The story of energy and the economy seems

to be an obvious common sense one: some sources of energy are becoming scarce or

overly polluting, so we need to develop new ones. The new ones may be more

expensive, but the world will adapt. Prices will rise and people will learn to

do more with less. Everything will work out in the end. It is only a matter of

time and a little faith. In fact, the Financial Times published an article

recently called “

Looking Past the Death of Peak Oil” that

pretty much followed this line of reasoning.

Energy Common Sense Doesn’t Work Because the World is

Finite

The main reason such common sense doesn’t

work is because in a finite world, every

action we take has many direct and indirect effects. This chain of effects

produces connectedness that makes the economy operate as a network. This network

behaves differently than most of us would expect. This networked behavior is not

reflected in current economic models.

Most people believe that the amount of oil in the ground is the

limiting factor for oil extraction. In a finite world, this isn’t true. In a

finite world, the limiting factor is feedback loops that lead to inadequate

wages, inadequate debt growth, inadequate tax revenue, and ultimately inadequate

funds for investment in oil extraction. The behavior of networks may lead to

economic collapses of oil exporters, and even to a collapse of the overall

economic system.

An issue that is often overlooked in the

standard view of oil limits is diminishing returns. With diminishing returns,

the cost of extraction eventually rises because the easy-to-obtain resources are

extracted first. For a time, the rising cost of extraction can be hidden by

advances in technology and increased mechanization, but at some point, the

inflation-adjusted cost of oil production starts to rise.

With diminishing returns, the economy is,

in effect, becoming less and less efficient, instead of becoming more and more

efficient. As this effect feeds through the system, wages tend to fall and the

economy tends to shrink rather than grow. Because of the way a networked system

“works,” this shrinkage tends to collapse the economy. The usage of energy

products of all kinds is likely to fall, more or less simultaneously.

In some ways current, economic models are

the equivalent of flat maps, when we live in s spherical world. These models

work pretty well for a while, but eventually, their predictions deviate farther

and farther from reality. The reason our models of the future are wrong is

because we are not imagining the system correctly.

The Connectedness of a Finite World

In a finite world, an action a person

takes has wide-ranging impacts. The amount of food I eat, or the amount of

minerals I extract from the earth, affects what other people (now and in the

future) can do, and what other species can do.

To illustrate, let’s look at an

exaggerated example. At any given time, there is only so much broccoli that is

ready for harvest. If I decide to corner the broccoli market and buy up 50% of

the world’s broccoli supply, that means that other people will have less

broccoli available to buy. If those growing the broccoli spray the growing crop

with pesticides, “broccoli pests” (caterpillars, aphids, and other insects) will

die back in number, perhaps contributing to a decline of those species. The

pesticides may also affect desirable species, like bees.

Growing the broccoli will also deplete

the soil of nutrients. If 50% of the world’s broccoli is shipped to me, the

nutrients from the soil will find their way around the world to me. These

nutrients are not likely to be replaced in the soil where the broccoli was grown

without long-distance transport of nutrients.

To take another example, if I (or the

imaginary company I own) extract oil from the ground, the extraction and the

selling of that oil will have many far-ranging effects:

- The oil I extract will most likely be

the cheapest, easiest-to-extract oil that I can find. Because of this, the oil

that is left will tend to be more expensive to extract. My extraction of oil

thus contributes to diminishing returns–that is, the tendency of the

cost of oil extraction to rise over time as resources deplete.

- The petroleum I extract from the ground

will consist of a mixture of hydrocarbon chains of varying lengths. When I send

the petroleum to a refinery, the refinery will separate the petroleum into

varying length chains: short chains are gasses, longer chains are liquids, still

longer ones are very viscous, and the longest ones are solids, such as asphalt.

Different length chains are used for different purposes. The shortest chains are

natural gas. Some chains are sold as gasoline, some as diesel, and some as

lubricants. Some parts of the petroleum spectrum are used to make plastics,

medicines, fabrics, and pesticides. All of these uses will help create jobs in a

wide range of industries. Indirectly, these uses are likely to enable higher

food production, and thus higher population.

- When I extract the oil from the ground,

the process itself will use some oil and natural gas. Refining the oil will also

use energy.

- Jobs will be created in the oil

industry. People with these jobs will spend their money on goods and services of

all sorts, indirectly leading to greater availability of jobs outside the oil

industry.

- Oil’s price is important. The lower the

price, the more affordable products using oil will be, such as cars.

- In order for consumers to purchase cars

that will operate using gasoline, there will likely be a need for debt to buy

the cars. Thus, the extraction of oil is tightly tied to the build-up of

debt.

- As an oil producer, I will pay taxes of

many different types to all levels of governments. (Governments of oil exporting

countries tend to get a high percentage of their revenue from taxes on oil. Even

in non-exporting countries, taxes on oil tend to be high.) Consumers will also

pay taxes, such as gasoline taxes.

- The jobs that are created through the

use of oil will lead to more tax revenue, because wage earners pay income

taxes.

- The government will need to build more

roads, partly for the additional cars that operate on the roads thanks to the

use of gasoline and diesel, and partly to repair the damage that is done as

trucks travel to oil extraction sites.

- To keep the oil extraction process

going, there will likely need to be schools and medical facilities to take care

of the workers and their families, and to educate those workers.

Needless to say, there are other effects

as well. The existence of my oil in the marketplace will somehow affect the

market price of oil. Burning of the oil may affect the climate, and will tend to

acidify oceans. It would be possible to go on and on.

The Difficulty of Substituting Away from

Oil

In some sense, the use of oil is very

deeply imbedded into the operation of the overall economy. We can talk about

electricity replacing oil, but oil’s involvement in the economy is so pervasive,

it can’t possibly replace everything. Perhaps electricity might replace gasoline

in private passenger automobiles. Such a change would reduce the demand for

hydrocarbon chains of a certain length (C7 to C11), but that only reduces demand for one

“slice” of the oil mixture. Both shorter and longer chain hydrocarbons would be

unaffected.

The price of gasoline will drop, (making

Chinese buyers happy because more will be able to afford to use motorcycles),

but what else will happen? Won’t we still need as much diesel, and as many

medicines as before? Refiners can fairly easily break longer-chain molecules

into shorter-chain molecules, so they can make diesel or asphalt into gasoline.

But going the other direction doesn’t work well at all. Making gasoline into

shorter chains would be a huge waste, because gasoline is much more valuable

than the resulting gases.

How about replacing all of the taxes

directly and indirectly related to the unused gasoline? Will the price of

electricity used in electric-powered vehicles be adjusted to cover the foregone

tax revenue?

If a liquid substitute for oil is made,

it needs to be low priced, because a high-priced substitute for oil is very

different from a low-priced substitute. Part of the problem is that high-priced

substitutes do not leave enough “room” for taxes for governments. Another part

of the problem is that customers cannot afford high-priced oil products. They

cut back on discretionary expenditures, and the economy tends to contract. There

are layoffs in the discretionary sectors, and (again) the government finds it

difficult to collect enough tax revenue.

The Economy as a Networked System

I think of the world economic system as

being a networked system, something like the dome shown in Figure 1. The dome

behaves as an object that is different from the many wooden sticks from which it

is made. The dome can collapse if sticks are removed.

The world economy consists of a network

of businesses, consumers, governments, and resources that is bound together with

a financial system. It is self-organizing, in the sense that consumers decide

what to buy based on what products are available at what prices. New businesses

are formed based on the overall environment: potential customers, competition,

resource availability, services available from other businesses, and laws.

Governments participate in the system as well, building infrastructure, making

laws, and charging taxes.

Over time, all of these gradually change.

If one business changes, other business and consumers are likely to make changes

in response. Even governments may change: make new laws, or build new

infrastructure. Over time, the tendency is to build a larger and more complex

network. Unused portions of the network tend to wither away–for example, few

businesses make buggy whips today. This is why the network is illustrated as

hollow. This feature makes it difficult for the network to “go backward.”

The network got its start as a way to

deliver food energy to people. Gradually economies expanded to include other

goods and services. Because energy is required to “do work,” (such as provide

heat, mechanical energy, or electricity), energy is always central to an

economy. In fact, the economy might be considered an energy delivery system.

This is especially the case if we consider wages to be payment for an important

type of energy–human energy.

Because of the way the network has grown

over time, there is considerable interdependency among different types of

energy. For example, electricity powers oil pipelines and gasoline pumps. Oil is

used to maintain the electric grid. Nuclear electric plants depend on

electricity from the grid to restart their operations after outages. Thus, if

one type of energy “has a problem,” this problem is likely to spread to other

types of energy. This is the opposite of the common belief that energy

substitution will fix all problems.

Economies are Prone to Collapse

We know the wooden dome in Figure 1 can

collapse if “things go wrong.” History shows that many civilizations have

collapsed in the past. Research has been done to see why this is the case.

Joseph Tainter’s research indicates that

diminishing returns played an important role in the collapse of past

civilizations. Diminishing returns would be a problem when adding more workers

didn’t add a corresponding amount more output, particularly with respect to

food. Such a situation might be reached when population grew too large for a

piece of arable land. Degradation of soil fertility might play a role as

well.

Today, we are reaching diminishing

returns with respect to oil supply, as evidenced by the rising cost of oil

extraction. This is occurring because we removed the easy to extract oil, and

now must move on to the more expensive to extract oil. In effect, the system is

becoming less efficient. More workers and more resources of other types are

needed to produce a given barrel of oil. The value of the barrel of oil in terms

of what it can do as work (say, how far it can move a car, or how much heat it

can produce) is unchanged, so the value each worker is producing is less. This

is the opposite of efficiency.

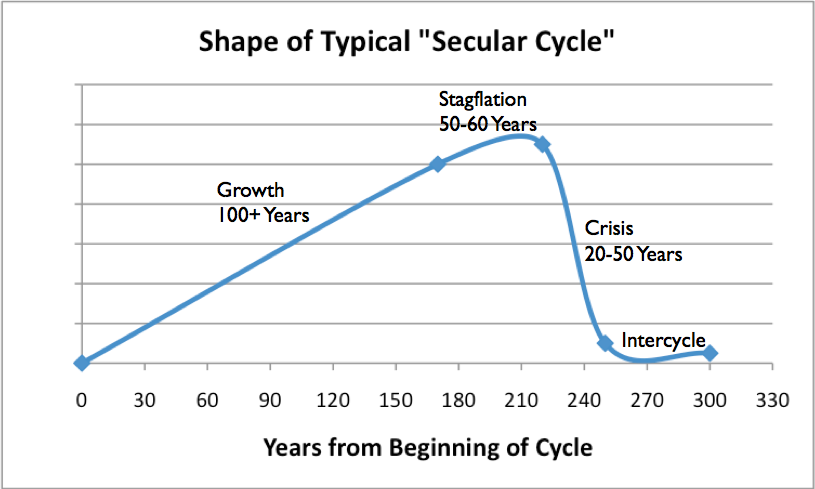

Peter Turchin and Sergey Nefedov have

done research on the nature of past collapses, documented in a book called

Secular Cycles. An economy would clear a

piece of land, or discover an approach to irrigation, or by some other means

discover a way to expand the number of people who could live in an area. The

resulting economy would grow for well over 100 years, until population started

catching up with resource availability. A period of stagflation followed,

typically for about 50 or 60 years, as the economy tried to continue to grow,

but bumped against increasing obstacles. Wage disparity grew as wages of new

workers lagged. Debt also grew.

Eventually collapse occurred, over a

period of 20 to 50 years. Often, much of the population died off. An inter-cycle

period followed, during which resources regenerated, so that a new civilization

could arise.

Figure 2. Shape of

typical Secular Cycle, based on work of Peter Turkin and Sergey Nefedov in

Secular Cycles.

One of the major issues in past collapses

was difficulty in funding government services. Part of the problem was that

wages of common workers were low, making it difficult to collect enough taxes.

Part of governments’ problems were that their costs went up, as they tried to

solve the increasingly complex problems of society. Today these costs might

include unemployment insurance and bailing out banks; in ages past they included

larger armies to try to conquer new lands with more resources, as their own

resources depleted.

Today’s Situation

Our situation isn’t too different. The

economy started growing in the early 1800s, abut the we started using fossil

fuels, thanks to technology that allowed us to use them. Oil is the fossil

fuel that is depleting most quickly, because it is very valuable in many uses,

including transportation, agriculture, construction, mining, and as a raw

material to produce many goods we use every day.

Our economy seems to have hit stagflation

in the early 1970s, when oil prices first began to spike. Now, some of the

symptoms we are seeing are looking distressingly like the symptoms that other

civilizations saw prior to the beginning of collapse. Our networked system has

many weak points:

- Oil exporters Governments can collapse, as

the government of the Former Soviet Union did in 1991, if oil prices are too

low. The fact that oil prices have not risen since 2011 is probably contributing

to unrest in the Middle East.

- Oil importers Spikes in oil prices lead to

recession.

- Governments funding Debt keeps expanding;

infrastructure needs fixes but they don’t get done; too many promises for

pensions and healthcare.

- Failing financial systems Debt defaults are

likely to be a major problem if the economic system starts shrinking. Debt is needed to keep oil prices

up.

- Contagion if one energy product is in short

supply This happens many ways. For example, nearly all businesses rely

on both electricity and oil. If either one of these becomes unavailable (say oil

to supply parts and ship goods to customers), then the business will need to

close. Because of the business closure, demand for other energy products the

business uses, such as electricity and natural gas, will drop at the same time.

Direct use of energy products to produce other energy products (mentioned

previously) also contributes to this contagion.

Unfortunately, when it comes to operating

an economy, it is

Liebig’s Law of the Minimum that rules. In other

words, if any required element is missing, the system doesn’t work. If

businesses can’t get financing, or can’t pay their employees because banks are

closed, businesses may need to close. Workers will get laid off, and the

inability to afford energy

products (economists would call this “lack of demand”) will be what brings

the system down.

Modeling our Current Economy

Everywhere we look, we see models of how

the energy system or the economy can be expected to work. None of the models

match our current situation well.

Growth will Continue As in the Past It is

pretty clear that this model is inadequate. Every

revision to growth estimates seems to be

downward. In a finite world, we know that growth at the same rate can’t

continue forever–we would run out of resources, and places for people to stand.

The networked nature of the system explains how the system really grows, and why

this growth can’t continue indefinitely.

Rising Cost of Producing Energy Products Doesn’t

Matter In a global world, we compete on the price of goods and services. The cost of

producing these goods and services depends on (a) the cost of energy products

used in making these goods and services (b) wages paid to workers for producing

these services (c) government, healthcare, and other overhead costs, and (d)

financing costs.

One part of our problem is that with

globalization, we are competing against warm countries–countries that receive

more free energy from the sun than we do, so are warmer than the US and Europe.

Because of this free energy from the sun, homes do not need to be built as

sturdily and less heat is needed in winter. Without these costs, wages do not

need to be as high. These countries also tend to have less expensive healthcare

systems and lower pensions for the elderly.

Governments can try to fix our

non-competitive cost structure compared to these countries by reducing interest

rates as much as possible, but the fact remains–it is very difficult for

countries in cold parts of the world to compete with countries in warm parts of

the world in making goods. This cost competition problem becomes worse, as the

price of energy products rises because we are competing with a cost of $0 for

heating requirements. If cold countries add carbon taxes, but do not surcharge

goods imported from warm countries, the disparity with warm countries becomes

even worse.

In the early years of civilization, warm

countries dominated the world economy. As energy prices rise, this situation is

likely to again occur.

Price is Not Important Apart from the warm

country–cool country issue, there is another reason that energy cost (in real

goods, not just in financial printed money) is important:

The price of the energy used in the

economy is important because it is tied to how much must be “given up” to buy

the oil or anther energy product (such as food). If energy is cheap, little

needs to be given up to obtain the energy. Because of energy’s huge ability to

do “work,” the work that is obtained can easily make goods and services that

compensate for what has been given up. If energy is expensive, there is much

less benefit (or perhaps negative benefit) when what is given up is compared to

the work that the energy product provides. As a result, economic growth is held

back by high-priced energy products of any kind.

Supply and Demand Leads to Higher Prices and

Substitutes Major obstacles to the standard model working are (a)

diminishing returns with respect to oil supply, (b) recession and even

government failure of oil importers, when oil prices rise and (c) civil unrest

and even government failure in oil exporters, if oil prices don’t keep

rising. If there isn’t enough oil supply, oil prices rise, but there are soon so

many follow-on effects that oil prices fall back again.

Reserves/ Production This ratio supposedly

tells how long we can produce oil (or natural gas or coal) at current extraction

rates. This ratio is simply misleading. The real limit is how long the economy

can function, given the feedback loops related to diminishing returns. If a

person simply looks at investment dollars required, it becomes clear that this

model doesn’t work. See my post

IEA Investment Report – What is Right; What

is Wrong.

Energy Payback Period, Energy Return on Energy

Invested, and Life Cycle Analysis These approaches look at the

efficiency of energy production, comparing energy used in the process to energy

produced in the process. In some ways, they work–they show that we are becoming

less and less efficient at producing oil, or coal, or natural gas, as we move to

more difficult to extract resources. And they can be worthwhile, if a decision

is being made as to which of two similar devices to purchase: Wind Turbine A or

Wind Turbine B.

Unfortunately, modeling a finite world is

virtually impossible. These approaches use narrow boundaries–energy used in

pulling oil out of the ground, or making a wind turbine. It doesn’t tell as much

as we need to know about new energy generation equipment, together with (a)

changes needed elsewhere in the system and (b) whatever financial system is used

to pay for the energy generated with that system, will actually work in the

economy. To really analyze the situation, broader analyses are needed.

Furthermore, there are the inherent

assumptions that (a) we have a long time period to make changes and (b) one

energy source can be substituted for another. Neither of these assumptions is

really true when we are this close to oil limits.

Where the Peak Oil Model Went Wrong

Part of the Peak Oil story is right: We

are reaching oil limits, and those limits are hitting about now. Part of the

Peak Oil story is not right, though, at least in a common version that is

prevalent now. The version that is prevalent is more or less equivalent to the

“standard” view of our current situation that I talked about at the beginning of

the post. In this standard view, oil supply will not disappear very

quickly–approximately 50% of the total amount of oil ever extracted will become

available after the peak in oil production. There will be considerable

substitution with other fuels, often at higher prices. The financial system may

be affected, but it can be replaced, and the economy will continue.

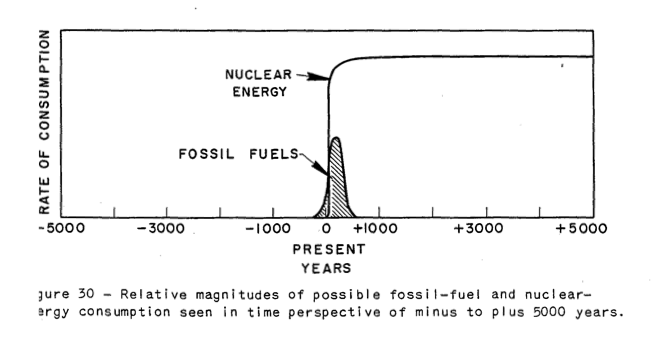

This view is based on writing of M. King

Hubbert

back in 1957. At that time, it was commonly

believed that nuclear energy would provide electricity

too cheap to meter. In fact, in a

1962 paper, Hubbert talks about “reversing

combustion,” to make liquid fuels. Thus, not only did his story include cheap

electricity, it also included cheap liquid fuels, both in huge quantity.

In such a situation, growth could

continue indefinitely. There would be no need to replace huge numbers of

vehicles with electric vehicles. Governments wouldn’t have a problem with

funding. There would be no problem with collapse. The supply of oil and other

fossil fuels could decline slowly, as suggested in his papers.

But the story of the cheap, rapid nuclear

ramp-up didn’t materialize, and we gradually got closer to the time when limits

were beginning to hit. Major changes were needed to Hubbert’s story to reflect

the fact that we really didn’t have a fix that would keep business as usual

going indefinitely. But these changes never took place. Instead the view of how

little change was needed to keep the economy going kept getting downgraded more

and more. “Standard” economic views filtered into the story, too.

There is a correct version of the oil limits story to

tell. It is the story of the failure of networked systems.