From Big State a Call for Small Banks ... An annual report from a regional Federal Reserve bank is typically a collection of banalities and clichés with some pictures of local worthies who serve on the board. And so it is with this year's annual report from the Federal Reserve Bank of Dallas, whose pages are graced by the smiling, stolid portraits of board members who run local companies like Whataburger Restaurants. But the text is something else entirely. It's a radical indictment of the nation's financial system. The lead essay, which is endorsed by the president of the Dallas Fed, contends that despite the great crisis of 2008, a cartel of megabanks is still hindering the economic recovery and the institutions remain too big to fail. The country's biggest banks look much as they did before the 2008 financial crisis -- only bigger. They have "increased oligopoly power" and "remain difficult to control because they have the lawyers and the money to resist the pressures of federal regulation," Harvey Rosenblum, the head of the Dallas Fed's research department, wrote in the essay. – ProPublica

Dominant Social Theme: We, the Fed, the most powerful monopoly on the planet, are concerned about the "increased oligopoly power" of our distribution system.

Free-Market Analysis: The excerpt above is taken from a column that "monitors" financial markets in order to hold "companies, executives and government officials accountable for their actions."

OK. It's a well-written column, but it misses a main point, in our humble view. The Federal Reserve is a mercantilist (quasi public) facility apparently controlled by dynastic families out of the City of London and elsewhere. For an entity within this larger monstrosity to call parts of the US banking system "too big to fail," is rich, to put it mildly.

This is actually part of a larger elite dominant social theme, that central banks are a public good and that the quasi-private banking system beneath them is where the problems reside.

This simply isn't true, in our humble opinion. As we've often pointed out, the current Western banking system is nothing but a distribution channel for the elite's monopoly fiat money. That's why the world is so overbanked.

If the Dallas Fed honchos had written the following, it would be closer to the truth: "Go to any large city on the planet and observe that the largest skyscrapers are filled with headquarters of obscure banks you've never heard of. Travel to any country and observe that banking is a primary occupation ...

"Banking is the world's biggest bubble. We distribute our printed and digital money-from-nothing through large commercial banks and thus they are never allowed to go out of business. They are part of us and we would no more remove them from the body politic than we would cease to purvey our endless tidal wave of currency."

In other words, it's kind of hypocritical for the Dallas Fed to complain about the size of American central banks. To use another metaphor, it's kind of like an obese person pointing to his stomach and claiming that it ought to shrink. Sure, a big stomach is a problem, but it's not the WHOLE problem by any means. Here's some more from the article:

Having seen the biggest banks make risky bets, crush the economy and get rewarded leaves "a residue of distrust for the government, the banking system, the Fed and capitalism itself," Mr. Rosenblum wrote. It's one thing for the Occupy movement to point out how bailing out the biggest banks -- with little cost to their executives or shareholders and creditors -- has demolished credibility. It's quite another for top officials in the Federal Reserve system to put it in an annual report.

"We know under the current structure that the government would be called on once again," the president of the Dallas Fed, Richard W. Fisher, told me. He has been giving a series of speeches about the continuing problem of "too big to fail." ...

Unfortunately for our banking regulation system, critics in the regional Federal Reserve banks haven't had much influence on regulatory policy ... Mr. Fisher, the Dallas Fed president, has been one of the fiercest inflation hawks. He has dissented against the Fed's efforts to buy longer-term assets, known as quantitative easing, which was an effort to stimulate the economy. (He has been less worried about inflation more recently, arguing that unemployment is the top problem for the economy.)

"Sound money and sound structure go hand in glove," Mr. Fisher said ... The top bank regulators at the Fed, meanwhile, have embraced unorthodox monetary policies, but have also had scant courage and originality in challenging the current structure of the country's financial system. Not so with the Dallas Fed. Its report champions "the ultimate solution for TBTF -- breaking up the nation's biggest banks into smaller units."

The elite's central banking promotion is an endless one. We are constantly transported to the Church of Paper Money where a group of good, gray men administer the creation of trillions of dollars at the push of a button.

After creating a random trillion here and there, these same individuals saunter out to the platform (or stage) and address the waiting "financial reporters." They explain they are very worried about "inflation," never hinting that they'd just primed their digital printing presses with another trillion that very morning.

In truth, central banks are inflation factories. The inflation is aimed at the money supply and price inflation is the inevitable result when the money finally begins to circulate. The confusion between inflation and price inflation is purposeful as well. It is another sub dominant social theme: "inflation" has to do with prices. It does not, of course. It has to do with the amount of money in circulation.

There were very few central banks 100 years ago. Today there are 150, and most of them are quasi-public entities, controlled behind the scenes by the top dynastic families, it seems, that want to create world government and use the proceeds of monopoly money to do so.

The trouble with the elite's control of central banking in the modern era is that what we call the Internet Reformation has thoroughly exposed it. As we have pointed out in many articles, the Internet is like the Gutenberg Press before it. It is a magnifying glass, exposing questionable realities that went unnoticed in the 20th century when the elites controlled virtually all forms of formal communication.

Today, the average man – struggling to keep his home, family and job – is well aware that there are a few people who regularly distribute trillions to their cronies while his region withers from the ruin that results from an overabundance of ever-more debased money.

It is this MORAL revelation – a revelation of immorality actually – that is likely going to do in the central banking system. The top central bankers like Fisher are deliberately trying to take a moral position about the modern money system but it may already be too late.

The idea is to whip up resentment against the putatively private sector – to pretend that central banking itself is above the fray and that the problems of the financial world have to do with the structure and immorality of Wall Street and "too-big-to-fail" banks.

For this reason, we have predicted that eventually there will be neo-Pecora hearings in Washington, DC that will then set the tone for the rest of the Western world as well. The previous Pecora hearings back in the 1930s blamed the Depression on Wall Street greed and corruption and set up the SEC, NASD etc.

The new Pecora hearings, which are even now being planned, will deal a full death blow to what is left of the private capital-raising mechanism of the US. There is no question that Wall Street is thoroughly contemptible and corrupted, but after these new hearings take place, there will be nothing left of market capitalism in the US.

The country will have fulfilled the mandate of possible Rothschild agent Alexander Hamilton who wanted to ensure that the US system mimicked the dirigiste European system where people born into one class could never migrate to another.

But there is the Internet ... Finally, there is the Internet. These neo-Pecora hearings – if and when they come – will not take place in a vacuum. The powers that be can do all they want to pretend that the problems of Western society come from "big banks" but the evident and obvious truth is that the problems faced by the Western world come from the money system itself.

The world is drowning in money and banks. This plethora of monetary agents has been propounded by the elites themselves to create recessions, depressions and eventually wars – the building blocks of the coming world government. Out of chaos ... order.

It will not do anymore for the elites to pretend that central banks are the disinterested solution to the "larger" problems of private-sector cronyism and corruption. In fact, fiat-money monopoly printing IS the problem. The biggest of the too-big-to-fail banks are the central banks themselves.

Conclusion: If the honchos of the Dallas Fed want to break up banks, they should start with their own.

DAILY BUSINESS REPORT - Financial Updates, International Markets and Business News

March 30, 2012

Peter Schiff: Market-Crushing Treasury Collapse To Hit Around 2013

Peter Schiff, the divisive investor and commentator that predicted the subprime/real-estate bubble, is forecasting a U.S. dollar and bond crisis over the next couple of years. Schiff blames intervened bond markets, where rates are artificially and excessively low, and expects the coming crisis to blow the 2008-9 financial crisis out of the water.

There is little doubt that the Federal Reserve, with Chairman Ben Bernanke at the helm, is holding markets by the hand. Bernanke, himself a divisive figure, has done all he can to push interest rates lower, using quantitative easing and Operation Twist once nominal rates had hit the zero-range. While many believe ultra-loose monetary policy is dangerous, Schiff thinks it will lead to a catastrophic correction.

“The more you delay it, the bigger it will be,” Schiff tells Forbes in a phone interview Tuesday, “so we need to raise interest rates during the recession to confront the inefficiencies.” Schiff, who runs Euro Pacific Capital and is seen by many as permanently bearish, argues that government-intervened bond markets are leading to massive distortions in capital allocation that have only been exacerbated as the Fed reacted to the last couple of recessions.

Recent market behavior supports his thesis that massive dislocations in bond yields distort reality. Ten-year Treasury yields had traded in a narrow-range for about four months, on the presumption that a weak economy would continue to count on Bernanke’s monetary support (particularly of the bond market). On March 13, the policy-setting Federal Open Market Committee (FOMC) acknowledged an improved recovery, but did not mention more quantitative easing, or bond purchases, were on the way, sparking a violent sell-off in Treasuries (exacerbated by JPMorgan’s dividend announcement the same day, which triggered a rally in financial stocks) as market players fled a bond rally they considered fixed by the Fed.

While Bernanke delivered calm to bond markets on Monday in a speech that promised “continued accommodative policies,” the violence of the sell-off speaks to Schiff’s argument. “We consume more than we produce and we borrow abroad, but we are never going to be able to pay them back,” says Schiff.

The controversial investor and commentator expects a massive crash over the next two to three years as a bond market bubble, coupled with the U.S. dollar, collapses under the weight of excessive debt. Schiff, like PIMCO’s Bill Gross, doesn’t believe in the current deleveraging cycle. While households have reduced their leverage, government debt has ballooned on the back of stimulus programs, but, argued Schiff, the government’s debt is the people’s debt, thus overall leverage has actually increased.

In CNBC interview Wednesday, Schiff called Bernanke “public enemy number one” and warned that banks would crash if the bond market collapses. While most major banks, including the likes of JPMorgan, Wells Fargo, and even Bank of America, passed the Fed’s strenuous stress tests, which stipulated a massive decline in equity and real estate prices, Schiff still believes they’re in trouble. “The Fed didn’t ask the banks to stress test a big drop in the bond market because that’s what coming, and the banks would fail that,” he said.

Schiff cites the rising price of gold as evidence that U.S. dollar debasement, and inflation, are higher than the Fed, and consumer price data, suggest. Following the Austrian economic tradition, Schiff believes that only a massive correction, via a deflationary recession, can set the system straight. “In a deflation, real wages will rise because the cost of goods will fall faster,” he says, adding that the government should accompany the correction by lowering taxes and cutting back on regulation.

While Schiff does suggest saving in gold, he understands the limitations of the investment. “If you invest in gold, then the economy doesn’t benefit from savings, I want investment to go to plants and equipment.”

The system, he argues, is as broken as it was before the financial crisis. Schiff, who was very prescient in his forecast and prediction of how the subprime debacle would filter through to the broader real estate market and thus bring down the economy, believes complacency is widespread. “All of the people who were 100% wrong [back in ‘08] are saying that everything’s OK [now]. I am telling them they didn’t solve the problem and are making it so much worse.”

Schiff, who knows how to build his case, concludes it thusly: “I didn’t get lucky, I just understood the problem, and we are going to get another big one coming soon.”

There is little doubt that the Federal Reserve, with Chairman Ben Bernanke at the helm, is holding markets by the hand. Bernanke, himself a divisive figure, has done all he can to push interest rates lower, using quantitative easing and Operation Twist once nominal rates had hit the zero-range. While many believe ultra-loose monetary policy is dangerous, Schiff thinks it will lead to a catastrophic correction.

“The more you delay it, the bigger it will be,” Schiff tells Forbes in a phone interview Tuesday, “so we need to raise interest rates during the recession to confront the inefficiencies.” Schiff, who runs Euro Pacific Capital and is seen by many as permanently bearish, argues that government-intervened bond markets are leading to massive distortions in capital allocation that have only been exacerbated as the Fed reacted to the last couple of recessions.

Recent market behavior supports his thesis that massive dislocations in bond yields distort reality. Ten-year Treasury yields had traded in a narrow-range for about four months, on the presumption that a weak economy would continue to count on Bernanke’s monetary support (particularly of the bond market). On March 13, the policy-setting Federal Open Market Committee (FOMC) acknowledged an improved recovery, but did not mention more quantitative easing, or bond purchases, were on the way, sparking a violent sell-off in Treasuries (exacerbated by JPMorgan’s dividend announcement the same day, which triggered a rally in financial stocks) as market players fled a bond rally they considered fixed by the Fed.

While Bernanke delivered calm to bond markets on Monday in a speech that promised “continued accommodative policies,” the violence of the sell-off speaks to Schiff’s argument. “We consume more than we produce and we borrow abroad, but we are never going to be able to pay them back,” says Schiff.

The controversial investor and commentator expects a massive crash over the next two to three years as a bond market bubble, coupled with the U.S. dollar, collapses under the weight of excessive debt. Schiff, like PIMCO’s Bill Gross, doesn’t believe in the current deleveraging cycle. While households have reduced their leverage, government debt has ballooned on the back of stimulus programs, but, argued Schiff, the government’s debt is the people’s debt, thus overall leverage has actually increased.

In CNBC interview Wednesday, Schiff called Bernanke “public enemy number one” and warned that banks would crash if the bond market collapses. While most major banks, including the likes of JPMorgan, Wells Fargo, and even Bank of America, passed the Fed’s strenuous stress tests, which stipulated a massive decline in equity and real estate prices, Schiff still believes they’re in trouble. “The Fed didn’t ask the banks to stress test a big drop in the bond market because that’s what coming, and the banks would fail that,” he said.

Schiff cites the rising price of gold as evidence that U.S. dollar debasement, and inflation, are higher than the Fed, and consumer price data, suggest. Following the Austrian economic tradition, Schiff believes that only a massive correction, via a deflationary recession, can set the system straight. “In a deflation, real wages will rise because the cost of goods will fall faster,” he says, adding that the government should accompany the correction by lowering taxes and cutting back on regulation.

While Schiff does suggest saving in gold, he understands the limitations of the investment. “If you invest in gold, then the economy doesn’t benefit from savings, I want investment to go to plants and equipment.”

The system, he argues, is as broken as it was before the financial crisis. Schiff, who was very prescient in his forecast and prediction of how the subprime debacle would filter through to the broader real estate market and thus bring down the economy, believes complacency is widespread. “All of the people who were 100% wrong [back in ‘08] are saying that everything’s OK [now]. I am telling them they didn’t solve the problem and are making it so much worse.”

Schiff, who knows how to build his case, concludes it thusly: “I didn’t get lucky, I just understood the problem, and we are going to get another big one coming soon.”

March 29, 2012

Goldman Ex-Prop Traders Flopping on Their Own

John Whitehead is being proven right.

The former Goldman co-chairman took the unheard of step of excoriating Lloyd Blankfein for Goldman’s “shocking” pay levels of 2006. As anyone who has been following Wall Street knows, compensation levels were even higher in 2007, 2009, 2010 and last year. Per an interview with Bloomberg:

“I’m appalled at the salaries,” the retired co-chairman of the securities industry’s most profitable firm said in an interview this week. At Goldman, which paid Chairman and Chief Executive Officer Lloyd Blankfein $54 million last year, compensation levels are “shocking,” Whitehead said. “They’re the leaders in this outrageous increase.”

Whitehead went even further, recommending the unthinkable, that Goldman cut pay:

Whitehead, who left the firm in 1984 and now chairs its charitable foundation, said Goldman should be courageous enough to curb bonuses, even if the effort to return a sense of restraint to Wall Street costs it some valued employees. No securities firm can match the pay available in a good year at the top hedge funds.

“I would take the chance of losing a lot of them and let them see what happens when the hedge fund bubble, as I see it, ends,” Whitehead, 85, said….

The Galtian traders who carry on as if they are solely responsible for their profits are being shown to be more dependent on the franchise, in particular, the concentrated information flows from dealing with lots of customers and counterparties, than they had persuaded themselves and management. Bloomberg today tells us that the prop traders who have decamped from Goldman, convinced that they’d be able to rack up stellar returns, are floundering. It isn’t just that they aren’t racking up huge wins; they are losing money and falling short of hitting the average for their trading strategy. As the report notes:

Ex-Goldman Sachs (GS) Group Inc. traders led by Pierre-Henri Flamand and Morgan Sze raised more than $4.5 billion for their own hedge funds..

So far, none of them has made money for clients.

The two are among at least six traders who have left Goldman Sachs’s biggest proprietary-trading group in the past two years, which the New York-based bank shuttered in response to new U.S. regulations. All, including Daniele Benatoff and Ariel Roskis, trailed this year’s stock market rally after losing money in 2011, investors said…

Flamand, 41, who was the global chief of Goldman Sachs’s principal strategies group before he quit two years ago to start Edoma Capital Partners LLP in London, has lost about 2.4 percent through February since his $1.8 billion hedge fund started in November 2010, according to investors.

Edoma is an event-driven fund, which invests in companies undergoing events such as mergers, spinoffs and bankruptcies. Such funds returned an average 3.9 percent in the same 16-month period…

Sze, 46, who ran Goldman Sachs’s principal strategies team in Asia before briefly replacing Flamand as global head, left the bank in 2010 to start Azentus Capital Management Ltd. in Hong Kong, hiring 13 former Goldman Sachs traders. His event- driven fund lost about 4.8 percent through February since its April 2011 inception, said a person with knowledge of its returns.

Event-driven funds declined 2.4 percent in the same period…

We’ve long been skeptical of the idea that big firm traders are worth their outsized pay packages. Of course, it nevertheless make sense for management to play along, since higher pay levels for traders justify robust pay for everyone senior to them in the hierarchy (yes, a top trader will often be paid more than the top brass, but it’s an anchoring issue. And pay in banks at the senior levels has become more hierarchical than it was in the 1980s and 1990s).

Long standing readers may recall the 2009 row over the pay level of Andrew Hall, the head of a Citigroup oil trading unit. He had made $100 million in 2008 on a long-standing pay arrangement that gave him a pay deal for his team that was just below 30% of profits, a level unheard of since Mike Milken at Drexel (and we all know how well that turned out). Kenneth Feinberg, Obama’s pay czar, refused to back down, leading to the predictable hue and cry as to how terrible it would be to break Hall’s contract (we pointed out that there were likely ways to do just that, that big producers like Hall were often guilty of expense abuses that would allow for termination for cause).

Consistent with the notion that Hall needed Citi more than he’d pretended earlier, he started negotiating with the bank (if he really was such a hot item, one would think he’d be able to decamp and raise money). As we pointed out at the time:

A LOT of Hall’s performance was due to cheap funding from Citi, and probably massive leverage too, conditions he could not replicate anywhere else. A risky, highly geared operation should pay an interest rate appropriate to the hazards it is taking, not the borrowing costs of its parent (this basic premise is widespread in financial firms, embodied in approaches like RAROC (Risk Adjusted Return on Capital), the Basel I and II rules, and Economic Value Added models.

And the denouement, from ECONNED:

Phibro, along with its richly paid chief, Andrew Hall, is leaving Citigroup for Occidental Petroleum. The price Oxy paid for Phibro was only the current value of its trading positions–liquidation value and not a brass razoo more. There was NO premium for the earning potential of Hall and his supposed money machine. It’s not hard to see why. Hall’s returns were heavily dependent on high leverage, cheap funding, and market intelligence from other trading desks, all huge subsidies from Citigroup. In turn, these concentrated capital and information flows do not come about naturally, but are the product of industry-favoring policies.

His example illustrates that the widely proclaimed view that highly profitable traders are worth their exorbitant pay is often a fiction. The fact that no other buyers, not a financial firm, commodities trader, or consortium, stepped forward when Citi was looking for a graceful exit shows that the business was worth very little on a stand-alone basis.

Instead of seeing the Hall episode as further evidence that industry pay practices are extractive, the media focused instead on “government interference” or how Citi would be harmed by losing the revenues from taxpayer-supported commodities speculation.

The problem, of course is that given how much traders and investors who appear to generate outsized returns (query at what risk and with what information advantages) are celebrated in their circles almost as much as sports stars. Their allure is fading bit by bit, but it will be quite a while before the ascendancy of traders is reversed.

The former Goldman co-chairman took the unheard of step of excoriating Lloyd Blankfein for Goldman’s “shocking” pay levels of 2006. As anyone who has been following Wall Street knows, compensation levels were even higher in 2007, 2009, 2010 and last year. Per an interview with Bloomberg:

“I’m appalled at the salaries,” the retired co-chairman of the securities industry’s most profitable firm said in an interview this week. At Goldman, which paid Chairman and Chief Executive Officer Lloyd Blankfein $54 million last year, compensation levels are “shocking,” Whitehead said. “They’re the leaders in this outrageous increase.”

Whitehead went even further, recommending the unthinkable, that Goldman cut pay:

Whitehead, who left the firm in 1984 and now chairs its charitable foundation, said Goldman should be courageous enough to curb bonuses, even if the effort to return a sense of restraint to Wall Street costs it some valued employees. No securities firm can match the pay available in a good year at the top hedge funds.

“I would take the chance of losing a lot of them and let them see what happens when the hedge fund bubble, as I see it, ends,” Whitehead, 85, said….

The Galtian traders who carry on as if they are solely responsible for their profits are being shown to be more dependent on the franchise, in particular, the concentrated information flows from dealing with lots of customers and counterparties, than they had persuaded themselves and management. Bloomberg today tells us that the prop traders who have decamped from Goldman, convinced that they’d be able to rack up stellar returns, are floundering. It isn’t just that they aren’t racking up huge wins; they are losing money and falling short of hitting the average for their trading strategy. As the report notes:

Ex-Goldman Sachs (GS) Group Inc. traders led by Pierre-Henri Flamand and Morgan Sze raised more than $4.5 billion for their own hedge funds..

So far, none of them has made money for clients.

The two are among at least six traders who have left Goldman Sachs’s biggest proprietary-trading group in the past two years, which the New York-based bank shuttered in response to new U.S. regulations. All, including Daniele Benatoff and Ariel Roskis, trailed this year’s stock market rally after losing money in 2011, investors said…

Flamand, 41, who was the global chief of Goldman Sachs’s principal strategies group before he quit two years ago to start Edoma Capital Partners LLP in London, has lost about 2.4 percent through February since his $1.8 billion hedge fund started in November 2010, according to investors.

Edoma is an event-driven fund, which invests in companies undergoing events such as mergers, spinoffs and bankruptcies. Such funds returned an average 3.9 percent in the same 16-month period…

Sze, 46, who ran Goldman Sachs’s principal strategies team in Asia before briefly replacing Flamand as global head, left the bank in 2010 to start Azentus Capital Management Ltd. in Hong Kong, hiring 13 former Goldman Sachs traders. His event- driven fund lost about 4.8 percent through February since its April 2011 inception, said a person with knowledge of its returns.

Event-driven funds declined 2.4 percent in the same period…

We’ve long been skeptical of the idea that big firm traders are worth their outsized pay packages. Of course, it nevertheless make sense for management to play along, since higher pay levels for traders justify robust pay for everyone senior to them in the hierarchy (yes, a top trader will often be paid more than the top brass, but it’s an anchoring issue. And pay in banks at the senior levels has become more hierarchical than it was in the 1980s and 1990s).

Long standing readers may recall the 2009 row over the pay level of Andrew Hall, the head of a Citigroup oil trading unit. He had made $100 million in 2008 on a long-standing pay arrangement that gave him a pay deal for his team that was just below 30% of profits, a level unheard of since Mike Milken at Drexel (and we all know how well that turned out). Kenneth Feinberg, Obama’s pay czar, refused to back down, leading to the predictable hue and cry as to how terrible it would be to break Hall’s contract (we pointed out that there were likely ways to do just that, that big producers like Hall were often guilty of expense abuses that would allow for termination for cause).

Consistent with the notion that Hall needed Citi more than he’d pretended earlier, he started negotiating with the bank (if he really was such a hot item, one would think he’d be able to decamp and raise money). As we pointed out at the time:

A LOT of Hall’s performance was due to cheap funding from Citi, and probably massive leverage too, conditions he could not replicate anywhere else. A risky, highly geared operation should pay an interest rate appropriate to the hazards it is taking, not the borrowing costs of its parent (this basic premise is widespread in financial firms, embodied in approaches like RAROC (Risk Adjusted Return on Capital), the Basel I and II rules, and Economic Value Added models.

And the denouement, from ECONNED:

Phibro, along with its richly paid chief, Andrew Hall, is leaving Citigroup for Occidental Petroleum. The price Oxy paid for Phibro was only the current value of its trading positions–liquidation value and not a brass razoo more. There was NO premium for the earning potential of Hall and his supposed money machine. It’s not hard to see why. Hall’s returns were heavily dependent on high leverage, cheap funding, and market intelligence from other trading desks, all huge subsidies from Citigroup. In turn, these concentrated capital and information flows do not come about naturally, but are the product of industry-favoring policies.

His example illustrates that the widely proclaimed view that highly profitable traders are worth their exorbitant pay is often a fiction. The fact that no other buyers, not a financial firm, commodities trader, or consortium, stepped forward when Citi was looking for a graceful exit shows that the business was worth very little on a stand-alone basis.

Instead of seeing the Hall episode as further evidence that industry pay practices are extractive, the media focused instead on “government interference” or how Citi would be harmed by losing the revenues from taxpayer-supported commodities speculation.

The problem, of course is that given how much traders and investors who appear to generate outsized returns (query at what risk and with what information advantages) are celebrated in their circles almost as much as sports stars. Their allure is fading bit by bit, but it will be quite a while before the ascendancy of traders is reversed.

March 28, 2012

Bernanke Claims That The Fed Has Averted A Second Great Depression By Bailing Out The Too Big To Fail Banks

Federal Reserve Chairman Ben Bernanke claims that the Federal Reserve averted a second Great Depression by bailing out the big Wall Street banks during the last financial crisis, and he says that if a similar financial crisis comes along that the correct "policy response" will be to do the exact same thing again. This was the theme of the lecture that Bernanke delivered to students at George Washington University on Tuesday. In previous lectures Bernanke has defended the existence of the Fed and detailed the history of Fed activities, but on Tuesday he addressed things that have happened since he has been at the helm of the Fed. And according to Bernanke, he has been doing a great job. Bernanke told the students that the "threat of a second Great Depression was very real" and that the Federal Reserve did exactly what needed to be done to fix the financial system. Unfortunately, the truth is that all Bernanke did was kick the can a bit farther down the road. You can't fix a debt problem with more debt, and the debt bubble we are living in today is far larger than it was in 2008. Will Bernanke still be trying to portray himself as a hero when this house of cards finally falls apart?

During his lecture to the students on Tuesday, Bernanke stated the following....

"I think the view is increasingly gaining acceptance that without the forceful policy response that stabilized the financial system in 2008 and early 2009, we could have had a much worse outcome in the economy."

So what did that "forceful policy response" entail?

Well, on slide 24 of his presentation to the students Bernanke tells us....

• On October 10, 2008, G‐7 countries agreed to

work together to stabilize the global financial

system. They agreed to

– prevent the failure of systemically important

financial institutions

– ensure financial institutions’ access to funding and

capital

– restore depositor confidence

– work to normalize credit markets

Please note that not all financial institutions got bailed out.

In fact, hundreds of small and mid-size U.S. banks failed during the financial crisis.

It was only the "systemically important financial institutions" that got bailed out.

So who decided which financial institutions were important enough to be bailed out?

The Federal Reserve made those decisions. There were no Congressional votes and no input from the public. The Federal Reserve determined who the winners and the losers would be in secret and without any public debate.

Sure sounds "democratic", eh?

But we are told to trust them because they are supposedly the experts.

So once the Federal Reserve bailed out the "too big to fail" banks, what was the outcome?

On page 25 of his presentation to the students Bernanke claimed that the bailouts successfully prevented the global financial system from collapsing....

• The international policy response averted the collapse of the global financial system.

But it wasn't just big Wall Street banks that got bailed out. Bernanke says that AIG was also bailed out because the insurance company was deemed to be too "interconnected with many other parts of the global financial system" to be allowed to fail....

Because AIG was interconnected with many other parts of the global financial system, its failure would have had a massive effect on other financial firms and markets.

Once again, we see that it is the Federal Reserve who picks the winners and the losers.

AIG got bailed out and was then able to pay 100 cents on the dollar of what it owed to Goldman Sachs.

That sure worked out well for Goldman Sachs.

In all, the Federal Reserve issued a grand total of more than 16 trillion dollars in secret loans during the financial crisis.

The big Wall Street banks got showered with cash while hundreds of smaller banks were allowed to die like dogs.

The fact that the Fed greatly favors the big Wall Street banks has allowed them to grow massively in size and in power.

Back in 1970, the 5 biggest U.S. banks held 17 percent of all U.S. banking industry assets.

Today, the 5 biggest U.S. banks hold 52 percent of all U.S. banking industry assets.

The "too big to fail" banks just keep getting bigger and bigger and bigger.

Yet during his presentation to the students, Bernanke tried to talk out of both sides of his mouth by claiming that it is not a good thing for some banks to be "too big to fail"....

"But clearly, it is something fundamentally wrong with a system in which some companies are 'too big to fail.'"

So who is to blame for them being so big?

Well, the Federal Reserve is probably the biggest culprit.

Thanks Bernanke.

The big Wall Street banks are bigger than ever and they are also more unstable than ever.

According to the Comptroller of the Currency, the biggest U.S. banks have exposure to derivatives that is absolutely mind blowing. Just check out these numbers which have just been released....

JPMorgan Chase - $70.1 Trillion

Citibank - $52.1 Trillion

Bank of America - $50.1 Trillion

Goldman Sachs - $44.2 Trillion

So what is going to happen when that bubble pops?

Is Bernanke going to zap tens of trillions of dollars into existence to bail out that gigantic mess?

Meanwhile, the debt bubble that we are all living in just keeps exploding in size.

Total student loan debt in the United States is over 1 trillion dollars at this point. Consumer debt is rising. Millions of mortgages are past due.

The American people are not in better financial condition than they were during the last financial crisis. In fact, they are significantly worse off.

All over America, state and local governments are also drowning in debt. In fact, there have been several very notable municipal bankruptcies lately.

And the U.S. government is racking up debt at a pace that is almost unimaginable.

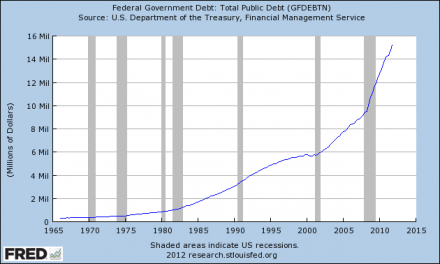

When the last financial crisis began, the U.S. national debt was about 10 trillion dollars.

Today, it has risen to 15.5 trillion dollars.

So Bernanke did not fix anything.

The best that can be said is that he kicked the can down the road a little bit and made our long-term financial problems a lot worse at the same time.

Bernanke can create money out of thin air and loan it to his friends all he wants, but he is not going to be able to prevent this house of cards from crashing down indefinitely.

So grab a bucket of popcorn and get ready. The next few years are going to be fascinating to watch.

During his lecture to the students on Tuesday, Bernanke stated the following....

"I think the view is increasingly gaining acceptance that without the forceful policy response that stabilized the financial system in 2008 and early 2009, we could have had a much worse outcome in the economy."

So what did that "forceful policy response" entail?

Well, on slide 24 of his presentation to the students Bernanke tells us....

• On October 10, 2008, G‐7 countries agreed to

work together to stabilize the global financial

system. They agreed to

– prevent the failure of systemically important

financial institutions

– ensure financial institutions’ access to funding and

capital

– restore depositor confidence

– work to normalize credit markets

Please note that not all financial institutions got bailed out.

In fact, hundreds of small and mid-size U.S. banks failed during the financial crisis.

It was only the "systemically important financial institutions" that got bailed out.

So who decided which financial institutions were important enough to be bailed out?

The Federal Reserve made those decisions. There were no Congressional votes and no input from the public. The Federal Reserve determined who the winners and the losers would be in secret and without any public debate.

Sure sounds "democratic", eh?

But we are told to trust them because they are supposedly the experts.

So once the Federal Reserve bailed out the "too big to fail" banks, what was the outcome?

On page 25 of his presentation to the students Bernanke claimed that the bailouts successfully prevented the global financial system from collapsing....

• The international policy response averted the collapse of the global financial system.

But it wasn't just big Wall Street banks that got bailed out. Bernanke says that AIG was also bailed out because the insurance company was deemed to be too "interconnected with many other parts of the global financial system" to be allowed to fail....

Because AIG was interconnected with many other parts of the global financial system, its failure would have had a massive effect on other financial firms and markets.

Once again, we see that it is the Federal Reserve who picks the winners and the losers.

AIG got bailed out and was then able to pay 100 cents on the dollar of what it owed to Goldman Sachs.

That sure worked out well for Goldman Sachs.

In all, the Federal Reserve issued a grand total of more than 16 trillion dollars in secret loans during the financial crisis.

The big Wall Street banks got showered with cash while hundreds of smaller banks were allowed to die like dogs.

The fact that the Fed greatly favors the big Wall Street banks has allowed them to grow massively in size and in power.

Back in 1970, the 5 biggest U.S. banks held 17 percent of all U.S. banking industry assets.

Today, the 5 biggest U.S. banks hold 52 percent of all U.S. banking industry assets.

The "too big to fail" banks just keep getting bigger and bigger and bigger.

Yet during his presentation to the students, Bernanke tried to talk out of both sides of his mouth by claiming that it is not a good thing for some banks to be "too big to fail"....

"But clearly, it is something fundamentally wrong with a system in which some companies are 'too big to fail.'"

So who is to blame for them being so big?

Well, the Federal Reserve is probably the biggest culprit.

Thanks Bernanke.

The big Wall Street banks are bigger than ever and they are also more unstable than ever.

According to the Comptroller of the Currency, the biggest U.S. banks have exposure to derivatives that is absolutely mind blowing. Just check out these numbers which have just been released....

JPMorgan Chase - $70.1 Trillion

Citibank - $52.1 Trillion

Bank of America - $50.1 Trillion

Goldman Sachs - $44.2 Trillion

So what is going to happen when that bubble pops?

Is Bernanke going to zap tens of trillions of dollars into existence to bail out that gigantic mess?

Meanwhile, the debt bubble that we are all living in just keeps exploding in size.

Total student loan debt in the United States is over 1 trillion dollars at this point. Consumer debt is rising. Millions of mortgages are past due.

The American people are not in better financial condition than they were during the last financial crisis. In fact, they are significantly worse off.

All over America, state and local governments are also drowning in debt. In fact, there have been several very notable municipal bankruptcies lately.

And the U.S. government is racking up debt at a pace that is almost unimaginable.

When the last financial crisis began, the U.S. national debt was about 10 trillion dollars.

Today, it has risen to 15.5 trillion dollars.

So Bernanke did not fix anything.

The best that can be said is that he kicked the can down the road a little bit and made our long-term financial problems a lot worse at the same time.

Bernanke can create money out of thin air and loan it to his friends all he wants, but he is not going to be able to prevent this house of cards from crashing down indefinitely.

So grab a bucket of popcorn and get ready. The next few years are going to be fascinating to watch.

March 27, 2012

John Corzine- An Insider Helping Out Fellow Insiders

Few men have a resume quite like Jon Corzine. Not only has Corzine served in the U.S. Senate and been governor of New Jersey, he has also been the CEO of Goldman Sachs and the recently imploded brokerage firm MF Global. The insider blood filtrated through cronyism and the endless squandering of the public dime flows heavily through his veins.

When MF Global went belly up back in the fall, Corzine was finally revealed for the inept, overly connected bureaucrat he really is. Corruption seemingly follows the former Senator, Governor, and banker like shadows on a sunny day. Earlier this week, New Jersey was declared the least corruptible state in the union much to the surprise of, well, everyone. But as the great Jonathan Weil pointed out, the methodology in the study conducted by the Center for Public Integrity was horribly flawed. New Jersey has historically been defined with corruption:

…this is a state where in 2009 three mayors, two assemblymen and five rabbis were among 44 charged in a single money-laundering and bribery sting by the Federal Bureau of Investigation. One of those mayors, Peter Cammarano, was from Hoboken, where I live. He was sentenced to 24 months in prison. Five years before his arrest, another former Hoboken mayor, Anthony Russo, pleaded guilty to corruption charges. His son now sits on the city council.

Corzine was of course acquainted with one of the mayors listed and a member of his own cabinet faced investigation by the FBI during the same time period. And that was only the man’s tenure as Governor. Anyone who spends their time horse-trading in Congress is instantly guilty of corruption by definition. Corzine was especially so as he coauthored the Sarbanes-Oxley financial regulatory bill which heaped another expense on start up businesses to the benefit of already established and politically favored firms.

Corzine’s political career was launched after his term heading the financial vampire squid known as Goldman Sachs which has its tentacles within practically every important or relevant governing authority around the globe. During his time at GS, he served on a presidential commission for Bill Clinton and a committee in the U.S. Treasury. In short, before his time heading MF Global, Corzine was an expert paper pusher whose connections in the political establishment were deeply rooted. That’s why he made the perfect candidate for a multinational investment firm on the up and up.

Not too long after Corzine went to MF Global, he visited the New York branch of the Federal Reserve in an attempt to expedite the process by which MF could received the coveted “primary dealer” privilege. This primary dealer position gave MF the ability to be one of the first financial institutions the NY Fed would purchase government securities and bonds from when the central bank wished to expand the monetary base. It is the ultimate position any banking insider looking to game the system seeks. Though an official from the NY Fed denies any special treatment was given to Corzine (as if they would own up to it in public anyway), as the Wall Street Journal explains, “the New York Fed doesn’t publicly discuss” decisions of granting primary dealership status, “but a source with knowledge of the process says that it sometimes takes several years for a firm to gain acceptance.”

And yet we are to believe that Corzine’s numerous connections didn’t help fast track this process?

It should be obvious by now how heavy a user Mr. Corzine is of the revolving door between Wall Street and Washington. Insiders are able to make a fortune by occupying public office and subsequently being offered a prominent position in an industry seeking to exploit regulation by hiring those who know it best. This often includes the authors of the regulations themselves. Corzine is not only an experienced alumni of this group but a practical valedictorian.

For someone so experienced in this utterly corrupt dynamic, it came as a surprise to see MF Global crash and burn as the European debt crisis escalated. Perhaps Corzine was betting on a more monetarily aggressive European Central Bank to bailout the profligate governments of the periphery? Whatever the case, Corzine and co. were caught red handed as the firm declared bankruptcy and $1.2 billion of money supposed to be secured in customer accounts went missing. At the time, Corzine pathetically told the Agricultural Committee in the House of Representatives:

“I simply do not know where the money is, or why the accounts have not been reconciled to date,”

As it turns out, Corzine should have known where at least some of the funds went. From Bloomberg:

Jon S. Corzine, MF Global Holding Ltd. (MFGLQ)’s chief executive officer, gave “direct instructions” to transfer $200 million from a customer fund account to meet an overdraft in a brokerage account with JPMorgan Chase & Co. (JPM), according to a memo written by congressional investigators.

Edith O’Brien, a treasurer for the firm, said in an e-mail quoted in the memo that the transfer was “Per JC’s direct instructions,” according to a copy of the memo obtained by Bloomberg News yesterday. The e-mail, dated Oct. 28, was sent three days before the company collapsed, the memo says. The memo does not indicate whether that phrase was the full text of the e-mail or an excerpt.

In what will surely be labeled an unfortunate coincidence, a fellow NY Fed primary dealer was given a helping hand as the firm knowingly imploded.

Talk about friends with benefits.

Corzine may be subpoenaed by Congress and used as a punching bag by Republicans looking to score political points but the dominant culture of increasing centralization and cronyism which is an ever-present aspect of state will carry on unchallenged. Corzine will simply be the scapegoat of the political class looking to give off the mirage of integrity within government. God forbid politicians not “do something” in the wake of a controversy they themselves are responsible for.

As economist Freidrich Hayek taught, power centers attract and breed unscrupulous behavior. There is no institution more powerful than that of the state apparatus which feeds off the continual usurpation of authority and acts as the sole monopolizer of force over a given geographical area. Governments don’t minimize class divisions, they are the originator of stagnant social mobility. The Jon Corzines of the world feel entitled to their positions of prominence and will do anything to secure them as they blatantly skirt the law and protect their friends by any means necessary. The normal rules imposed on society don’t apply to them for they are the rule makers. The existence of central banks not bound by restraints on money creation and the backing of fractional reserve banking with taxpayer funds are simply extensions of the unceasing jackboot pressed down upon economic and social freedom. This is why Ben Bernanke’s Fed fought tooth and nail to not disclose the amount of money “lent” out to big banks during the financial crisis.

If there is one good thing to come about from the whole MF Global affair, besides putting a stake in the heart of Corzine’s reputation, it was the fact that the firm wasn’t bailed out by by the Treasury or Fed. The powers that be decided to let MF go as a possible sign that more of the public is becoming aware of the farce of a market the financial industry is which acts as a middleman between the government and the printing press. Market forces don’t decide winners and losers in today’s banking industry; the members of the elite class do.

When MF Global went belly up back in the fall, Corzine was finally revealed for the inept, overly connected bureaucrat he really is. Corruption seemingly follows the former Senator, Governor, and banker like shadows on a sunny day. Earlier this week, New Jersey was declared the least corruptible state in the union much to the surprise of, well, everyone. But as the great Jonathan Weil pointed out, the methodology in the study conducted by the Center for Public Integrity was horribly flawed. New Jersey has historically been defined with corruption:

…this is a state where in 2009 three mayors, two assemblymen and five rabbis were among 44 charged in a single money-laundering and bribery sting by the Federal Bureau of Investigation. One of those mayors, Peter Cammarano, was from Hoboken, where I live. He was sentenced to 24 months in prison. Five years before his arrest, another former Hoboken mayor, Anthony Russo, pleaded guilty to corruption charges. His son now sits on the city council.

Corzine was of course acquainted with one of the mayors listed and a member of his own cabinet faced investigation by the FBI during the same time period. And that was only the man’s tenure as Governor. Anyone who spends their time horse-trading in Congress is instantly guilty of corruption by definition. Corzine was especially so as he coauthored the Sarbanes-Oxley financial regulatory bill which heaped another expense on start up businesses to the benefit of already established and politically favored firms.

Corzine’s political career was launched after his term heading the financial vampire squid known as Goldman Sachs which has its tentacles within practically every important or relevant governing authority around the globe. During his time at GS, he served on a presidential commission for Bill Clinton and a committee in the U.S. Treasury. In short, before his time heading MF Global, Corzine was an expert paper pusher whose connections in the political establishment were deeply rooted. That’s why he made the perfect candidate for a multinational investment firm on the up and up.

Not too long after Corzine went to MF Global, he visited the New York branch of the Federal Reserve in an attempt to expedite the process by which MF could received the coveted “primary dealer” privilege. This primary dealer position gave MF the ability to be one of the first financial institutions the NY Fed would purchase government securities and bonds from when the central bank wished to expand the monetary base. It is the ultimate position any banking insider looking to game the system seeks. Though an official from the NY Fed denies any special treatment was given to Corzine (as if they would own up to it in public anyway), as the Wall Street Journal explains, “the New York Fed doesn’t publicly discuss” decisions of granting primary dealership status, “but a source with knowledge of the process says that it sometimes takes several years for a firm to gain acceptance.”

And yet we are to believe that Corzine’s numerous connections didn’t help fast track this process?

It should be obvious by now how heavy a user Mr. Corzine is of the revolving door between Wall Street and Washington. Insiders are able to make a fortune by occupying public office and subsequently being offered a prominent position in an industry seeking to exploit regulation by hiring those who know it best. This often includes the authors of the regulations themselves. Corzine is not only an experienced alumni of this group but a practical valedictorian.

For someone so experienced in this utterly corrupt dynamic, it came as a surprise to see MF Global crash and burn as the European debt crisis escalated. Perhaps Corzine was betting on a more monetarily aggressive European Central Bank to bailout the profligate governments of the periphery? Whatever the case, Corzine and co. were caught red handed as the firm declared bankruptcy and $1.2 billion of money supposed to be secured in customer accounts went missing. At the time, Corzine pathetically told the Agricultural Committee in the House of Representatives:

“I simply do not know where the money is, or why the accounts have not been reconciled to date,”

As it turns out, Corzine should have known where at least some of the funds went. From Bloomberg:

Jon S. Corzine, MF Global Holding Ltd. (MFGLQ)’s chief executive officer, gave “direct instructions” to transfer $200 million from a customer fund account to meet an overdraft in a brokerage account with JPMorgan Chase & Co. (JPM), according to a memo written by congressional investigators.

Edith O’Brien, a treasurer for the firm, said in an e-mail quoted in the memo that the transfer was “Per JC’s direct instructions,” according to a copy of the memo obtained by Bloomberg News yesterday. The e-mail, dated Oct. 28, was sent three days before the company collapsed, the memo says. The memo does not indicate whether that phrase was the full text of the e-mail or an excerpt.

In what will surely be labeled an unfortunate coincidence, a fellow NY Fed primary dealer was given a helping hand as the firm knowingly imploded.

Talk about friends with benefits.

Corzine may be subpoenaed by Congress and used as a punching bag by Republicans looking to score political points but the dominant culture of increasing centralization and cronyism which is an ever-present aspect of state will carry on unchallenged. Corzine will simply be the scapegoat of the political class looking to give off the mirage of integrity within government. God forbid politicians not “do something” in the wake of a controversy they themselves are responsible for.

As economist Freidrich Hayek taught, power centers attract and breed unscrupulous behavior. There is no institution more powerful than that of the state apparatus which feeds off the continual usurpation of authority and acts as the sole monopolizer of force over a given geographical area. Governments don’t minimize class divisions, they are the originator of stagnant social mobility. The Jon Corzines of the world feel entitled to their positions of prominence and will do anything to secure them as they blatantly skirt the law and protect their friends by any means necessary. The normal rules imposed on society don’t apply to them for they are the rule makers. The existence of central banks not bound by restraints on money creation and the backing of fractional reserve banking with taxpayer funds are simply extensions of the unceasing jackboot pressed down upon economic and social freedom. This is why Ben Bernanke’s Fed fought tooth and nail to not disclose the amount of money “lent” out to big banks during the financial crisis.

If there is one good thing to come about from the whole MF Global affair, besides putting a stake in the heart of Corzine’s reputation, it was the fact that the firm wasn’t bailed out by by the Treasury or Fed. The powers that be decided to let MF go as a possible sign that more of the public is becoming aware of the farce of a market the financial industry is which acts as a middleman between the government and the printing press. Market forces don’t decide winners and losers in today’s banking industry; the members of the elite class do.

March 26, 2012

On the Meaningless of Contracts and the New Optionality

An old saying is that contracts are only as good as the parties that enter into them. And the evidence is growing that when there is a meaningful power disparity between two parties to an agreement, the odds are high that the bigger player will elect to behave badly. This blog is rife with examples: pervasive contractual and regulatory violations in securitizations and foreclosures, banks exploiting not just ordinary consumers with “tricks and traps” but even billionaire clients; debt collection abuses; routine raiding of employee pensions while CEO pay and perquisites remain sacrosanct; and, of course, the pilfering of customer accounts at MF Global.

And conditions on the ground are even worse. Hoisted from comments:

LAS says:

March 23, 2012 at 10:41 am

I think you are on to something, Yves.

There’s no indication of improvement either.

For an example, our firm completed work for a major corporation last month (successfully) and they will not accept the invoice for our work. While we have had to lay out cash to perform the work, they have not. Although they came to us to do the work for them, they have shut down their procurement/accounts payable dept and they have kept it shut for about 2 months now. This is a major international corporation and I believe they are treating other suppliers like this, trying to make their Q1 performance look better than it is.

I consider this to be theft of service. Until they re-open their procurement/accounts payable system, they are in effect refusing to acknowledge that they owe anything.

Mel says:

March 23, 2012 at 1:38 pm

(Robert Reich wrote another post mentioning the “destruction of meaning”. Why can’t I find these things when I want references?)

Wait till you see their next move. They’re going to run Accounts Payable as a Profit Center. Because they can.

Lidia says:

March 23, 2012 at 7:43 pm

Is (isn’t) that how banks work?

As a small business person, I was shocked at the practices OF MY DEBTORS that pretended to keep me on the skids.

I was expected to be THEIR BANK, me! Someone who pulled in $50k, was fronting money to Siemans, Bard Medical and even larger, more obscure, companies whose names I now forget.

Obscene.

Planck says:

March 24, 2012 at 8:58 am

We saw this recently too…major corporations who don’t think they have to pay suppliers. Also, procurement officers who want 5% off the top of everything to justify their measily paper pushing jobs for profits that roll up to some Family Office somewhere.

Now LAS might have some creative routes for recourse (say drafting a press release from Concerned Big Multinational Suppliers expressing concern that the mysterious shuttering of the purchase department might be a sign that Big Multinational is in very bad financial shape because it is taking such desperate measures, faxing it to the corporate communications office from a Kinkos so as to disguise the source, with a list of financial websites and websites to whom it will be sent if checks are not forthcoming in a week. That might get their attention). But it is grotesque that we are even having to discuss taking extreme measures to get paid. LAS’s company is a victim of theft, period.

Guest blogger and author of On Value and Values Doug Smith took note of the LAS story and e-mailed:

It all reminded me of two things: specifically, the Morgan Stanley guy who is charged with stabbing the cab driver – and more generally a profoundly important shift that is already happening in society/capitalism/markets.

Business used to be based on cultivating critical relationships: with customers, employees, suppliers. Capitalism has not simply abandoned a relationship orientation, but has rapidly moved through “transactions” to “options.”

Today, everything is just an option. As deleterious as transaction orientation is to relationships, at least transactions have the constraints of obligations to follow through. But in our current raging and out of control homo economicus-as-options situation, not even that exists. There are no contractual obligations whatsoever.. there are only new negotiating positions tied to option values.

When the corporation in LAS’s initial comment above refuses to accept the invoice for services, it is merely exercising its option choice — likely under the belief that any cost (whether legal or otherwise) will be less than paying the invoice.

This is the world in which William Bryan Jennings operates. The driver’s account is credible, because it reflects this new business reality. When the cab pulled into the driveway, Jennings — just out of habit, routine and practice — treated the ‘agreed upon transaction amount’ as a mere option to be exercised through a new transaction/renegotiation. What the cabbie recalled as a contract for $204 became, if I remember, an option to pay $50.

In a world of relationships, those relationships had value beyond ‘just one damn transaction after another’…. and this goes missing in a world of transactions… but, in a world where every moment is just that moment’s options … not even previous promises have any stable value, let alone relationships …. and this is the dog now, not the tail.

Now there are settings in which not having a contract can work, but those are where relationships matter. When I worked with in Japan in the 1980s, the entire society was non-contractual. You’d have a vague understanding (Japanese is a vague language, being explicit is seen as tiresome and rude) and the two parties would keep arguing about what the deal was as they worked together. But there was a well understood, well shared set of norms, and it was a shame based culture, so word getting out that one party had been abusive would have led it to be hectored and shunned by others.

With a rise in an options-based view of business, it isn’t hard to see how a pernicious dynamic sets in. It used to be that only occasional scumbags would behave this way, and you’d write it off as bad luck and a reminder to do a decent amount of due diligence on new customers. But when this sort of behavior becomes common, the cost of doing business escalates since no one can trust anyone’s commitments. You can see this now in the way many types of contracts have changed. It used to be possible to do business with a short agreement. In many fields, they’ve now become excruciatingly long, since the odds of them being litigated is correctly seen as higher, so nailing down all sorts of possible outcomes is more important. And longer agreements means more protracted negotiations. It amounts to a tax on commerce.

And this pattern is particularly devastating to small businesses. It’s comical to see the Administration talk up the need to help entrepreneurs yet gut the rule of law to help banks. The last time I had to think about suing someone (more than 10 years ago), the rule of thumb was that it didn’t make sense to litigate unless the matter at hand was at least $300,000, between the hard dollar costs (you can get to $50,000 in legal and not be very far along) as well as the management distraction and emotional toll. Adjusting for inflation alone, the number has to be even higher now.

And the power imbalance does not have to be of the big company versus small one sort. It can be informational. As we wrote in ECONNED:

When the seller knows more than the buyer (or vice versa), commerce in the neoclassical framework becomes costly. One option is dealing only with vendors a buyer has used before successfully. Even then, he runs the risk that the seller pulls a fast one now and again, taking advantage of him in ways he cannot readily detect.

If sellers cannot be presumed to be trustworthy (and the dictates of maximizing self-interest say they in fact won’t be), consumers have to either spend money and effort to validate the quality of their purchase or accept the risk of being cheated.

Consider purchasing a computer in the neoclassical paradigm. The buyer has no way of being certain that the computer lives up to the vendor’s promises. So the consumer will have to bring an expert to test the computer’s functionality at the time of purchase (does it really have the memory and chip speed promised, for instance?). The seller will need to be paid in cash, otherwise the buyer could revoke payment.

And what happens if the computer fails in a few weeks? Assuming the vendor has not fled the jurisdiction, the only remedy is litigation, or an enforcer with brass knuckles.

But even that scenario is too simplistic. It assumes the buyer can evaluate the expert. But in fact, if you aren’t a computer professional, you can’t readily assess the competence of someone who has expertise you lack. And even if the person you hired is competent, he might arrange to get a kickback from the seller for endorsing shoddy goods. The same problem holds true in any area of specialized skills, such as accounting, the law, or finance. Many people judge service quality by bedside manner, which is not necessarily a good proxy for the quality of the substantive advice. And as we will see later, one of the factors that helped create the crisis was the willingness of investors to buy complicated financial products based on the recommendation of a salesman who did not have the buyers’ best interests at heart.

We can see the damage of the breakdown of the norms of commerce. The private label securitization market, which functioned fairly well when originators and servicers acted in accordance with their agreements with investors, is now dead. The securitization market, which was 60% private label prior to the crisis, is now effectively 100% government guaranteed (there was all of one private label deal last year). Various reform proposals have been suggested; some have been well thought out enough that past investors reacted positively. But of course, the sell side nixed anything far-reaching enough to make a real difference. The investors I know say there won’t be a private label securitization market ex root and branch changes for at least ten years.

So it looks like Marx is being proven correct, that capitalism sows the seeds of its own destruction, although not by the route he envisaged, that of a worker revolt. Instead, it comes about via the capitalists turning on each other to try to secure an even better deal.

And conditions on the ground are even worse. Hoisted from comments:

LAS says:

March 23, 2012 at 10:41 am

I think you are on to something, Yves.

There’s no indication of improvement either.

For an example, our firm completed work for a major corporation last month (successfully) and they will not accept the invoice for our work. While we have had to lay out cash to perform the work, they have not. Although they came to us to do the work for them, they have shut down their procurement/accounts payable dept and they have kept it shut for about 2 months now. This is a major international corporation and I believe they are treating other suppliers like this, trying to make their Q1 performance look better than it is.

I consider this to be theft of service. Until they re-open their procurement/accounts payable system, they are in effect refusing to acknowledge that they owe anything.

Mel says:

March 23, 2012 at 1:38 pm

(Robert Reich wrote another post mentioning the “destruction of meaning”. Why can’t I find these things when I want references?)

Wait till you see their next move. They’re going to run Accounts Payable as a Profit Center. Because they can.

Lidia says:

March 23, 2012 at 7:43 pm

Is (isn’t) that how banks work?

As a small business person, I was shocked at the practices OF MY DEBTORS that pretended to keep me on the skids.

I was expected to be THEIR BANK, me! Someone who pulled in $50k, was fronting money to Siemans, Bard Medical and even larger, more obscure, companies whose names I now forget.

Obscene.

Planck says:

March 24, 2012 at 8:58 am

We saw this recently too…major corporations who don’t think they have to pay suppliers. Also, procurement officers who want 5% off the top of everything to justify their measily paper pushing jobs for profits that roll up to some Family Office somewhere.

Now LAS might have some creative routes for recourse (say drafting a press release from Concerned Big Multinational Suppliers expressing concern that the mysterious shuttering of the purchase department might be a sign that Big Multinational is in very bad financial shape because it is taking such desperate measures, faxing it to the corporate communications office from a Kinkos so as to disguise the source, with a list of financial websites and websites to whom it will be sent if checks are not forthcoming in a week. That might get their attention). But it is grotesque that we are even having to discuss taking extreme measures to get paid. LAS’s company is a victim of theft, period.

Guest blogger and author of On Value and Values Doug Smith took note of the LAS story and e-mailed:

It all reminded me of two things: specifically, the Morgan Stanley guy who is charged with stabbing the cab driver – and more generally a profoundly important shift that is already happening in society/capitalism/markets.

Business used to be based on cultivating critical relationships: with customers, employees, suppliers. Capitalism has not simply abandoned a relationship orientation, but has rapidly moved through “transactions” to “options.”

Today, everything is just an option. As deleterious as transaction orientation is to relationships, at least transactions have the constraints of obligations to follow through. But in our current raging and out of control homo economicus-as-options situation, not even that exists. There are no contractual obligations whatsoever.. there are only new negotiating positions tied to option values.

When the corporation in LAS’s initial comment above refuses to accept the invoice for services, it is merely exercising its option choice — likely under the belief that any cost (whether legal or otherwise) will be less than paying the invoice.

This is the world in which William Bryan Jennings operates. The driver’s account is credible, because it reflects this new business reality. When the cab pulled into the driveway, Jennings — just out of habit, routine and practice — treated the ‘agreed upon transaction amount’ as a mere option to be exercised through a new transaction/renegotiation. What the cabbie recalled as a contract for $204 became, if I remember, an option to pay $50.

In a world of relationships, those relationships had value beyond ‘just one damn transaction after another’…. and this goes missing in a world of transactions… but, in a world where every moment is just that moment’s options … not even previous promises have any stable value, let alone relationships …. and this is the dog now, not the tail.

Now there are settings in which not having a contract can work, but those are where relationships matter. When I worked with in Japan in the 1980s, the entire society was non-contractual. You’d have a vague understanding (Japanese is a vague language, being explicit is seen as tiresome and rude) and the two parties would keep arguing about what the deal was as they worked together. But there was a well understood, well shared set of norms, and it was a shame based culture, so word getting out that one party had been abusive would have led it to be hectored and shunned by others.

With a rise in an options-based view of business, it isn’t hard to see how a pernicious dynamic sets in. It used to be that only occasional scumbags would behave this way, and you’d write it off as bad luck and a reminder to do a decent amount of due diligence on new customers. But when this sort of behavior becomes common, the cost of doing business escalates since no one can trust anyone’s commitments. You can see this now in the way many types of contracts have changed. It used to be possible to do business with a short agreement. In many fields, they’ve now become excruciatingly long, since the odds of them being litigated is correctly seen as higher, so nailing down all sorts of possible outcomes is more important. And longer agreements means more protracted negotiations. It amounts to a tax on commerce.

And this pattern is particularly devastating to small businesses. It’s comical to see the Administration talk up the need to help entrepreneurs yet gut the rule of law to help banks. The last time I had to think about suing someone (more than 10 years ago), the rule of thumb was that it didn’t make sense to litigate unless the matter at hand was at least $300,000, between the hard dollar costs (you can get to $50,000 in legal and not be very far along) as well as the management distraction and emotional toll. Adjusting for inflation alone, the number has to be even higher now.

And the power imbalance does not have to be of the big company versus small one sort. It can be informational. As we wrote in ECONNED:

When the seller knows more than the buyer (or vice versa), commerce in the neoclassical framework becomes costly. One option is dealing only with vendors a buyer has used before successfully. Even then, he runs the risk that the seller pulls a fast one now and again, taking advantage of him in ways he cannot readily detect.

If sellers cannot be presumed to be trustworthy (and the dictates of maximizing self-interest say they in fact won’t be), consumers have to either spend money and effort to validate the quality of their purchase or accept the risk of being cheated.

Consider purchasing a computer in the neoclassical paradigm. The buyer has no way of being certain that the computer lives up to the vendor’s promises. So the consumer will have to bring an expert to test the computer’s functionality at the time of purchase (does it really have the memory and chip speed promised, for instance?). The seller will need to be paid in cash, otherwise the buyer could revoke payment.

And what happens if the computer fails in a few weeks? Assuming the vendor has not fled the jurisdiction, the only remedy is litigation, or an enforcer with brass knuckles.

But even that scenario is too simplistic. It assumes the buyer can evaluate the expert. But in fact, if you aren’t a computer professional, you can’t readily assess the competence of someone who has expertise you lack. And even if the person you hired is competent, he might arrange to get a kickback from the seller for endorsing shoddy goods. The same problem holds true in any area of specialized skills, such as accounting, the law, or finance. Many people judge service quality by bedside manner, which is not necessarily a good proxy for the quality of the substantive advice. And as we will see later, one of the factors that helped create the crisis was the willingness of investors to buy complicated financial products based on the recommendation of a salesman who did not have the buyers’ best interests at heart.

We can see the damage of the breakdown of the norms of commerce. The private label securitization market, which functioned fairly well when originators and servicers acted in accordance with their agreements with investors, is now dead. The securitization market, which was 60% private label prior to the crisis, is now effectively 100% government guaranteed (there was all of one private label deal last year). Various reform proposals have been suggested; some have been well thought out enough that past investors reacted positively. But of course, the sell side nixed anything far-reaching enough to make a real difference. The investors I know say there won’t be a private label securitization market ex root and branch changes for at least ten years.