Central Banks Act With a New Boldness ... When James Bullard, president of the Federal Reserve Bank of St. Louis, arrived in Frankfurt last week, he issued an unusual public warning to the European Central Bank: Be bolder. Central bankers, anywhere in the world, are a cautious lot. They prefer slow and steady over the dramatic gesture. And they rarely go public with criticisms of other central banks. But the economic stagnation of the major developed nations has driven central banks in the United States, Japan, Britain and the European Union to take increasingly aggressive action. – New York Times

Dominant Social Theme: The good, gray men have their collective hand on the tiller and can steer us to safety.

Free-Market Analysis: This article is a companion piece to our lead story this issue (see above) and provides more evidence that one needs to look at patterns and promotions rather than taking pronouncements at face value when it comes to world affairs.

Of course, the article (excerpted above) does seem logical in that we know central bankers are concerned about lagging economies and believe they can debase currency (print money) to stimulate "growth."

But if one utilizes the correct terminology (debase) and tracks the manifestations of debasement around the world, one can come to several conclusions.

First, an uneasy balance is being sought between "revolution and recovery" – that is, those in charge of central banking policies around the world are trying to push the entire financial system toward more centralization and, at the same time, avoid outright rebellion in Europe, the US and elsewhere where these policies are taking hold with perhaps unexpected viciousness.

There is nothing especially controversial, in our view, about postulating that there is a new global economic system in the making because the same powers now in charge previously created the building blocks for this system after the Second World War.

The UN, the IMF, the World Bank and various international trade organizations still exist today and have more power than ever. Now they are being employed in the service perhaps of the evolution of the post-war environment, which was quasi-globalist but had a long way to go.

Today, it seems, we are observing the glimmers of a new paradigm, though unlike Bretton Woods, we are not yet being informed of its fullness. That is perhaps because those supporting these changes do not have a full-fledged crisis to justify what's taking place. Thus a need for secrecy.

Nonetheless, we can see a process unfolding and would be foolish, in the scheme of things, simply to discount it. Rather than war, it is the global downturn itself that is providing the beginnings of a justification for some of the moves being made, specifically the worldwide effort to reinflate (debase). Here's more from the article:

Because governments are not taking steps to revive economies, like increasing spending or cutting taxes, the traditional concern of central bankers that economic growth will cause too much inflation has been supplanted by the fear that growth is not fast enough to prevent deflation, or falling prices.

The Fed has announced plans to keep borrowing costs at historic lows until unemployment declines. The staid Bank of England has bought more than a half-trillion dollars' worth of bonds to ignite British business activity. Last month, Haruhiko Kuroda, the new chairman of the Bank of Japan, steered the central bank toward an audacious new policy of reinflating the Japanese economy by doubling the money supply. It is considered the boldest step so far by a central bank.

So far, the results of these activist central banks have fallen short of expectations. "I'm not sure why we're not getting more response," said Donald L. Kohn, a former Federal Reserve vice chairman who is now at the Brookings Institution. "Maybe we've made some progress in identifying some of the causes, but it's not fully satisfying why we have negative real interest rates everywhere in the industrial world and so little growth."

... The Federal Reserve in the United States has been significantly more aggressive since December 2008, when the Fed reduced its benchmark short-term interest rate nearly to zero. Ever since, it has pursued a pair of experiments aimed at dragging other interest rates closer to zero, too. The Fed has tried to bolster confidence that rates will stay low by talking more about the future.

The article's ultimate point is that throughout the West, central bankers are getting more aggressive about printing money and are doing it in bolder ways. Actually, we'd argue that these good, gray men have been doing pretty much what they've wanted for a century, only they have never admitted to the fullness of their manipulations in the past.

Unlike Mr. Kohn, we are not surprised at the failure of these manipulations to perform as advertised. Monetary debasement funneled through financial vehicles and into various stock markets is an incredibly tedious and complex way to "stimulate." But it is necessary if one wants to 1) draw out the pain and 2) control the process.

It sounds rash, perhaps, to accuse central bankers of wanting to prolong the current economic crisis but to us it seems inescapable. The monetary debasement probably will only end when economies finally roar back to life in all their distorted and maniacal glory.

By not allowing economies to purge themselves of failed business and corporations, top central bankers have guaranteed that whatever "recovery" actually occurs will be one that includes manifold bubbles and distortions.

Such recoveries will also boost interest rates, inevitably, giving rise to further crises. These crises will, in our view, be critical and unavoidable. As the world's financial economy threatens to collapse, cries will be raised for a new "Bretton Woods" and a new and more comprehensively global monetary pact. One guess, anyway.

You may disagree with this scenario, dear reader, but can you discount it outright? Accept it may have a correlation to reality and one then must harbor a suspicion that articles like the one we are commenting on are not properly explaining reality.

In fact, the ultimate aim here may be to CREATE a further crisis in order to resolve it.

This is certainly a cynical analysis but can we say with certainty it has never been tried before?

Conclusion: Don't believe everything you read, even in the New York Times.

Source

DAILY BUSINESS REPORT - Financial Updates, International Markets and Business News

May 31, 2013

May 30, 2013

Volcker On Bernanke's Grand Monetary Experiment: "Good Luck In That"

A week ago, in a very comic interlude, the hawkish head of the only G-7 country to have experienced hyperinflation in the recent past - Bundesbank's Jens Weidmann - had some sobering words of encouragement for his Japanese colleague Kuroda: "I wish them luck in their experiments."

Now, another former central bank head, the most famous one of the 1980s, and the man thanks to whom America did not implode in a depressionary puff of runaway inflation, Greenspan's predecessor Paul Volcker, has taken the podium and made a mockery of the entire fallback premise on which Bernanke's house of manipulated, centrally-planned cards is built: his assumption that no matter how much deferred inflation is injected, that Bernanke needs just "15 minutes" to take it away. Better yet, and as Japan has recently seen: the fact that central bank credibility is slowly but surely starting to slip away - first visible in rapid rises in bond yields, then in a surge in bond volatility, and finally: an all out inflationary conflagration.

Quote Volcker:

Source

Now, another former central bank head, the most famous one of the 1980s, and the man thanks to whom America did not implode in a depressionary puff of runaway inflation, Greenspan's predecessor Paul Volcker, has taken the podium and made a mockery of the entire fallback premise on which Bernanke's house of manipulated, centrally-planned cards is built: his assumption that no matter how much deferred inflation is injected, that Bernanke needs just "15 minutes" to take it away. Better yet, and as Japan has recently seen: the fact that central bank credibility is slowly but surely starting to slip away - first visible in rapid rises in bond yields, then in a surge in bond volatility, and finally: an all out inflationary conflagration.

Quote Volcker:

Hopefully Volcker can be cryogenically frozen because when the Chairsatan eventually - and it is only a matter of time - loses control and all hell breaks lose, none of the muppets in the Marriner Eccles building, no click-baiting Nobel-winning trolling Op-Ed writer with socialist delusions of grandure, will have any idea what to do, and it will be someone like Paul who will be needed to unleash his magic once more. Sadly, we have the sinking suspiction that not even thawed out of carbonite, will Volcker have any success when faced with the Frankenstein monster that the MIT central-banking braintrust have managed to unleash.“The Federal Reserve, any central bank, should not be asked to do too much to undertake responsibilities that it cannot responsibly meet with its appropriately limited powers,” Volcker said. He said a central bank’s basic responsibility is for a “stable currency.”

“Credibility is an enormous asset,” Volcker said. “Once earned, it must not be frittered away by yielding to the notion that a little inflation right now is a good a thing, a good thing to release animal spirits and to pep up investment.”

“The implicit assumption behind that siren call must be that the inflation rate can be manipulated to reach economic objectives,” according to Volcker. “Up today, maybe a little more tomorrow and then pulled back on command. Good luck in that. All experience demonstrates that inflation, when fairly and deliberately started, is hard to control and reverse.”

Source

May 29, 2013

Is EVERY Market Rigged?

European Union Launches Investigation Into Manipulation of Oil Prices Since 2002

CNN reports:The European Commission raided the offices of Shell, BP and Norway’s Statoil this week as part of an investigation into suspected attempts to manipulate global oil prices spanning more than a decade.

None of the companies have been accused of wrongdoing, but the controversy has brought back memories of the Libor rate-rigging scandal that rocked the financial world last year.

***

A review ordered by the British government last year in the wake of the Libor revelations cited “clear” parallels between the work of the oil-price-reporting agencies and Libor.

“[T]hey are both widely used benchmarks that are compiled by private organizations and that are subject to minimal regulation and oversight by regulatory authorities,” the review, led by former financial regulator Martin Wheatley, said in August . “To that extent they are also likely to be vulnerable to similar issues with regards to the motivation and opportunity for manipulation and distortion.”

***

In a report issued in October, the International Organization of Securities Commissions — an association of regulators — said the ability “to selectively report data on a voluntary basis creates an opportunity for manipulating the commodity market data” submitted to Platts and its competitors.

Responding to questions from IOSCO last year, French oil giant Total said the price-reporting agencies, or PRAs, sometimes “do not assure an accurate representation of the market and consequently deform the real price levels paid at every level of the price chain, including by the consumer.” But Total called Platts and its competitors “generally… conscientious and professional.”

***USA Today notes:

“Even small distortions of assessed prices may have a huge impact on the prices of crude oil, refined oil products and biofuels purchases and sales, potentially harming final consumers,” the European Commission said this week.

The Commission … said, however, that its probe covers a wide range of oil products — crude oil, biofuels, and refined oil products, which include gasoline, heating oil, petrochemicals and others.

***

The EU said it has concerns that some companies may have tried to manipulate the pricing process by colluding to report distorted prices and by preventing other companies from submitting their own prices.

***

Unlike oil futures, which set prices for contracts, the data used in the MOC process is based on the physical sale and purchase of actual shipments of oil and oil products.

***Fox points out:

According to Statoil, the EU investigation stretches back to 2002, which is when Platts launched its MOC price system in Europe. The suspicion is that some companies may have provided inaccurate information to Platts to affect the oil products’ pricing, presumably for financial gain.

At issue is whether there was collusion to distort prices of crude, refined oil products and ethanol traded during Platts’ market-on-close (MOC) system – a daily half-hour “window” in which it sets prices.

But the European Commission also is examining whether companies were prevented from taking part in the price assessment process.The Guardian writes:

The commission said the alleged price collusion, which may have been going on since 2002, could have had a “huge impact” on the price of petrol at the pumps “potentially harming final consumers”.

Lord Oakeshott, former Liberal Democrat Treasury spokesman, said the alleged rigging of oil prices was “as serious as rigging Libor” – which led to banks being fined hundreds of millions of pounds.

He demanded to know why the UK authorities had not taken action earlier and said he would ask questions of the British regulator in Parliament. “Why have we had to wait for Brussels to find out if British oil giants are ripping off British consumers?” he said. “The price of energy ripples right through our economy and really matters to every business and families.”

***

Shadow energy and climate change secretary Caroline Flint said: “These are very concerning reports, which if true, suggest shocking behaviour in the oil market that should be dealt with strongly.

“When the allegations of price fixing in the gas market were made, Labour warned that opaque over-the-counter deals and relying on price reporting agencies left the market vulnerable to abuse.

“These latest allegations of price fixing in the oil market raise very similar questions. Consumers need to know that the prices they pay for their energy or petrol are fair, transparent and not being manipulated by traders.”

Shadow financial secretary to the Treasury Chris Leslie said: “If oil price fixing has taken place it would be a shocking scandal for our financial markets.The Telegraph reports:

“97 per cent of all we eat, drink, wear or build has spent some time in a diesel lorry,” said a spokesman for FairFuel UK, the lobbyists. “If it is proved, they have been gambling with the very oxygen of our economy.”

***The New York Times notes of agencies like Platt and Argus Media:

Platts – to determine the benchmark price – examines just trades in the final 30 minutes of the trading day. A group of half a dozen analysts gather round a trading screen and decide on the final price. As with much that goes on in the City, it is a surprisingly old-fashioned method, reliant on gentlemanly conduct. Critics say it leaves the market open to abuse, and the price can suddenly spike or fall in the final minutes of the day.

Their influence is extensive. Total, the French oil giant, estimated last year that 75 to 80 percent of crude oil and refined product transactions were linked to the prices published by such agencies.The Observer writes that manipulation of the oil markets has long been an open secret:

Robert Campbell, a former price reporter at another PRA, Argus – he is now a staffer at Thomson Reuters, which also competes with Platts and others on providing energy news and data – said this a few days ago in a little-noticed commentary: “The vulnerability of physical crude price assessments to manipulation is an open secret within the oil industry. The surprise is that it took regulators so long to open a formal probe.”Reuters points out that the probe may be expanding to the U.S.:

In Washington, the chairman of the Senate energy committee asked the Justice Department to investigate whether alleged price manipulation has boosted fuel prices for U.S. consumers.

“Efforts to manipulate the European oil indices, if proven, may have already impacted U.S. consumers and businesses, because of the interrelationships among world oil markets and hedging practices,” Sen. Ron Wyden (D-Ore.), chairman of the Senate Energy and Natural Resources Committee, wrote in a letter to Attorney General Eric H. Holder Jr.

Wyden also asked Justice to investigate whether oil market manipulation was taking place in the United States.Not only are petroleum products a multi-trillion dollar market on their own, but manipulation of petroleum prices would effect virtually every market in the world.

For example, the Cato Institute notes how many industries use oil:

U.S. industries use petroleum to produce the synthetic fiber used in textile mills making carpeting and fabric from polyester and nylon. U.S. tire plants use petroleum to make synthetic rubber. Other U.S. industries use petroleum to produce plastic, drugs, detergent, deodorant, fertilizer, pesticides, paint, eyeglasses, heart valves, crayons, bubble gum and Vaseline.The India Times explains that:

The price variation in crude oil impacts the sentiments and hence the volatility in stock markets all over the world. The rise in crude oil prices is not good for the global economy. Price rise in crude oil virtually impacts industries and businesses across the board. Higher crude oil prices mean higher energy prices, which can cause a ripple effect on virtually all business aspects that are dependent on energy (directly or indirectly).The Federal Reserve Bank of San Francisco points out:

When gasoline prices increase, a larger share of households’ budgets is likely to be spent on it, which leaves less to spend on other goods and services. The same goes for businesses whose goods must be shipped from place to place or that use fuel as a major input (such as the airline industry). Higher oil prices tend to make production more expensive for businesses, just as they make it more expensive for households to do the things they normally do.

***

Oil price increases are generally thought to increase inflation and reduce economic growth.

***

Oil prices indirectly affect costs such as transportation, manufacturing, and heating. The increase in these costs can in turn affect the prices of a variety of goods and services, as producers may pass production costs on to consumers.

***

Oil price increases can also stifle the growth of the economy through their effect on the supply and demand for goods other than oil. Increases in oil prices can depress the supply of other goods because they increase the costs of producing them. In economics terminology, high oil prices can shift up the supply curve for the goods and services for which oil is an input.

High oil prices also can reduce demand for other goods because they reduce wealth, as well as induce uncertainty about the future (Sill 2007). One way to analyze the effects of higher oil prices is to think about the higher prices as a tax on consumers (Fernald and Trehan 2005).The Post Carbon Institute notes (via OilPrice.com) that high oil prices raise food prices as well:

The connection between food and oil is systemic, and the prices of both food and fuel have risen and fallen more or less in tandem in recent years (figure 1). Modern agriculture uses oil products to fuel farm machinery, to transport other inputs to the farm, and to transport farm output to the ultimate consumer. Oil is often also used as input in agricultural chemicals. Oil price increases therefore put pressure on all these aspects of commercial food systems.

Figure 1: Evolution of food and fuel prices, 2000 to 2009

Sources: US Energy Information Administration and FAO.

Economists Nouriel Roubini and Setser note that all recessions after 1973 were associated with oil shocks.

Interest Rates Are Manipulated

Unless you live under a rock, you know about the Libor scandal.For those just now emerging from a coma, here’s a recap:

- The big banks have conspired for years to rig interest rates … upon which $800 trillion in assets are pegged

- This was the largest insider trading scandal ever … and the largest financial scam in world history

- Local governments got ripped off bigtime by the Libor manipulation

- Libor is still being manipulated

Derivatives Are Manipulated

The big banks have long manipulated derivatives … a $1,200 Trillion Dollar market.Indeed, many trillions of dollars of derivatives are being manipulated in the exact same same way that interest rates are fixed: through gamed self-reporting.

Gold and Silver Are Manipulated

The Guardian and Telegraph report that gold and silver prices are “fixed” in the same way as interest rates and derivatives – in daily conference calls by the powers-that-be.Everything Can Be Manipulated through High-Frequency Trading

Traders with high-tech computers can manipulate stocks, bonds, options, currencies and commodities. And see this.Manipulating Numerous Markets In Myriad Ways

The big banks and other giants manipulate numerous markets in myriad ways, for example:- Shaving money off of virtually every pension transaction they handled over the course of decades, stealing collectively billions of dollars from pensions worldwide. Details here, here, here, here, here, here, here, here, here, here, here and here

- Charging “storage fees” to store gold bullion … without even buying or storing any gold . And raiding allocated gold accounts

- Committing massive and pervasive fraud both when they initiated mortgage loans and when they foreclosed on them (and see this)

- Pledging the same mortgage multiple times to different buyers. See this, this, this, this and this. This would be like selling your car, and collecting money from 10 different buyers for the same car

- Cheating homeowners by gaming laws meant to protect people from unfair foreclosure

- Pushing investments which they knew were terrible, and then betting against the same investments to make money for themselves. See this, this, this, this and this

- Engaging in unlawful “frontrunning” to manipulate markets. See this, this, this, this, this and this

- Charging veterans unlawful mortgage fees

- Cooking their books (and see this)

May 28, 2013

The Japanese Financial System Is Beginning To Spin Wildly Out Of Control

The financial system of the third largest economy on the planet is starting to come apart at the seams, and the ripple effects are going to be felt all over the globe. Nobody knew exactly when the Japanese financial system was going to begin to implode, but pretty much everyone knew that a day of reckoning for Japan was coming eventually. After all, the Japanese economy has been in a slump for over a decade, Japan has a debt to GDP ratio of well over 200 percent and they are spending about 50 percent of all tax revenue on debt service. In a desperate attempt to revitalize the economy and reduce the debt burden, the Bank of Japan decided a few months ago to start pumping massive amounts of money into the economy. At first, it seemed to be working. Economic activity perked up and the Japanese stock market went on a tremendous run. Unfortunately, there is also a very significant downside to pumping your economy full of money. Investors start demanding higher returns on their money and interest rates go up. But the Japanese government cannot afford higher interest rates. Without super low interest rates, Japanese government finances would totally collapse. In addition, higher interest rates in the private sector would make it much more difficult for the Japanese economy to expand. In essence, pretty much the last thing that Japan needs right now is significantly higher interest rates, but that is exactly what the policies of the Bank of Japan are going to produce.

There is a lot of fear in Japan right now. On Thursday, the Nikkei plunged 7.3 percent. That was the largest single day decline in more than two years. Then on Monday the index fell by another 3.2 percent.

And according to Business Insider, things are not looking good for Tuesday at this point...

The term "currency war" is something that you are going to hear a lot more over the next few years, and what you can see in the chart above is only the beginning.

What the Bank of Japan is doing right now is absolutely unprecedented. It has announced that it plans to inject the equivalent of approximately $1.4 trillion into the Japanese economy in less than two years.

As Kyle Bass recently discussed, that dwarfs the quantitative easing that the Federal Reserve has been doing...

Because Japan has a debt to GDP ratio of more than 200 percent, the only way that it can avoid a total meltdown of government finances is to have super low interest rates. The video posted below does a great job of elaborating on this point...

It really is very simple. If interest rates rise substantially, Japan will be done.

Investor Kyle Bass is one of those that have been warning about this for a long time...

And what is happening right now in Japan should serve as a sober warning to the United States. Like Japan, the money printing that the Federal Reserve has been doing has caused economic activity to perk up a bit and it has sent the stock market on an unprecedented run.

Unfortunately, no bubble that the Federal Reserve has ever created has been able to last forever. At some point, we will pay a very great price for all of the debt that the U.S. government has been accumulating and all of the reckless money printing that the Fed has been engaged in.

So enjoy the calm before the storm while you still can.

It won't last for long.

Source

There is a lot of fear in Japan right now. On Thursday, the Nikkei plunged 7.3 percent. That was the largest single day decline in more than two years. Then on Monday the index fell by another 3.2 percent.

And according to Business Insider, things are not looking good for Tuesday at this point...

In post-close futures trading, the Nikkei has dropped by another couple hundred points, and has dropped below 14,000.Are we witnessing the beginning of a colossal financial meltdown by the third largest economy on the planet? The Bank of Japan is starting to lose control, and if Japan goes down hard the crisis could spread to Europe and North America very rapidly. The following is from a recent article by Graham Summers...

As Japan has indicated, when bonds start to plunge, it’s not good for stocks. Today the Japanese Bond market fell and the Nikkei plunged 7%. The entire market down 7%… despite the Bank of Japan funneling $19 billion into it to hold things together.

This is what it looks like when a Central Bank begins to lose control. And what’s happening in Japan today will be coming to the US in the not so distant future.

If you think the Fed is not terrified of this, think again. The Fed has pumped over $1 trillion into foreign banks, hoping to stop the mess from getting to the US. As Japan is showing us, the Fed will fail.

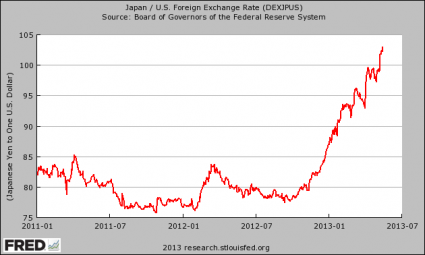

Investors, take note… the financial system is sending us major warnings…And all of this money printing is absolutely crushing the Japanese yen. Since the start of 2013, the yen has declined 16 percent against the U.S. dollar, even though the U.S. dollar is also being rapidly debased. Just check out this chart of the yen vs. the U.S. dollar. It is absolutely stunning...

If you are not already preparing for a potential market collapse, now is the time to be doing so.

The term "currency war" is something that you are going to hear a lot more over the next few years, and what you can see in the chart above is only the beginning.

What the Bank of Japan is doing right now is absolutely unprecedented. It has announced that it plans to inject the equivalent of approximately $1.4 trillion into the Japanese economy in less than two years.

As Kyle Bass recently discussed, that dwarfs the quantitative easing that the Federal Reserve has been doing...

"What they're doing represents 70% of what the Fed is doing here with an economy 1/3 the size of ours"The big problem for Japan will come when government bond yields really start to rise. The yield on 10 year government bonds has been creeping up over the past few months, and if they hit the 1.0% mark that will set off some major red flags.

Because Japan has a debt to GDP ratio of more than 200 percent, the only way that it can avoid a total meltdown of government finances is to have super low interest rates. The video posted below does a great job of elaborating on this point...

It really is very simple. If interest rates rise substantially, Japan will be done.

Investor Kyle Bass is one of those that have been warning about this for a long time...

There's a fatalism, he says, in everyone he talks to in Japan. Their thinking is changing, and the way they talk to him about debt is changing. They already spend 50% of tax revenue on debt service.The financial problems in Cyprus and Greece are just tiny blips compared to what a major financial crisis in Japan would potentially be like. The Japanese economy is larger than the economies of Germany and Italy combined. If the house of cards in Japan comes tumbling down, trillions of dollars of investments all over the globe are going to be affected.

"If rates go up, it's game over."

And what is happening right now in Japan should serve as a sober warning to the United States. Like Japan, the money printing that the Federal Reserve has been doing has caused economic activity to perk up a bit and it has sent the stock market on an unprecedented run.

Unfortunately, no bubble that the Federal Reserve has ever created has been able to last forever. At some point, we will pay a very great price for all of the debt that the U.S. government has been accumulating and all of the reckless money printing that the Fed has been engaged in.

So enjoy the calm before the storm while you still can.

It won't last for long.

Source

May 27, 2013

IMF Rethinks Sovereign Defaults, Again

I noted back in January that the IMF had started to do its own “lessons learned” on its European financial crisis response and had begun to admit it had made some fairly terrible mistakes in its assessment of the debt sustainability of a number of nations, including Greece, under its current programs.

Late last week the IMF released another discussion paper (available below) that covers recent developments in sovereign debt restructures and their effect on IMF policy. The paper concludes that:

The paper discusses the implication of the ongoing litigation against Argentina as well as the experience of the fund in the recent case of Greece. Of note is the admission by the fund that it was forced to lower its assessment of the country due to contagion worries from the official sector in Europe:

There may be a case for exploring additional ways to limit the risk that Fund resources will simply be used to bail out private creditors.

For example, a presumption could be established that some form of a creditor bail-in measure would be implemented as a condition for Fund lending in cases where, although no clear-cut determination has been made that the debt is unsustainable, the member has lost market access and prospects for regaining market access are uncertain.

In such cases, the primary objective of creditor bail-in would be designed to ensure that creditors would not exit during the period while the Fund is providing financial assistance. This would also give more time for the Fund to determine whether the problem is one of liquidity or solvency. Accordingly, the measures would typically involve a rescheduling of debt, rather than the type of debt stock reduction that is normally required in circumstances where the debt is judged to be unsustainable.

Providing the member with a more comfortable debt profile would also have the additional benefit of enhancing market confidence in the feasibility of the member’s adjustment efforts, thereby reducing the risk that the debt will, in fact, become unsustainable. While bail-in measures would be voluntary (ranging from rescheduling of loans to bond exchanges that result in long maturities), creditors would understand that the success of such measures would be a condition for continued Fund support for the adjustment measures. Such a strategy—debt rescheduling instead of debt reduction—would not be appropriate when it is clear that the problem is one of solvency in which case reducing debt upfront to address debt overhang and restore sustainability would be the preferred course of action.

In light of the ongoing litigation against Argentina the paper also appears to be pushing for two things, firstly the introduction of a standard across-the-board mechanism to support collective action clauses, and resolution, within the sovereign debt markets:

It will be interesting to see if this paper has any effect on future programs, but it does appear, if only very slowly, that the IMF is learning from past mistakes and attempting to shift policy in a direction to address that issue. It would appear, at least from this paper, that the IMF will be demanding a more realistic assessment of the debt sustainability of target nations and a greater use of up-front restructuring as a per-requisite for program engagement. We’ll have to watch the next steps in Europe to determine if this is simply a talking point or something the IMF board will action.

Full paper below.

Source

Late last week the IMF released another discussion paper (available below) that covers recent developments in sovereign debt restructures and their effect on IMF policy. The paper concludes that:

First, debt restructurings have often been too little and too late, thus failing to re-establish debt sustainability and market access in a durable way. Overcoming these problems likely requires action on several fronts, including

(i) increased rigor and transparency of debt sustainability and market access assessments,Second, while creditor participation has been adequate in recent restructurings, the current contractual, market-based approach to debt restructuring is becoming less potent in overcoming collective action problems, especially in pre-default cases. In response, consideration could be given to making the contractual framework more effective, including through the introduction of more robust aggregation clauses into international sovereign bonds bearing in mind the inter-creditor equity issues that such an approach may raise. The Fund may also consider ways to condition use of its financing more tightly to the resolution of collective action problems;

(ii) exploring ways to prevent the use of Fund resources to simply bail out private creditors, and

(iii) measures to alleviate the costs associated with restructurings

Third, the growing role and changing composition of official lending call for a clearer framework for official sector involvement, especially with regard to non-Paris Club creditors, for which the modality for securing program financing commitments could be tightened; and

Fourth, although the collaborative, good-faith approach to resolving external private arrears embedded in the lending into arrears (LIA) policy remains the most promising way to regain market access post-default, a review of the effectiveness of the LIA policy is in order in light of recent experience and the increased complexity of the creditor base. Consideration could also be given to extending the LIA policy to official arrears.In short, the assessments of debt sustainability have been woeful, there aren’t strong enough binding terms (read CACS) in sovereign securities, the official sector, but not the IMF itself, need to play a part in defaults and the IMF should investigate the optimal debt resolution mechanisms available for negotiating between creditors and debtors.

The paper discusses the implication of the ongoing litigation against Argentina as well as the experience of the fund in the recent case of Greece. Of note is the admission by the fund that it was forced to lower its assessment of the country due to contagion worries from the official sector in Europe:

Accordingly, when a member’s sovereign debt is unsustainable and there are concerns regarding the contagion effects of a restructuring, providing large-scale financing without debt relief would only postpone the need to address the debt problem.In other words, Europe, and its banks, weren’t prepared for a Greek default so the IMF was forced to pretend that the country’s position was better than it actually was. That was obviously a mistake and the country, like many before it, was forced to take a second bailout followed by a re-structure that should have occurred up front. As noted by the paper:

Instead, the appropriate response would be to deal with the contagion effects of restructuring head-on by, for example, requiring that currency union authorities establish adequate safeguards promptly and decisively to cushion the effect of spillovers to other countries (via, e.g., proactive recapitalization of creditor banks, establishment of firewalls, and provision of liquidity support). In the context of the first Greece program, financial assistance was delayed until Greece had lost market access. In response to concerns about possible spillovers from debt restructuring, the Fund lowered the bar for exceptional access (second criterion) by creating an exception to the requirement for achieving debt sustainability with a high probability in the presence of systemic inter national spillover effects. In light of these issues, the modification of the exceptional access policy could usefully be reviewed

A review of the recent experience suggests that unsustainable debt situations often fester before they are resolved and, when restructurings do occur, they do not always restore sustainability and market access in a durable manner, leading to repeated restructurings. While the costs of delaying a restructuring are well recognized, pressures to delay can still arise due to the authorities’ concerns about financial stability and contagion. Delays were also sometimes facilitated by parallel incentives on the part of official creditors, who accordingly may have an interest in accepting, and pressuring the Fund to accept, sanguine assessments of debt sustainability and market reaccess.And:

In hindsight, the Fund’s assessments of debt sustainability and market access may sometimes have been too sanguine.

The existing DSA framework does not specify the period over which debt sustainability or market access is supposed to be achieved (although it is generally understood that debt would be sustainable within a five-year horizon) or how maximum sustainable debt ranges should be derived, leaving this mostly to Fund staff judgment. Sustainability was generally assessed on the basis of an eventual decline in the debt-to-GDP ratio—Argentina, Seychelles and St. Kitts and Nevis were the only three cases that provided for a quick and sizable reduction in the debt-to-GDP levels post-restructuring. St. Kitts and Nevis also targeted an explicit debt threshold, i.e., the ECCU debt target of 60 percent of GDP by 2020. Most other cases allowed more than five years for the debt level to fall significantly below safe levels.

For example, in Greece the debt-to-GDP ratio in the most recent program projections is not expected to be reduced substantially below 110 percent before 2022, while in the forthcoming Fund-supported program with Jamaica, debt is still projected to remain close to 120 percent of GDP in five years’ time. In Grenada, the debt ratio at the end of the five-year horizon actually turned out much higher than staff projections at the time of the restructuring. Also, in Greece, Jamaica (2010) and Seychelles, staff medium-term debt projections have been revised upward substantially within only a few years compared to projections made at the time of the restructurings.Also of note is the emphasis on the broader guidelines of the IMF programs , supporting countries sustainable return to private capital markets in a specific time-frame , and what that means in terms of the types of restructures that should be used and how, and when, the IMF can support them:

There may be a case for exploring additional ways to limit the risk that Fund resources will simply be used to bail out private creditors.

For example, a presumption could be established that some form of a creditor bail-in measure would be implemented as a condition for Fund lending in cases where, although no clear-cut determination has been made that the debt is unsustainable, the member has lost market access and prospects for regaining market access are uncertain.

In such cases, the primary objective of creditor bail-in would be designed to ensure that creditors would not exit during the period while the Fund is providing financial assistance. This would also give more time for the Fund to determine whether the problem is one of liquidity or solvency. Accordingly, the measures would typically involve a rescheduling of debt, rather than the type of debt stock reduction that is normally required in circumstances where the debt is judged to be unsustainable.

Providing the member with a more comfortable debt profile would also have the additional benefit of enhancing market confidence in the feasibility of the member’s adjustment efforts, thereby reducing the risk that the debt will, in fact, become unsustainable. While bail-in measures would be voluntary (ranging from rescheduling of loans to bond exchanges that result in long maturities), creditors would understand that the success of such measures would be a condition for continued Fund support for the adjustment measures. Such a strategy—debt rescheduling instead of debt reduction—would not be appropriate when it is clear that the problem is one of solvency in which case reducing debt upfront to address debt overhang and restore sustainability would be the preferred course of action.

In light of the ongoing litigation against Argentina the paper also appears to be pushing for two things, firstly the introduction of a standard across-the-board mechanism to support collective action clauses, and resolution, within the sovereign debt markets:

Recent experience indicates that the contractual, market-based approach has worked reasonably well in securing creditor participation and avoiding protracted negotiations. But these episodes have also foreshadowed potential collective action problems that could hamper future restructurings. These problems are most acute when a default has not yet occurred, large haircuts are needed to reestablish sustainability, and sovereign bond contracts do not include CACs. The ongoing Argentina litigation has exacerbated the collective action problem, by increasing leverage of holdout creditors. Assuming there continues to be lack of sufficient support within the membership for the type of statutory framework envisaged under the SDRM, avenues could be considered to strengthen the existing contractual framework.

—

These aspects of the Greek legislation resemble the aggregation features of the SDRM. The key differences between the framework envisaged under the SDRM and the Greek legislation is that the SDRM would be established through a universal treaty (rather than through domestic law),

apply to all debt instruments (and not just to bonds governed by domestic law), and be subject to the jurisdiction of an international forum (rather than the domestic courts of the member whose debt is being restructured). At this stage, there does not appear to be sufficient support within the membership to amend the Articles of Agreement to establish such a universal treaty.

—-

Complementing efforts to revamp CACs, the Fund may consider conditioning the availability of its financing more tightly to the resolution of collective action problems.

For instance, the use of high minimum participation thresholds could be required in debt exchange operations launched under Fund-supported programs to ensure broad creditor participation. Fund policy encourages members to avoid default to the extent possible, even after restructuring. An expectation of eventually being paid out in full may encourage holdouts. The use of high minimum participation thresholds would help reduce such incentives. The Fund could also routinely issue statements alerting creditors that securing a critical participation mass in the debt exchange would be required for the restoration of external stability—the implication being that failure to meet the

established minimum participation threshold would block future program financing, leaving no other option but default and protracted arrears.

Also, in pre-default restructurings, where collective action problems are most acute, the Fund could consider setting a clearer expectation (already allowed under existing policy) that non-negotiated offers by the debtor—following informal consultations with creditors—rather than negotiated deals, would be the norm, as in these cases speed is of the essence to avoid a default. These ideas could be explored in future staff work.And the second area, that is also “to be explored in future staff work”, is what to do about the risks caused by asymmetry in the treatment of private and official sector creditors, something that was very apparent in the recent Greek restructure:

… arrears to private and official creditors are currently treated asymmetrically under Fund policy.

Private external arrears are tolerated but arrears to official bilateral lenders are not. This subjects the Fund to the risk that it could not assist a member in need due to one or more holdout official bilateral creditors who seek favorable treatment of their claims.

Consideration could be given to extend the LIA policy to official bilateral arrears and in that context clarify the modality through which assurances of debt relief are provided by (non-Paris Club) official lenders. Another possibility would be for the Paris Club to extend its membership to all major lenders, so as to allow the Fund to rely on the Paris Club conventions with respect to financing assurances and arrears.

However, it is uncertain whether the Club could achieve such an expansion.All up it’s an interesting paper and well worth the read if you are interested in this type of thing. The paper also has some discussion on the European crisis-resolution mechanism ( discussed in more detail here ) , although given recent back-steps from Europe on the banking union this looks to still be something of a distant dream at this point.

It will be interesting to see if this paper has any effect on future programs, but it does appear, if only very slowly, that the IMF is learning from past mistakes and attempting to shift policy in a direction to address that issue. It would appear, at least from this paper, that the IMF will be demanding a more realistic assessment of the debt sustainability of target nations and a greater use of up-front restructuring as a per-requisite for program engagement. We’ll have to watch the next steps in Europe to determine if this is simply a talking point or something the IMF board will action.

Full paper below.

Source

May 24, 2013

Why the Stock Market Is Going Higher, According to Goldman

Goldman: Four Reasons Why the Market is Going Much Higher ... Last night's much-buzzed about research report from Goldman Sachs, in which the firm lays out its new S&P targets, contains an interesting rationale for higher stock prices. Rather than making the bull case based on earnings growth, Goldman believes that the 2% dividend yield on the S&P 500 will serve as a rising floor of sorts. This, along with an expanding PE multiple, augur well for US equities. – The Reformed Broker

Dominant Social Theme: Stocks are on a tear, despite the recent Nikkei setback.

Free-Market Analysis: Goldman Sachs has released a research report with four reasons why stocks are poised to go higher, as related in this short article posted over at The Reformed Broker.

The reasons reduce to some simple observations. First, the economy is getting better, meaning that good economic news will buoy stocks; second, stocks will continue to outperform bonds, which means stocks will attract a good flow of investment cash; third, companies will raise dividends, making stocks more attractive for those interested in an income stream; fourth, interest rates may remain low, benefiting stocks.

From our point of view, of course, it is simpler than that. Central bankers have decided that even the current rates of monetary debasement are not enough. They are determined to print even more money, thus swelling the prospects of equity even further.

In retrospect, the Japanese decisions to print money seems part of a larger promotion to make clear to a worldwide audience that economies are only being run one way these days, via Keynesian stimulation.

The BRICS, the EU and, of course, the US are all embarked on various forms of monetary stimulation and much of the talk in the financial press is about doing more of it rather than less.

Yesterday, Ben Bernanke gave congressional testimony warning against any significant diminution of "quantitative easing." At the same time, over in Europe, a senior Fed banker was purveying much the same message to the European Central Bank. Here's how the New York Times put it:

James Bullard, president of the Federal Reserve Bank of St. Louis and a voting member of the Fed's policy-setting open markets committee, said Europe's central bank should consider quantitative easing similar to that undertaken by the Fed — large bond purchases meant to drive down market interest rates.

The public comments were highly unusual. While central bankers from different countries frequently confer in private and offer advice and criticism to their peers behind closed doors, it is rare for any official to go public with even the mildest criticism of another central bank.

But with official interest rates in almost every advanced economy already close to zero, Mr. Bullard said, central bankers must reach for stronger tools to avoid getting trapped in economic doldrums.

This seems to us to have elements of a planned campaign. Japan's easing has received wide publicity of late and the ECB's determination to ease has proven both controversial and newsworthy.

Even Ben Bernanke's massive money printing schemes are attracting more attention than previously. Now, such a seemingly deliberate program will doubtless buy some more time for beleaguered central bankers. But the ultimate result is sure to be more ruined economies, countries and companies before this latest bout of trillion-dollar-plus stimulation has run its course.

In the meantime, as we've written, those with strong constitutions and an appetite for risk may wish to position themselves in various equity markets, counting on the strong central banking bias toward continued money printing.

Rightly or wrongly, what matters these days is monetary policy. The Goldman Sachs stock report, just released, is a kind of window dressing. For the most part, with some exceptions, the performance of a stock does not matter nearly so much as the commitment to a steady production of currency.

Conclusion: The Fed and central bankers generally are going out of their way to indicate that such an easing will continue. And despite recent market volatility, those who choose to ride the trend rather than oppose it may book at least short-term profits.

Source

Dominant Social Theme: Stocks are on a tear, despite the recent Nikkei setback.

Free-Market Analysis: Goldman Sachs has released a research report with four reasons why stocks are poised to go higher, as related in this short article posted over at The Reformed Broker.

The reasons reduce to some simple observations. First, the economy is getting better, meaning that good economic news will buoy stocks; second, stocks will continue to outperform bonds, which means stocks will attract a good flow of investment cash; third, companies will raise dividends, making stocks more attractive for those interested in an income stream; fourth, interest rates may remain low, benefiting stocks.

From our point of view, of course, it is simpler than that. Central bankers have decided that even the current rates of monetary debasement are not enough. They are determined to print even more money, thus swelling the prospects of equity even further.

In retrospect, the Japanese decisions to print money seems part of a larger promotion to make clear to a worldwide audience that economies are only being run one way these days, via Keynesian stimulation.

The BRICS, the EU and, of course, the US are all embarked on various forms of monetary stimulation and much of the talk in the financial press is about doing more of it rather than less.

Yesterday, Ben Bernanke gave congressional testimony warning against any significant diminution of "quantitative easing." At the same time, over in Europe, a senior Fed banker was purveying much the same message to the European Central Bank. Here's how the New York Times put it:

James Bullard, president of the Federal Reserve Bank of St. Louis and a voting member of the Fed's policy-setting open markets committee, said Europe's central bank should consider quantitative easing similar to that undertaken by the Fed — large bond purchases meant to drive down market interest rates.

The public comments were highly unusual. While central bankers from different countries frequently confer in private and offer advice and criticism to their peers behind closed doors, it is rare for any official to go public with even the mildest criticism of another central bank.

But with official interest rates in almost every advanced economy already close to zero, Mr. Bullard said, central bankers must reach for stronger tools to avoid getting trapped in economic doldrums.

This seems to us to have elements of a planned campaign. Japan's easing has received wide publicity of late and the ECB's determination to ease has proven both controversial and newsworthy.

Even Ben Bernanke's massive money printing schemes are attracting more attention than previously. Now, such a seemingly deliberate program will doubtless buy some more time for beleaguered central bankers. But the ultimate result is sure to be more ruined economies, countries and companies before this latest bout of trillion-dollar-plus stimulation has run its course.

In the meantime, as we've written, those with strong constitutions and an appetite for risk may wish to position themselves in various equity markets, counting on the strong central banking bias toward continued money printing.

Rightly or wrongly, what matters these days is monetary policy. The Goldman Sachs stock report, just released, is a kind of window dressing. For the most part, with some exceptions, the performance of a stock does not matter nearly so much as the commitment to a steady production of currency.

Conclusion: The Fed and central bankers generally are going out of their way to indicate that such an easing will continue. And despite recent market volatility, those who choose to ride the trend rather than oppose it may book at least short-term profits.

Source

May 23, 2013

Billion-Trillion Derivatives Market! ... Reform or a Blowup?

Derivatives Reform on the Ropes ... New rules to regulate derivatives, adopted last week by the Commodity Futures Trading Commission, are a victory for Wall Street and a setback for financial reform. They may also signal worse things to come ... The regulations, required under the Dodd-Frank reform law, are intended to impose transparency and competition on the notoriously opaque multitrillion-dollar market for derivatives, which is dominated by five banks: JPMorgan Chase, Goldman Sachs, Bank of America, Citigroup and Morgan Stanley. – New York Times

Dominant Social Theme: We have this billion trillion market under control. Don't worry.

Free-Market Analysis: Derivatives reform? We hardly think so ...

First of all, nobody knows how big the derivatives market is and no one knows how many dollars are at risk. Those involved in making the regulations are also the largest players in the market. Whatever "reform" is being worked out will benefit those who are part of the industry.

Here's how Wikipedia describes a derivative:

A derivative is a financial instrument which derives its value from the value of underlying entities such as an asset, index, or interest rate--it has no intrinsic value in itself. Derivative transactions include a variety of financial contracts, including structured debt obligations and deposits, swaps, futures, options, caps, floors, collars, forwards, and various combinations of these.

To give an idea of the size of the derivative market, The Economist magazine has reported that as of June 2011, the over-the-counter (OTC) derivatives market amounted to approximately $700 trillion, and the size of the market traded on exchanges totaled an additional $83 trillion. However, these are "notional" values, and some economists say that this value greatly exaggerates the market value and the true credit risk faced by the parties involved. For example, in 2010, while the aggregate of OTC derivatives exceeded $600 trillion, the value of the market was estimated much lower at $21 trillion. The credit risk equivalent of the derivative contracts was estimated at $3.3 trillion.

Still, even these scaled down figures represent huge amounts of money. For perspective, the budget for total expenditure of the United States Government during 2012 was $3.5 trillion, and the total current value of the US stock market is an estimated $23 trillion.

The world annual Gross Domestic Product is about $65 trillion. And for one type of derivative at least, Credit Default Swaps (CDS), for which the inherent risk is considered high, the higher, notional value, remains relevant. It was this type of derivative that investment magnate Warren Buffet referred to in his famous 2002 speech in which warned against "weapons of financial mass destruction." CDS notional value in early 2012 amounted to $25.5 trillion, down from $55 trillion in 2008.

Perhaps the most important part of this Wikipedia article (and admittedly Wikipedia is not definitive and often inaccurate) is this statement:

Proportion Used for Hedging and Speculation ... Unfortunately, the true proportion of derivatives contracts used for legitimate hedging purposes is unknown (and perhaps unknowable), but it appears to be relatively small. Also, derivatives contracts account for only 3–6% of the median firms' total currency and interest rate exposure. Nonetheless, we know that many firms' derivatives activities have at least some speculative component for a variety of reasons.

Not knowing how much of a billion trillion dollar market is unsecured and speculative would seem to be a problem. It is a problem because the derivatives market is not a normal market as the securities industry is abnormal, constrained by regulation and fattened by incredible amounts of fiat money.

Nothing like the modern money industry would exist without big government support and central bank monetary stimulation.

Because Wall Street and the City in particular are abnormal industry enterprises, the derivatives market itself is artificial and sooner or later apt to deflate unless one believes that trees can grow to the sky, eternally. But nothing goes up forever.

In the 1980s, portfolio insurance was supposed to insure that counterparty risk was a thing of the past. The Crash of 1987 put that incorrect assumption to rest and those who had depended on those instruments lost billions. There is no such thing as a "sure thing," and no regulatory oversight will adequately supervise or diminish the risk posed by a billion trillion dollar market. Even the New York Times recognizes this:

In the run-up to the financial crisis − and since − the lack of transparency and competition has fostered recklessness and instability. But banks like opacity, because their outsized profits depend on keeping clients in the dark about what other clients pay in similar deals. Under the Dodd-Frank law, derivatives are supposed to be traded on "swap execution facilities," which are to operate much like the exchanges that exist for equities and futures ...

The initial proposal ... called for derivatives trading to take place on open electronic platforms. The final rules will allow much of the negotiation over derivative prices to take place over the phone, a practice that is difficult to monitor and prone to abuse.

By themselves, these new rules are not fatal to the overall reform effort. And they are the best that the commission's reform-minded chairman, Gary Gensler, could achieve at this time because of resistance to tougher standards by the agency's two Republican commissioners and by one of its Democratic commissioners, Mark Wetjen.

The problem now is that Mr. Gensler's term has officially ended, and he is expected to leave the agency at the end of the year. Given Wall Street's incessant lobbying and powerful presence in Washington, it is assumed that he will be replaced by a chairman who is friendlier to Wall Street. That bodes ill for rules that have started out weak and need to be shored up later. To lose a reformer would also reflect poorly on President Obama, but he has not yet shown interest in keeping Mr. Gensler in the government.

This last paragraph refers to something called "regulatory capture." It is one reason why consumers should not count on regulation to protect them. Inevitably in modern governance those who are begin regulated end up in control of the regulations.

The CFTC is a notoriously weak regulator in any case and to further complicate matters US derivatives regulations are not being applied overseas. A lack of transparency, regulatory capture and a regime that ends at the water's edge means that the regs now being put in place for derivatives would seem to be virtually useless. In any event, regulations cannot stabilize a market in advance of a destabilizing event. They are price fixes that transfer risk and wealth from one place to another.

So what is the average investor to do? Given the amount of money pouring into stock markets, it is evident and obvious that averages will continue to move up in the long or short term. Eventually markets around the world will move back down – and no one actually knows when – but it is likely that time is not now.

For those who want to participate in the "only game in town," given that central banks control money printing, US stock markets in particular must present a tempting target. They will likely inflate further.

But those who want to expose some funds to stocks ought to keep in mind that what goes up can come down. Rigorous diversification is surely called for. Cash and precious metals ought to compete with any equity exposure. And it is possible that one ought to consider taking the initial investment out of the market over time, while leaving in the appreciation. This way the risk – and there is a billion trillion dollar risk to be concerned about – will be lessened.

Conclusion: Central banks are apparently determined to lift markets higher with money printing, at least in the short term. Those tempted to play the game – and it can be a profitable one – will remember the risks as the mainstream press is not apt to present many reminders.

Source

Dominant Social Theme: We have this billion trillion market under control. Don't worry.

Free-Market Analysis: Derivatives reform? We hardly think so ...

First of all, nobody knows how big the derivatives market is and no one knows how many dollars are at risk. Those involved in making the regulations are also the largest players in the market. Whatever "reform" is being worked out will benefit those who are part of the industry.

Here's how Wikipedia describes a derivative:

A derivative is a financial instrument which derives its value from the value of underlying entities such as an asset, index, or interest rate--it has no intrinsic value in itself. Derivative transactions include a variety of financial contracts, including structured debt obligations and deposits, swaps, futures, options, caps, floors, collars, forwards, and various combinations of these.

To give an idea of the size of the derivative market, The Economist magazine has reported that as of June 2011, the over-the-counter (OTC) derivatives market amounted to approximately $700 trillion, and the size of the market traded on exchanges totaled an additional $83 trillion. However, these are "notional" values, and some economists say that this value greatly exaggerates the market value and the true credit risk faced by the parties involved. For example, in 2010, while the aggregate of OTC derivatives exceeded $600 trillion, the value of the market was estimated much lower at $21 trillion. The credit risk equivalent of the derivative contracts was estimated at $3.3 trillion.

Still, even these scaled down figures represent huge amounts of money. For perspective, the budget for total expenditure of the United States Government during 2012 was $3.5 trillion, and the total current value of the US stock market is an estimated $23 trillion.

The world annual Gross Domestic Product is about $65 trillion. And for one type of derivative at least, Credit Default Swaps (CDS), for which the inherent risk is considered high, the higher, notional value, remains relevant. It was this type of derivative that investment magnate Warren Buffet referred to in his famous 2002 speech in which warned against "weapons of financial mass destruction." CDS notional value in early 2012 amounted to $25.5 trillion, down from $55 trillion in 2008.

Perhaps the most important part of this Wikipedia article (and admittedly Wikipedia is not definitive and often inaccurate) is this statement:

Proportion Used for Hedging and Speculation ... Unfortunately, the true proportion of derivatives contracts used for legitimate hedging purposes is unknown (and perhaps unknowable), but it appears to be relatively small. Also, derivatives contracts account for only 3–6% of the median firms' total currency and interest rate exposure. Nonetheless, we know that many firms' derivatives activities have at least some speculative component for a variety of reasons.

Not knowing how much of a billion trillion dollar market is unsecured and speculative would seem to be a problem. It is a problem because the derivatives market is not a normal market as the securities industry is abnormal, constrained by regulation and fattened by incredible amounts of fiat money.

Nothing like the modern money industry would exist without big government support and central bank monetary stimulation.

Because Wall Street and the City in particular are abnormal industry enterprises, the derivatives market itself is artificial and sooner or later apt to deflate unless one believes that trees can grow to the sky, eternally. But nothing goes up forever.

In the 1980s, portfolio insurance was supposed to insure that counterparty risk was a thing of the past. The Crash of 1987 put that incorrect assumption to rest and those who had depended on those instruments lost billions. There is no such thing as a "sure thing," and no regulatory oversight will adequately supervise or diminish the risk posed by a billion trillion dollar market. Even the New York Times recognizes this:

In the run-up to the financial crisis − and since − the lack of transparency and competition has fostered recklessness and instability. But banks like opacity, because their outsized profits depend on keeping clients in the dark about what other clients pay in similar deals. Under the Dodd-Frank law, derivatives are supposed to be traded on "swap execution facilities," which are to operate much like the exchanges that exist for equities and futures ...

The initial proposal ... called for derivatives trading to take place on open electronic platforms. The final rules will allow much of the negotiation over derivative prices to take place over the phone, a practice that is difficult to monitor and prone to abuse.

By themselves, these new rules are not fatal to the overall reform effort. And they are the best that the commission's reform-minded chairman, Gary Gensler, could achieve at this time because of resistance to tougher standards by the agency's two Republican commissioners and by one of its Democratic commissioners, Mark Wetjen.

The problem now is that Mr. Gensler's term has officially ended, and he is expected to leave the agency at the end of the year. Given Wall Street's incessant lobbying and powerful presence in Washington, it is assumed that he will be replaced by a chairman who is friendlier to Wall Street. That bodes ill for rules that have started out weak and need to be shored up later. To lose a reformer would also reflect poorly on President Obama, but he has not yet shown interest in keeping Mr. Gensler in the government.

This last paragraph refers to something called "regulatory capture." It is one reason why consumers should not count on regulation to protect them. Inevitably in modern governance those who are begin regulated end up in control of the regulations.

The CFTC is a notoriously weak regulator in any case and to further complicate matters US derivatives regulations are not being applied overseas. A lack of transparency, regulatory capture and a regime that ends at the water's edge means that the regs now being put in place for derivatives would seem to be virtually useless. In any event, regulations cannot stabilize a market in advance of a destabilizing event. They are price fixes that transfer risk and wealth from one place to another.

So what is the average investor to do? Given the amount of money pouring into stock markets, it is evident and obvious that averages will continue to move up in the long or short term. Eventually markets around the world will move back down – and no one actually knows when – but it is likely that time is not now.

For those who want to participate in the "only game in town," given that central banks control money printing, US stock markets in particular must present a tempting target. They will likely inflate further.

But those who want to expose some funds to stocks ought to keep in mind that what goes up can come down. Rigorous diversification is surely called for. Cash and precious metals ought to compete with any equity exposure. And it is possible that one ought to consider taking the initial investment out of the market over time, while leaving in the appreciation. This way the risk – and there is a billion trillion dollar risk to be concerned about – will be lessened.

Conclusion: Central banks are apparently determined to lift markets higher with money printing, at least in the short term. Those tempted to play the game – and it can be a profitable one – will remember the risks as the mainstream press is not apt to present many reminders.

Source

May 22, 2013

Banks Win Big as Regulators Refuse to Rein in $700 Trillion Derivatives Market

Here are Black’s policy recommendations:

JAY: Okay. So you can’t get even measly regulation through. You can’t tame the scorpion. And the scorpion ain’t changing its nature. I guess most people know this little story by now. So you’re talking about let’s get rid of the scorpions. What does that mean?

BLACK: Yeah. So my thing is we’ve got to do three things. And the good news is economically it would make a better economy. The first of the three things is stop the entities that are systemically dangerous from growing. And many of them are growing very substantially.

The second thing is to order them to shrink over the next five years below $50 billion in assets, a point where they’ll no longer pose a systemic risk. And let them figure out how they’re going to do that.

And the third thing that we need to do–admittedly it assumes to some extent the answer–is to have hyperintensive regulation during that time period. Now, I do recognize that I just told you a story about how the Commodity Futures Trading Commission couldn’t even get fairly weak regulation, but that’s why I’m saying where our effort should be as progressives during that period is to be hypervigilant about the regulation.

JAY: So to get to what you’re talking about means a political transformation of the country, ’cause right now the scorpions control the politics.

BLACK: And that’s really my point is that the systemically dangerous institutions, first, they are so large that they are horribly inefficient and risky.

Second, they have this massive implicit federal subsidy that means that any of these, you know, odes you hear to free markets are completely fictional. And conservative scholars agree that there’s absolutely nothing free about the financial markets.

Then you have the fact that they do create these periodic crises that are getting worse. We simply cannot afford to have the next crisis.

And the final thing is the point you were raising. It is impossible to have a real democracy with these kind of systemically dangerous institutions. What you have instead is crony capitalism, and crony capitalism is the death of democracy.

OK. But how?

Source

May 21, 2013

The Coming Collapse Of The Petrodollar System

PETRODOLLAR

WAR

The theory of Petrodollar Warfare can be attributed to US analyst and author William R Clarke, and his 2005 book of that title which interpreted the US-UK decision to invade Iraq in 2003. He called this an "oil currency war", but the concept of the petrodollar system and petrodollar recyling dates back to the eve of the first Oil Shock in 1973-1974. The role of the petrodollar system as a driving force of US foreign policy is explained by analysts and historians as basic to maintaining the dollar's status as the world's dominant reserve currency - and the currency in which oil is priced.

The term "petrodollar warfare" as used by William R. Clark says that major international war, legal or not, was seen as justified to protect the petrodollar system. Over and above the loss of human life, the combined costs of the Afghan and Iraq wars for the US are controversial like the interpretation of these wars as "oil wars", but analysts like Joseph Stiglitz and Linda Bilmes put the total combined war cost at above $4 trillion. This can be compared with - and totally dwarfs - the annual cost of US oil imports, which are now sharply declining on a year-in year-out basis as domestic shale oil output ramps up, and US oil demand stagnates.

Clarke's theory, like the explanation of the role and power of the "petrodollar system" depends on two basic drivers. Most major developed countries rely on oil imports, which are purchased using dollars, so they are forced to hold large stockpiles of dollars in order to continue importing oil. In turn this also creates consistent demand for dollars, and prevents the dollar from losing its relative international monetary value, regardless of what happens to the US economy.

Variants of the Petrodollar War concept include the role of oil currency

conflicts and rivalry, notably concerning US relations with Iran, Venezuela and

Russia, and possibly with Europe concerning the gradual replacement of

US dollars with the euro, for oil transactions. More important, the

entire petromoney system and the potential for Petrodollar War hinges on global

oil import demand and the oil price. Both of these have to hold up. When or if

they do not, foreign oil importer nations who formerly found it beneficial to

hold dollars to pay for oil, would have to find some other (unexplained) reason

for huge holdings of dollars, when their oil imports decline and-or oil prices

also decline.

Variants of the Petrodollar War concept include the role of oil currency

conflicts and rivalry, notably concerning US relations with Iran, Venezuela and

Russia, and possibly with Europe concerning the gradual replacement of

US dollars with the euro, for oil transactions. More important, the

entire petromoney system and the potential for Petrodollar War hinges on global

oil import demand and the oil price. Both of these have to hold up. When or if

they do not, foreign oil importer nations who formerly found it beneficial to

hold dollars to pay for oil, would have to find some other (unexplained) reason

for huge holdings of dollars, when their oil imports decline and-or oil prices

also decline.

The "currency war" variant of the petrodollar system theory, holding that a shift to notably euros or gold for oil payments would undermine the system, is unrealistic when given any serious analysis, because all world moneys are interchangeable or convertible, and gold is priced in US dollars.

THE THREE PHASES OF THE SYSTEM

These are easy to define.

1974-1986 The first phase. The 1972 start of "petrodollar recycling" initiated by Nixon and Kissinger just before the fivefold rise in oil prices of 1973-74, set the process of US-Saudi Arabian cooperation for the near-exclusive benefit of these two players. The US dollar was "backstopped" by the transfer of Saudi liquidities to the US Federal Reserve system banks, especially the Federal Reserve Bank of New York. A small number of other chosen central banks, especially the Bank of England, and the central banks of Germany, France, Italy and Japan also benefitted.