25, 2012

Battle lines forming between MF Global customers, hedge funds

The MF Global saga could soon become a legal battle between hedge funds and the futures brokerage's shortchanged customers, with more than a billion dollars at stake.

As the investigation into the collapse of the Jon Corzine-led brokerage moves into more of a regulatory whodunnit than a criminal case, the guessing game centers on who the two court-appointed trustees overseeing MF Global's liquidation will sue to recoup money owed to customers of MF's broker-dealer unit and creditors of its parent.

Those decisions are not easy ones, legal experts say, and they could end up pitting hedge funds like David Tepper's Appaloosa Management and Paul Singer's Elliott Management - who own MF Global bonds - against brokerage customers trying to recover an estimated $1.6 billion shortfall in their accounts.

It's likely that James Giddens, the trustee in charge of recovering customer funds, and Louis Freeh, the trustee in charge of recovering money for parent creditors, will dispute the ownership of certain assets, said attorney Chris Ward, vice chair of Polsinelli Shughart's bankruptcy practice, who is not involved in the case.

A more complex battle could arise from the fact that both customers and bondholders claim priority for payouts from MF Global's general estate.

Customer groups have said that if efforts to recoup customer cash do not make them whole, they have a right under Commodity Futures Trading Commission regulations to demand payment from the parent company.

"Customers are going to claim they should be satisfied in entirety first before one penny goes to" MF Holdings' bond holders and other creditors, said Fred Grede, an attorney who served as trustee for fallen cash-management firm Sentinel Management Group.

But distressed debt investors like Elliott and Appaloosa, who scooped-up MF Global's bonds after the firm filed for bankruptcy on October 31, say bankruptcy laws paint a different picture, one giving them priority over customers for general estate payouts.

"I will not be surprised at all if sometime in the near future you find Freeh and Giddens as adversaries," said attorney Chris Dickerson, who is not involved in MF Global but represented defunct financial services firm Refco in its 2005 bankruptcy.

A spokeswoman for MF Global Holdings said Freeh will not know exactly how much creditors of the parent company are owed until claims are filed. The company has $650 million in senior debt and another $850 million in subordinated debt, the spokeswoman said.

PICKING A TARGET

Before any decision can be made on the order of payouts, Giddens and Freeh, the former FBI director, must think strategically about which deep-pocketed institutions to pursue.

Some of the likely litigation targets are MF Global's main trading partners, its primary banker JPMorganChase, and clearinghouses that processed last minute trades for MF Global as it spiraled towards bankruptcy. Another possibility is MF Global's own United Kingdom affiliate, where about $700 million in customer money is tied up.

But recovering any funds won't be easy.

"In terms of resources, the worst counterparty in the world to go up against in court is the government," said one bankruptcy lawyer, who asked not to be named due to relationships with firms that have a stake in the outcome of potential litigation. "The next is JP Morgan."

A spokeswoman for JPMorgan declined to comment on whether either of the trustees have indicated that litigation may be in the offing.

"We lost money too" from MF Global's collapse, JPMorgan spokeswoman Mary Sedarat said on Thursday. "We're doing everything we can to assist in the investigations."

Connecticut-based broker-dealer CRT Capital Group told investors in November, and again earlier this month, that if they were looking at buying MF Global securities, they should expect at least a two-to-three-year battle to reclaim funds.

"You may see go after low-hanging fruit first," said Ward. "Pursue cases that are easy, get money back into the estate, and give them a war chest to go after bigger claims later."

JPMorgan is likely to make a strong argument, at least on the customer side, that its financial dealings were not improper because it did not have a responsibility to analyze the legality of the transactions it was clearing, Ward said.

UK FACE-OFF

One source close to Freeh said claims against MF Global's UK entity may be the first to be dealt with, noting that much of the money that changed hands in the company's last days wound up at the UK unit.

The source, who asked for anonymity because Freeh is still formulating his litigation strategies, said the UK unit will also have its own claims against various counterparties, adding another layer of complexity to recovery efforts.

One particular dispute likely to wind up in court is the battle over the ownership of about $700 million being held in the UK subsidiary. The money is associated with the accounts of US customers who traded on UK exchanges, and US and UK laws are inconsistent on who has a right to those funds.

A Giddens spokesman acknowledged the likelihood of a court battle, saying "We are hoping we can reach an accommodation with the UK administrators, but it looks very tough."

Giddens has hired a U.K. law firm to advise it on that issue.

Giddens and Freeh may also target individual executives, including Corzine, who resigned on November 4, Dickerson said. Hedge funds that own MF Global bonds also include potential litigation against executives on their laundry list of avenues that could bring money back to creditors.

Reuters has previously reported that investigators are having trouble finding an element of criminal intent in MF Global's downfall.[ID:nL2E8D9IKR] But they can still bring cases for civil infractions like breach of fiduciary duty, Dickerson said, and, because most executives are covered by insurance policies, there may be plenty of money to be recouped from those lawsuits.

MF Global's bankruptcy is In re MF Global Holdings Ltd, U.S. Bankruptcy Court, Southern District of New York, No. 11-15059.

The broker-dealer liquidation case is In re MF Global Inc, U.S. Bankruptcy Court, Southern District of New York, No. 11-2790.

As the investigation into the collapse of the Jon Corzine-led brokerage moves into more of a regulatory whodunnit than a criminal case, the guessing game centers on who the two court-appointed trustees overseeing MF Global's liquidation will sue to recoup money owed to customers of MF's broker-dealer unit and creditors of its parent.

Those decisions are not easy ones, legal experts say, and they could end up pitting hedge funds like David Tepper's Appaloosa Management and Paul Singer's Elliott Management - who own MF Global bonds - against brokerage customers trying to recover an estimated $1.6 billion shortfall in their accounts.

It's likely that James Giddens, the trustee in charge of recovering customer funds, and Louis Freeh, the trustee in charge of recovering money for parent creditors, will dispute the ownership of certain assets, said attorney Chris Ward, vice chair of Polsinelli Shughart's bankruptcy practice, who is not involved in the case.

A more complex battle could arise from the fact that both customers and bondholders claim priority for payouts from MF Global's general estate.

Customer groups have said that if efforts to recoup customer cash do not make them whole, they have a right under Commodity Futures Trading Commission regulations to demand payment from the parent company.

"Customers are going to claim they should be satisfied in entirety first before one penny goes to" MF Holdings' bond holders and other creditors, said Fred Grede, an attorney who served as trustee for fallen cash-management firm Sentinel Management Group.

But distressed debt investors like Elliott and Appaloosa, who scooped-up MF Global's bonds after the firm filed for bankruptcy on October 31, say bankruptcy laws paint a different picture, one giving them priority over customers for general estate payouts.

"I will not be surprised at all if sometime in the near future you find Freeh and Giddens as adversaries," said attorney Chris Dickerson, who is not involved in MF Global but represented defunct financial services firm Refco in its 2005 bankruptcy.

A spokeswoman for MF Global Holdings said Freeh will not know exactly how much creditors of the parent company are owed until claims are filed. The company has $650 million in senior debt and another $850 million in subordinated debt, the spokeswoman said.

PICKING A TARGET

Before any decision can be made on the order of payouts, Giddens and Freeh, the former FBI director, must think strategically about which deep-pocketed institutions to pursue.

Some of the likely litigation targets are MF Global's main trading partners, its primary banker JPMorganChase, and clearinghouses that processed last minute trades for MF Global as it spiraled towards bankruptcy. Another possibility is MF Global's own United Kingdom affiliate, where about $700 million in customer money is tied up.

But recovering any funds won't be easy.

"In terms of resources, the worst counterparty in the world to go up against in court is the government," said one bankruptcy lawyer, who asked not to be named due to relationships with firms that have a stake in the outcome of potential litigation. "The next is JP Morgan."

A spokeswoman for JPMorgan declined to comment on whether either of the trustees have indicated that litigation may be in the offing.

"We lost money too" from MF Global's collapse, JPMorgan spokeswoman Mary Sedarat said on Thursday. "We're doing everything we can to assist in the investigations."

Connecticut-based broker-dealer CRT Capital Group told investors in November, and again earlier this month, that if they were looking at buying MF Global securities, they should expect at least a two-to-three-year battle to reclaim funds.

"You may see go after low-hanging fruit first," said Ward. "Pursue cases that are easy, get money back into the estate, and give them a war chest to go after bigger claims later."

JPMorgan is likely to make a strong argument, at least on the customer side, that its financial dealings were not improper because it did not have a responsibility to analyze the legality of the transactions it was clearing, Ward said.

UK FACE-OFF

One source close to Freeh said claims against MF Global's UK entity may be the first to be dealt with, noting that much of the money that changed hands in the company's last days wound up at the UK unit.

The source, who asked for anonymity because Freeh is still formulating his litigation strategies, said the UK unit will also have its own claims against various counterparties, adding another layer of complexity to recovery efforts.

One particular dispute likely to wind up in court is the battle over the ownership of about $700 million being held in the UK subsidiary. The money is associated with the accounts of US customers who traded on UK exchanges, and US and UK laws are inconsistent on who has a right to those funds.

A Giddens spokesman acknowledged the likelihood of a court battle, saying "We are hoping we can reach an accommodation with the UK administrators, but it looks very tough."

Giddens has hired a U.K. law firm to advise it on that issue.

Giddens and Freeh may also target individual executives, including Corzine, who resigned on November 4, Dickerson said. Hedge funds that own MF Global bonds also include potential litigation against executives on their laundry list of avenues that could bring money back to creditors.

Reuters has previously reported that investigators are having trouble finding an element of criminal intent in MF Global's downfall.[ID:nL2E8D9IKR] But they can still bring cases for civil infractions like breach of fiduciary duty, Dickerson said, and, because most executives are covered by insurance policies, there may be plenty of money to be recouped from those lawsuits.

MF Global's bankruptcy is In re MF Global Holdings Ltd, U.S. Bankruptcy Court, Southern District of New York, No. 11-15059.

The broker-dealer liquidation case is In re MF Global Inc, U.S. Bankruptcy Court, Southern District of New York, No. 11-2790.

February 24, 2012

Ex-Goldman analyst writes white collar crime tale

"The Darlings" tells a fictional tale about the downfall of a hedge fund and the wealthy family that owns it during Wall Street's 2008 meltdown, but many aspects of the novel are drawn straight from author Cristina Alger's reality.

As a former Goldman Sachs analyst and bankruptcy attorney at a white-shoe law firm in New York, Alger knew that the twists and turns that led to many a Wall Street fiasco could make for a fascinating story.

"It's easy to see finance as something that happens in a conference room, but white-collar crime is fascinating," Alger told Reuters. "No one's dying or no cars are blowing up, but it's incredibly fast-paced and interesting and complex."

"The Darlings", which is released on Monday in the United States, is one of the first works of fiction centered on the events of the 2008 financial crisis.

The book begins with an apparent suicide, which sets off a series of investigations and cover-ups by a web of characters that includes lawyers, financiers, government officials and journalists.

The dynamics and loyalties of the blue-blooded Darling family that runs the hedge fund, founded by patriarch and billionaire Carter Darling, are also thrown into tumult as the foundation of the family's wealth and status is threatened.

WITNESSING CORPORATE SCANDALS

Alger, 31, knows a thing or two about family businesses: her family founded prominent New York investment firm Fred Alger Management. In addition to her professional experience, she said that she also drew on her family background to write the book.

"I grew up going to my dad's office, and family dinners were filled with chatter about work life," she said. "One of the things I tried to draw from in 'The Darlings' was the sense that the whole family was involved in the business, and the demise of the business in their case was really like the demise of the family as a whole."

As Alger tried to make sense of the corporate scandals she witnessed as an attorney, she found that chalking up bad behavior to mere greed didn't quite get to the root of such scandals. As she pondered what could drive some investors to such extreme corruption, she found her thoughts circling back to family loyalties.

"One of the fun parts of writing the book for me was trying to get into the minds of people who caused huge amounts of damage professionally, and try to understand what their motivations were for the way they acted," she said.

The urge to protect and provide for children, parents, and spouses factor powerfully into the professional decisions of all characters in "The Darlings", from CEO Carter Darling to whistle-blowing secretary, Yvonne.

"I had deep affection for all my characters, and didn't like to see anyone as purely bad or purely good," she said. "People act well, and people act badly, and they're all doing it for the best interest of their families."

Alger said that another element in the collapse of firms such as Lehman Brothers and AIG was the widespread bending of rules by those high up in Wall Street's steel towers. This is reflected in the story as the Darling family scrambles to perform damage control once they become aware of the firm's problems.

"I think there were two sets of rules that were operating during that period," Alger said. "There were the rules that were on the books, and then there were the rules that were market-wide practice, and what a lot of people realized was that market-wide practice wasn't always legal."

Post-2008 crisis, Alger said she believed that real-life CEO's like that of Carter Darling seemed to be under more scrutiny, and hoped that any increased attention would provide a check on power, along with better regulation and increased market transparency.

As a former Goldman Sachs analyst and bankruptcy attorney at a white-shoe law firm in New York, Alger knew that the twists and turns that led to many a Wall Street fiasco could make for a fascinating story.

"It's easy to see finance as something that happens in a conference room, but white-collar crime is fascinating," Alger told Reuters. "No one's dying or no cars are blowing up, but it's incredibly fast-paced and interesting and complex."

"The Darlings", which is released on Monday in the United States, is one of the first works of fiction centered on the events of the 2008 financial crisis.

The book begins with an apparent suicide, which sets off a series of investigations and cover-ups by a web of characters that includes lawyers, financiers, government officials and journalists.

The dynamics and loyalties of the blue-blooded Darling family that runs the hedge fund, founded by patriarch and billionaire Carter Darling, are also thrown into tumult as the foundation of the family's wealth and status is threatened.

WITNESSING CORPORATE SCANDALS

Alger, 31, knows a thing or two about family businesses: her family founded prominent New York investment firm Fred Alger Management. In addition to her professional experience, she said that she also drew on her family background to write the book.

"I grew up going to my dad's office, and family dinners were filled with chatter about work life," she said. "One of the things I tried to draw from in 'The Darlings' was the sense that the whole family was involved in the business, and the demise of the business in their case was really like the demise of the family as a whole."

As Alger tried to make sense of the corporate scandals she witnessed as an attorney, she found that chalking up bad behavior to mere greed didn't quite get to the root of such scandals. As she pondered what could drive some investors to such extreme corruption, she found her thoughts circling back to family loyalties.

"One of the fun parts of writing the book for me was trying to get into the minds of people who caused huge amounts of damage professionally, and try to understand what their motivations were for the way they acted," she said.

The urge to protect and provide for children, parents, and spouses factor powerfully into the professional decisions of all characters in "The Darlings", from CEO Carter Darling to whistle-blowing secretary, Yvonne.

"I had deep affection for all my characters, and didn't like to see anyone as purely bad or purely good," she said. "People act well, and people act badly, and they're all doing it for the best interest of their families."

Alger said that another element in the collapse of firms such as Lehman Brothers and AIG was the widespread bending of rules by those high up in Wall Street's steel towers. This is reflected in the story as the Darling family scrambles to perform damage control once they become aware of the firm's problems.

"I think there were two sets of rules that were operating during that period," Alger said. "There were the rules that were on the books, and then there were the rules that were market-wide practice, and what a lot of people realized was that market-wide practice wasn't always legal."

Post-2008 crisis, Alger said she believed that real-life CEO's like that of Carter Darling seemed to be under more scrutiny, and hoped that any increased attention would provide a check on power, along with better regulation and increased market transparency.

February 23, 2012

55 Interesting Facts About The U.S. Economy In 2012

How is the U.S. economy doing in 2012? Unfortunately, it is not doing nearly as well as the mainstream media would have you believe. Yes, things have stabilized for the moment but this bubble of false hope will not last for long. The long-term trends that are ripping our economy and our financial system to shreds continue unabated. When you step back and look at the broader picture, it is hard to deny that we are in really bad shape and that things are rapidly getting worse. Later on in this article you will find a list of interesting facts that show the true state of the U.S. economy. Hopefully many of you will find this list to be a useful tool that you can share with your family and friends. Each day the foundations of our economy crumble a little bit more, and we need to wake up as many Americans as we can to what is really going on while there is still time. We have accumulated way too much debt, we consume far more wealth than we produce, millions of our jobs are being shipped overseas, our big cities are decaying, family budgets are being squeezed more than ever, poverty is rampant and we have raised several generations of Americans that expect the government to fix all of their problems. The U.S. economy is at a crossroads, and the decisions that the American people make in 2012 are going to be incredibly important.

The statistics listed below are presented without much commentary. They pretty much speak for themselves.

After reading this list, it will be hard for anyone to argue that we are on the right track.

The following are 55 interesting facts about the U.S. economy in 2012....

#1 As you read this, there are more than 6 million mortgages in the United States that are overdue.

#2 In January, U.S. home prices were the lowest that they have been in more than a decade.

#3 In Florida right now, some drivers are paying nearly 6 dollars for a gallon of gas.

#4 On average, you could buy about 10 gallons of gas for an hour of work back in the mid-90s. Today, the average hour of work will get you less than 6 gallons of gas.

#5 Sadly, 43 percent of all American families spend more than they earn each year.

#6 According to Gallup, the unemployment rate was at 8.3% in mid-January but rose to 9.0% in mid-February.

#7 The percentage of working age Americans that have jobs is not increasing. The employment to population ratio has stayed very steady (hovering between 58% and 59%) since the beginning of 2010.

#8 If you gathered together all of the workers that are "officially" unemployed in the United States into one nation, they would constitute the 68th largest country in the entire world.

#9 When Barack Obama first took office, the number of "long-term unemployed workers" in the United States was approximately 2.6 million. Today, that number is sitting at 5.6 million.

#10 The average duration of unemployment in the United States is hovering close to an all-time record high.

#11 According to Reuters, approximately 23.7 million American workers are either unemployed or underemployed right now.

#12 There are about 88 million working age Americans that are not employed and that are not looking for employment. That is an all-time record high.

#13 According to CareerBuilder, only 23 percent of American companies plan to hire more employees in 2012.

#14 Back in the year 2000, about 20 percent of all jobs in America were manufacturing jobs. Today, about 5 percent of all jobs in America are manufacturing jobs.

#15 The United States has lost an average of approximately 50,000 manufacturing jobs a month since China joined the World Trade Organization in 2001.

#16 Amazingly, more than 56,000 manufacturing facilities in the United States have been shut down since 2001.

#17 According to author Paul Osterman, about 20 percent of all U.S. adults are currently working jobs that pay poverty-level wages.

#18 During the Obama administration, worker health insurance costs have risen by 23 percent.

#19 An all-time record 49.9 million Americans do not have any health insurance at all at this point, and the percentage of Americans covered by employer-based health plans has fallen for 11 years in a row.

#20 According to the New York Times, approximately 100 million Americans are either living in poverty or in "the fretful zone just above it".

#21 In the United States today, corporate profits are at an all-time high. The percentage of Americans that are living in "extreme poverty" is also at an all-time high according to the U.S. Census Bureau.

#22 In the United States today, the wealthiest one percent of all Americans have a greater net worth than the bottom 90 percent combined.

#23 The poorest 50 percent of all Americans now collectively own just 2.5% of all the wealth in the United States.

#24 The number of children living in poverty in the state of California has increased by 30 percent since 2007.

#25 According to the National Center for Children in Poverty, 36.4% of all children that live in Philadelphia are living in poverty, 40.1% of all children that live in Atlanta are living in poverty, 52.6% of all children that live in Cleveland are living in poverty and 53.6% of all children that live in Detroit are living in poverty.

#26 Since Barack Obama entered the White House, the number of Americans on food stamps has increased from 32 million to 46 million.

#27 As the economy has slowed down, so has the number of marriages. According to a Pew Research Center analysis, only 51 percent of all Americans that are at least 18 years old are currently married. Back in 1960, 72 percent of all U.S. adults were married.

#28 In 1984, the median net worth of households led by someone 65 or older was 10 times larger than the median net worth of households led by someone 35 or younger. Today, the median net worth of households led by someone 65 or older is 47 times larger than the median net worth of households led by someone 35 or younger.

#29 If you can believe it, 37 percent of all U.S. households that are led by someone under the age of 35 have a net worth of zero or less than zero.

#30 After adjusting for inflation, U.S. college students are borrowing about twice as much money as they did a decade ago.

#31 According to the Student Loan Debt Clock, total student loan debt in the United States will surpass the 1 trillion dollar mark at some point in 2012. If you went out right now and starting spending one dollar every single second, it would take you more than 31,000 years to spend one trillion dollars.

#32 Today, 46% of all Americans carry a credit card balance from month to month.

#33 Incredibly, one out of every seven Americans has at least 10 credit cards.

#34 The average interest rate on a credit card that is carrying a balance is now up to 13.10 percent.

#35 Of the U.S. households that do have credit card debt, the average amount of credit card debt is an astounding $15,799.

#36 Overall, Americans are carrying a grand total of $798 billion in credit card debt. If you were alive when Jesus was born and you spent a million dollars every single day since then, you still would not have spent $798 billion by now.

#37 It may be hard to believe, but the truth is that consumer debt in America has increased by a whopping 1700% since 1971.

#38 At this point, about 70 percent of all auto purchases in the United States involve an auto loan.

#39 In the United States today, 45 percent of all auto loans are made to subprime borrowers.

#40 Mortgage debt as a percentage of GDP has more than tripled since 1955.

#41 According to a recent study conducted by the BlackRock Investment Institute, the ratio of household debt to personal income in the United States is now 154 percent.

#42 To get the same purchasing power that you got out of $20.00 back in 1970 you would have to have more than $116 today.

#43 When Barack Obama first took office, an ounce of gold was going for about $850. Today an ounce of gold costs more than $1700 an ounce.

#44 The number of Americans that are not paying federal incomes taxes is at an all-time high.

#45 A staggering 48.5% of all Americans live in a household that receives some form of government benefits. Back in 1983, that number was below 30 percent.

#46 The amount of money that the federal government gives directly to Americans has increased by 32 percent since Barack Obama entered the White House.

#47 During 2012, the U.S. government must roll over nearly 3 trillion dollars of old debt.

#48 The U.S. debt to GDP ratio has now reached 101 percent.

#49 At the moment, the U.S. national debt is sitting at a grand total of $15,419,800,222,325.15.

#50 The U.S. national debt is now more than 22 times larger than it was when Jimmy Carter became president.

#51 During the Obama administration, the U.S. government has accumulated more debt than it did from the time that George Washington took office to the time that Bill Clinton took office.

#52 If the federal government began right at this moment to repay the U.S. national debt at a rate of one dollar per second, it would take over 440,000 years to pay off the national debt.

#53 If Bill Gates gave every single penny of his fortune to the U.S. government, it would only cover the U.S. budget deficit for about 15 days.

#54 Right now, the U.S. national debt is increasing by about 150 million dollars every single hour.

#55 Spending by the federal government accounted for about 2 percent of GDP back in 1800. It accounted for 23.8 percent in 2011, and according to former U.S. Comptroller General David M. Walker, it will account for 36.8 percent of GDP by 2040.

Bad news, eh?

But it isn't just our economy that is decaying.

We are witnessing a tremendous amount of social decay as well. As I wrote about the other day, America is rapidly decomposing right in front of our eyes.

When the water level of a river drops far enough, it will reveal rocks that have been hidden from view for a very long time. Well, a similar thing is happening in America right now. For decades, our debt-fueled prosperity has masked a lot of the social decay that has been going on.

But now that our prosperity is evaporating, a lot of frightening stuff is being revealed.

Unfortunately, another major financial crisis is rapidly approaching and economic conditions in the United States are going to get a lot worse.

So what is our country going to look like when that happens?

That is a very good question.

The statistics listed below are presented without much commentary. They pretty much speak for themselves.

After reading this list, it will be hard for anyone to argue that we are on the right track.

The following are 55 interesting facts about the U.S. economy in 2012....

#1 As you read this, there are more than 6 million mortgages in the United States that are overdue.

#2 In January, U.S. home prices were the lowest that they have been in more than a decade.

#3 In Florida right now, some drivers are paying nearly 6 dollars for a gallon of gas.

#4 On average, you could buy about 10 gallons of gas for an hour of work back in the mid-90s. Today, the average hour of work will get you less than 6 gallons of gas.

#5 Sadly, 43 percent of all American families spend more than they earn each year.

#6 According to Gallup, the unemployment rate was at 8.3% in mid-January but rose to 9.0% in mid-February.

#7 The percentage of working age Americans that have jobs is not increasing. The employment to population ratio has stayed very steady (hovering between 58% and 59%) since the beginning of 2010.

#8 If you gathered together all of the workers that are "officially" unemployed in the United States into one nation, they would constitute the 68th largest country in the entire world.

#9 When Barack Obama first took office, the number of "long-term unemployed workers" in the United States was approximately 2.6 million. Today, that number is sitting at 5.6 million.

#10 The average duration of unemployment in the United States is hovering close to an all-time record high.

#11 According to Reuters, approximately 23.7 million American workers are either unemployed or underemployed right now.

#12 There are about 88 million working age Americans that are not employed and that are not looking for employment. That is an all-time record high.

#13 According to CareerBuilder, only 23 percent of American companies plan to hire more employees in 2012.

#14 Back in the year 2000, about 20 percent of all jobs in America were manufacturing jobs. Today, about 5 percent of all jobs in America are manufacturing jobs.

#15 The United States has lost an average of approximately 50,000 manufacturing jobs a month since China joined the World Trade Organization in 2001.

#16 Amazingly, more than 56,000 manufacturing facilities in the United States have been shut down since 2001.

#17 According to author Paul Osterman, about 20 percent of all U.S. adults are currently working jobs that pay poverty-level wages.

#18 During the Obama administration, worker health insurance costs have risen by 23 percent.

#19 An all-time record 49.9 million Americans do not have any health insurance at all at this point, and the percentage of Americans covered by employer-based health plans has fallen for 11 years in a row.

#20 According to the New York Times, approximately 100 million Americans are either living in poverty or in "the fretful zone just above it".

#21 In the United States today, corporate profits are at an all-time high. The percentage of Americans that are living in "extreme poverty" is also at an all-time high according to the U.S. Census Bureau.

#22 In the United States today, the wealthiest one percent of all Americans have a greater net worth than the bottom 90 percent combined.

#23 The poorest 50 percent of all Americans now collectively own just 2.5% of all the wealth in the United States.

#24 The number of children living in poverty in the state of California has increased by 30 percent since 2007.

#25 According to the National Center for Children in Poverty, 36.4% of all children that live in Philadelphia are living in poverty, 40.1% of all children that live in Atlanta are living in poverty, 52.6% of all children that live in Cleveland are living in poverty and 53.6% of all children that live in Detroit are living in poverty.

#26 Since Barack Obama entered the White House, the number of Americans on food stamps has increased from 32 million to 46 million.

#27 As the economy has slowed down, so has the number of marriages. According to a Pew Research Center analysis, only 51 percent of all Americans that are at least 18 years old are currently married. Back in 1960, 72 percent of all U.S. adults were married.

#28 In 1984, the median net worth of households led by someone 65 or older was 10 times larger than the median net worth of households led by someone 35 or younger. Today, the median net worth of households led by someone 65 or older is 47 times larger than the median net worth of households led by someone 35 or younger.

#29 If you can believe it, 37 percent of all U.S. households that are led by someone under the age of 35 have a net worth of zero or less than zero.

#30 After adjusting for inflation, U.S. college students are borrowing about twice as much money as they did a decade ago.

#31 According to the Student Loan Debt Clock, total student loan debt in the United States will surpass the 1 trillion dollar mark at some point in 2012. If you went out right now and starting spending one dollar every single second, it would take you more than 31,000 years to spend one trillion dollars.

#32 Today, 46% of all Americans carry a credit card balance from month to month.

#33 Incredibly, one out of every seven Americans has at least 10 credit cards.

#34 The average interest rate on a credit card that is carrying a balance is now up to 13.10 percent.

#35 Of the U.S. households that do have credit card debt, the average amount of credit card debt is an astounding $15,799.

#36 Overall, Americans are carrying a grand total of $798 billion in credit card debt. If you were alive when Jesus was born and you spent a million dollars every single day since then, you still would not have spent $798 billion by now.

#37 It may be hard to believe, but the truth is that consumer debt in America has increased by a whopping 1700% since 1971.

#38 At this point, about 70 percent of all auto purchases in the United States involve an auto loan.

#39 In the United States today, 45 percent of all auto loans are made to subprime borrowers.

#40 Mortgage debt as a percentage of GDP has more than tripled since 1955.

#41 According to a recent study conducted by the BlackRock Investment Institute, the ratio of household debt to personal income in the United States is now 154 percent.

#42 To get the same purchasing power that you got out of $20.00 back in 1970 you would have to have more than $116 today.

#43 When Barack Obama first took office, an ounce of gold was going for about $850. Today an ounce of gold costs more than $1700 an ounce.

#44 The number of Americans that are not paying federal incomes taxes is at an all-time high.

#45 A staggering 48.5% of all Americans live in a household that receives some form of government benefits. Back in 1983, that number was below 30 percent.

#46 The amount of money that the federal government gives directly to Americans has increased by 32 percent since Barack Obama entered the White House.

#47 During 2012, the U.S. government must roll over nearly 3 trillion dollars of old debt.

#48 The U.S. debt to GDP ratio has now reached 101 percent.

#49 At the moment, the U.S. national debt is sitting at a grand total of $15,419,800,222,325.15.

#50 The U.S. national debt is now more than 22 times larger than it was when Jimmy Carter became president.

#51 During the Obama administration, the U.S. government has accumulated more debt than it did from the time that George Washington took office to the time that Bill Clinton took office.

#52 If the federal government began right at this moment to repay the U.S. national debt at a rate of one dollar per second, it would take over 440,000 years to pay off the national debt.

#53 If Bill Gates gave every single penny of his fortune to the U.S. government, it would only cover the U.S. budget deficit for about 15 days.

#54 Right now, the U.S. national debt is increasing by about 150 million dollars every single hour.

#55 Spending by the federal government accounted for about 2 percent of GDP back in 1800. It accounted for 23.8 percent in 2011, and according to former U.S. Comptroller General David M. Walker, it will account for 36.8 percent of GDP by 2040.

Bad news, eh?

But it isn't just our economy that is decaying.

We are witnessing a tremendous amount of social decay as well. As I wrote about the other day, America is rapidly decomposing right in front of our eyes.

When the water level of a river drops far enough, it will reveal rocks that have been hidden from view for a very long time. Well, a similar thing is happening in America right now. For decades, our debt-fueled prosperity has masked a lot of the social decay that has been going on.

But now that our prosperity is evaporating, a lot of frightening stuff is being revealed.

Unfortunately, another major financial crisis is rapidly approaching and economic conditions in the United States are going to get a lot worse.

So what is our country going to look like when that happens?

That is a very good question.

February 22, 2012

As US Debt To GDP Passes 101%, The Global Debt Ponzi Enters Its Final Stages

Today, without much fanfare, US debt to GDP hit 101% with the latest issuance of $32 billion in 2 Year Bonds. If the moment when this ratio went from double to triple digits is still fresh in readers minds, is because it is: total debt hit and surpassed the most recently revised Q4 GDP on January 30, or just three weeks ago. Said otherwise, it has taken the US 21 days to add a full percentage point to this most critical of debt sustainability ratios: but fear not, with just under $1 trillion in new debt issuance on deck in the next 9 months, we will be at 110% in no time. Still, this trend made us curious to see who has been buying (and selling) US debt over the past year. The results are somewhat surprising. As the chart below, which highlights some of the biggest and most notable holders of US paper, shows, in the period December 31, 2010 to December 31, 2011, there have been two very distinct shifts: those who are going all in on the ponzi, and those who are gradually shifting away from the greenback, and just as quietly, and without much fanfare of their own, reinvesting their trade surplus in something distinctly other than US paper. The latter two: China and Russia, as we have noted in the past. Yet these are more than offset by... well, we'll let the readers look at the chart below based on TIC data and figure out it.

That the Fed is now actively monetizing US debt is beyond dispute (although some semantic holdouts remain - we are quite happy for them). Alas, with China, which has traditionally been the biggest buyer of US paper, no longer buying Treasurys, we are confident that the Fed will have no choice but to be dragged kicking and screaming once again into the fray, especially since traditional buyers of paper, even when allowing for exponential repo market leveraging (and someone please look at what is going on in the BoNY, State Street sponsored $15 trillion quicksand of repo'ed securities, which is the biggest black hole in the shadow banking system and will be the next pillar of the ponzi system to collapse) will be unable to keep up with US issuance. Especially since Primary Dealers already saw their Treasury holding rise to an all time high in the past week, and are loaded to the gills with US paper. So who is buying? Why Japan and the UK.

Japan and the UK? Hmm, if these two names sound oddly familiar, allow us to refresh one's memory. Behold the pristine leverage condition of both these two countries, in all its glory.

Hint: look at the far left.

So somehow the world's two most indebted countries (recall that Japan is about to in total pass 1 quadrillion debt) are out there and buying up the biggest amount of US debt (after the Fed of course)? Sorry, but while we are amusing by this attempt by the global ponzi regime to keep itself alive (even as Russia and China prudently step aside from the mauling that is sure to follow), whereby the most indebted nations keep buying each other's debt in the most transparent and potentially deadly shell game in history, we are also confident this is unsustainable. Which means the Fed will have no choice but to step in. And since when it comes to the capital markets, the ride up is over since we have now crossed the point where incremental profits are drowned by incremental input costs (thank you $106 WTI), the Fed now has just one mandate: to keep the US fiscal machine well-greased by buying up US debt at zero (and beginning in May negative) rates, through wanton monetization. 2012 may prove to be quite eventful after all.

That the Fed is now actively monetizing US debt is beyond dispute (although some semantic holdouts remain - we are quite happy for them). Alas, with China, which has traditionally been the biggest buyer of US paper, no longer buying Treasurys, we are confident that the Fed will have no choice but to be dragged kicking and screaming once again into the fray, especially since traditional buyers of paper, even when allowing for exponential repo market leveraging (and someone please look at what is going on in the BoNY, State Street sponsored $15 trillion quicksand of repo'ed securities, which is the biggest black hole in the shadow banking system and will be the next pillar of the ponzi system to collapse) will be unable to keep up with US issuance. Especially since Primary Dealers already saw their Treasury holding rise to an all time high in the past week, and are loaded to the gills with US paper. So who is buying? Why Japan and the UK.

Japan and the UK? Hmm, if these two names sound oddly familiar, allow us to refresh one's memory. Behold the pristine leverage condition of both these two countries, in all its glory.

Hint: look at the far left.

So somehow the world's two most indebted countries (recall that Japan is about to in total pass 1 quadrillion debt) are out there and buying up the biggest amount of US debt (after the Fed of course)? Sorry, but while we are amusing by this attempt by the global ponzi regime to keep itself alive (even as Russia and China prudently step aside from the mauling that is sure to follow), whereby the most indebted nations keep buying each other's debt in the most transparent and potentially deadly shell game in history, we are also confident this is unsustainable. Which means the Fed will have no choice but to step in. And since when it comes to the capital markets, the ride up is over since we have now crossed the point where incremental profits are drowned by incremental input costs (thank you $106 WTI), the Fed now has just one mandate: to keep the US fiscal machine well-greased by buying up US debt at zero (and beginning in May negative) rates, through wanton monetization. 2012 may prove to be quite eventful after all.

February 21, 2012

Presenting The Full Greek (Un)Sustainability Analysis - Take It Away German Media

You read headlines that Greece is saved (in a carbon copy release from July 21). Now read the truth behind the lies - presenting the 9 page (so it's brief enough) Greek sustainability (or lack thereof) analysis.

Here is the punchline:

The debt trajectory is extremely sensitive to program delays, suggesting that the program could be accident prone, and calling into question sustainability (Table 2). Under the tailored scenario described above, the debt ratio would peak at 178 percent of GDP in 2015. Once growth did recover, fiscal policy achieved its target, and privatization picked up, the debt would begin to slowly decline. Debt to GDP would fall to around 160 percent of GDP by 2020, well above the target of about 120 percent of GDP set by European leaders. Financing needs through 2020 would amount to perhaps €245 billion. Under the assumption that stronger growth could follow on the eventual elimination of the competiveness gap, the debt ratio would slowly converge to that in the baseline, but likely only in the late 2020s. With debt ratios so high in the next decade, smaller shocks would produce unsustainable dynamics, leaving the program highly accident-prone.

And if the downside case means the country is about to need 100% of its GDP in additional funding needs, the reality is that this number most likely be 200%, bringing the total bailout bill for Greece to nearly 3x its GDP!

Becase wait, there's more: the downside case assumes -1.0% GDP decline in 2013. As a reminder, in Q4 Greek GDP imploded by -7%! Somehow we are to believe that within a year, the country will not only turn around its economy, which is foundering courtesy of infinite austerity and striking tax collectors, but almost generate growth???

The German media is about to have a field day.

Here is the punchline:

The debt trajectory is extremely sensitive to program delays, suggesting that the program could be accident prone, and calling into question sustainability (Table 2). Under the tailored scenario described above, the debt ratio would peak at 178 percent of GDP in 2015. Once growth did recover, fiscal policy achieved its target, and privatization picked up, the debt would begin to slowly decline. Debt to GDP would fall to around 160 percent of GDP by 2020, well above the target of about 120 percent of GDP set by European leaders. Financing needs through 2020 would amount to perhaps €245 billion. Under the assumption that stronger growth could follow on the eventual elimination of the competiveness gap, the debt ratio would slowly converge to that in the baseline, but likely only in the late 2020s. With debt ratios so high in the next decade, smaller shocks would produce unsustainable dynamics, leaving the program highly accident-prone.

And if the downside case means the country is about to need 100% of its GDP in additional funding needs, the reality is that this number most likely be 200%, bringing the total bailout bill for Greece to nearly 3x its GDP!

Becase wait, there's more: the downside case assumes -1.0% GDP decline in 2013. As a reminder, in Q4 Greek GDP imploded by -7%! Somehow we are to believe that within a year, the country will not only turn around its economy, which is foundering courtesy of infinite austerity and striking tax collectors, but almost generate growth???

The German media is about to have a field day.

February 20, 2012

MF Global sold assets to Goldman before collapse: sources

MF Global unloaded hundreds of millions of dollars' worth of securities to Goldman Sachs in the days leading up to its collapse, according to two former MF Global employees with direct knowledge of the transactions. But it did not immediately receive payment from its clearing firm and lender, JPMorgan Chase & Co (JPM.N), one of the sources said.

The sale of securities to Goldman occurred on October 27, just days before MF Global Holdings Ltd (MFGLQ.PK) filed for bankruptcy on October 31, the ex-employees said. One of the employees said the transaction was cleared with JPMorgan Chase.

At the same time MF Global, which was run by former Goldman Sachs head Jon Corzine, was selling securities to Goldman to raise badly needed cash, the futures firm was also drawing down a $1.2 billion revolving line of credit it had with JPMorgan, according to one of the former MF Global employees.

JPMorgan spokeswoman Mary Sedarat said the bank did not withold money because of the line of credit. She declined further comment on details of the transactions.

JPMorgan has fought aggressively in bankruptcy court to protect its interests, and received a lien on some of MF Global's assets in exchange for granting the firm $8 million to fund its bankruptcy costs. The lien puts JPMorgan's interests ahead of MF Global customers who have not yet received an estimated $900 million worth of money from their accounts, which remain frozen as regulators search for missing funds.

The hastily crafted transactions and the seeming inability of MF Global to recoup some of the money in the sale to Goldman may start to explain why so much money remains unaccounted for at the futures firm.

It is unclear what type of assets Goldman bought from MF Global, but the securities were worth hundreds of millions of dollars, the former employees said. The sources spoke on the condition of anonymity.

The Wall Street Journal previously reported that George Soros' fund was a buyer of securities sold by MF Global, scooping-up some of its European sovereign debt at a deep discount. Panic among investors and clients about MF Global's $6.3 billion bet on European sovereign bonds led to its demise.

Corzine, who was CEO of MF Global at the time of the collapse, headed Goldman Sachs from 1994 to 1999 before being ousted after a power struggle with co-CEO Henry Paulson.

Corzine and other top MF Global executives reached out in desperation to Goldman Sachs Group Inc (GS.N) and JPMorgan, as well as Jefferies Group Inc (JEF.N) Barclays Plc (BARC.L), Citigroup Inc (C.N), Deutsche Bank AG (DBKGn.DE), Macquarie Group Ltd (MQG.AX), State Street Corp (STT.N) and Wells Fargo & Co (WFC.N), as potential buyers in its final days as the firm teetered toward collapse, Reuters earlier reported.

The sale of securities to Goldman occurred on October 27, just days before MF Global Holdings Ltd (MFGLQ.PK) filed for bankruptcy on October 31, the ex-employees said. One of the employees said the transaction was cleared with JPMorgan Chase.

At the same time MF Global, which was run by former Goldman Sachs head Jon Corzine, was selling securities to Goldman to raise badly needed cash, the futures firm was also drawing down a $1.2 billion revolving line of credit it had with JPMorgan, according to one of the former MF Global employees.

JPMorgan spokeswoman Mary Sedarat said the bank did not withold money because of the line of credit. She declined further comment on details of the transactions.

JPMorgan has fought aggressively in bankruptcy court to protect its interests, and received a lien on some of MF Global's assets in exchange for granting the firm $8 million to fund its bankruptcy costs. The lien puts JPMorgan's interests ahead of MF Global customers who have not yet received an estimated $900 million worth of money from their accounts, which remain frozen as regulators search for missing funds.

The hastily crafted transactions and the seeming inability of MF Global to recoup some of the money in the sale to Goldman may start to explain why so much money remains unaccounted for at the futures firm.

It is unclear what type of assets Goldman bought from MF Global, but the securities were worth hundreds of millions of dollars, the former employees said. The sources spoke on the condition of anonymity.

The Wall Street Journal previously reported that George Soros' fund was a buyer of securities sold by MF Global, scooping-up some of its European sovereign debt at a deep discount. Panic among investors and clients about MF Global's $6.3 billion bet on European sovereign bonds led to its demise.

Corzine, who was CEO of MF Global at the time of the collapse, headed Goldman Sachs from 1994 to 1999 before being ousted after a power struggle with co-CEO Henry Paulson.

Corzine and other top MF Global executives reached out in desperation to Goldman Sachs Group Inc (GS.N) and JPMorgan, as well as Jefferies Group Inc (JEF.N) Barclays Plc (BARC.L), Citigroup Inc (C.N), Deutsche Bank AG (DBKGn.DE), Macquarie Group Ltd (MQG.AX), State Street Corp (STT.N) and Wells Fargo & Co (WFC.N), as potential buyers in its final days as the firm teetered toward collapse, Reuters earlier reported.

February 19, 2012

Goldman Analyst Is Said to Face Insider Trading Inquiry

A Goldman Sachs stock analyst has been drawn into the government’s sweeping investigation into insider trading at hedge funds.

Federal investigators are examining whether Henry King, a senior technology industry analyst for Goldman based in Asia, provided confidential information to the bank’s hedge fund clients, according to a person with direct knowledge of the matter who requested anonymity because he was not authorized to discuss it publicly.

Mr. King recently took a leave of absence from Goldman, according to this person.

Mr. King could not be reached for comment. A spokesman for the firm declined to comment. The Federal Bureau of Investigation declined to comment.

The Wall Street Journal reported earlier on Mr. King’s role in the investigation.

Goldman has figured prominently in the government’s insider trading inquiry. Last year, federal prosecutors charged Rajat K. Gupta, a former director of Goldman, with leaking secret boardroom discussions to Raj Rajaratnam, the former head of the Galleon Group hedge fund who is serving an 11-year prison term after a jury convicted him of insider trading crimes last May.

Mr. Gupta has denied the charges. His trial is set to begin in May.

During pretrial hearings in Mr. Gupta’s case, it emerged that there was a second insider at Goldman who was said to have leaked Mr. Rajaratnam illegal stock tips. A letter filed with the court by federal prosecutors in the Gupta case said that another unidentified Goldman executive had provided Mr. Rajaratnam with confidential information.

Judge Jed S. Rakoff, the judge presiding over the case, agreed to keep the content of the leaks under seal because they were unrelated to the charges against Mr. Gupta.