So why does the government maintain such a transparently

inaccurate and misleading metric? For three reasons.

That the official rate of inflation doesn't reflect reality is obvious

to anyone paying college tuition and healthcare out of pocket. The debate

over the accuracy of the official consumer price index (CPI) and personal

consumption expenditures (PCE--the so-called core rate of inflation) has raged

for years, with no resolution in sight.

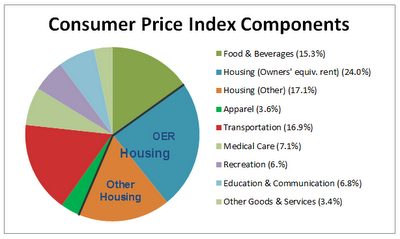

The CPI

calculates inflation based on the prices of a basket of goods and services that

are adjusted by hedonics, i.e. improvements that are not reflected in the price

of the goods. Housing costs are largely calculated on equivalent rent, i.e. what

homeowners reckon they would pay if they were renting their house.

The CPI

attempts to measure the relative weight of each component:

Many argue

that these weightings skew the CPI lower, as do hedonic adjustments. The

motivation for this skew is transparent: since the government increases Social

Security benefits and Federal employees' pay annually to keep up with inflation

(the cost of living allowance or COLA), a low rate of inflation keeps these

increases modest.

Over time,

an artificially low CPI/COLA lowers government expenditures (and deficits,

provided tax revenues rise at rates above official inflation).

Those

claiming the weighting is accurate face a blizzard of legitimate questions. For

example, if healthcare is 18% of the U.S. GDP, i.e. 18 cents of every dollar

goes to healthcare, then how can a mere 7% wedge of the CPI devoted to

healthcare be remotely accurate?

In my analysis, the debate over inflation is intrinsically

flawed. What really matters is not the overall rate of inflation, which can

be endlessly debated, but the purchasing power of earned income,

i.e. wages and the exposure to real-world costs.

In other

words, those households with zero exposure to college tuition and the full costs

of daycare, medical care and healthcare insurance may well experience low

inflation, while the household paying the full costs of daycare, college tuition

and healthcare insurance will experience soaring inflation.

Here's one example of how CPI fails to capture real-world

inflation/loss of purchasing power. Let's say an employee works for a

company or agency that pays his/her healthcare insurance. The monthly cost has

risen from $1,000/month to $1,500/month. The employee's wage has remained

stagnant but the total compensation costs paid by the employer

have gone up by $500/month.

Now the employer shifts that $500/month to the employee as their

share of the healthcare insurance cost. Since the average full-time worker earns

around $40,000 a year, and pays around 18% in taxes, their take-home pay is

around $33,000 annually.

The employee's co-pay of $6,000 a year ($500/month) represents 18% of

their take-home wage. This is an 18% reduction in earnings, or the

equivalent of 18% inflation (i.e. a reduction in purchasing power).

This

shifting of the skyrocketing burden of healthcare costs acts the same as 20%

inflation, yet it doesn't even register in the current CPI.

The geography of inflation doesn't register, either. Soaring rents

in Brooklyn, NY and the San Francisco Bay Area have a profound effect on those

exposed to these rapidly rising costs, yet these impacts are massaged to zero by

national CPI calculations.

So once again we have a bifurcated society: those protected by the

state from rising costs and those exposed to real-world reductions in purchasing

power.Households that receive government subsidies and direct payments have

little exposure to real-world healthcare costs, since they are covered by

Medicaid, and modest exposure to housing if they receive Section 8 benefits

(Section 8 recipients pay 30% of their income for rent, regardless of the market

price of the rental). Retirees on Medicare also have limited exposure to the

real-world costs of their care paid by the government.

If we analyze inflation by these two metrics, we find the middle class

is increasingly exposed to skyrocketing real-world prices. Pundits in the

top 5% have the luxury of pontificating on the accuracy of the CPI while those

protected by government subsidies and coverage have the luxury of wondering what

all the fuss is about. Only those 100% exposed to the real costs experience the

full fury of actual inflation.

So why does the government maintain such a transparently inaccurate

and misleading metric? For three reasons: 1) it is useful propaganda; 2) it

suppresses the state's cost-of-living increases and 3) it lowers the

government's cost of borrowing. The benefits of reducing COLA adjustments

are self-evident, as is the benefit of borrowing money at low rates of interest,

but the propaganda benefits are more subtle.

The key to enabling the endless printing of money that enriches the

banks and the top .1% is low inflation. Asset bubbles can be inflated,

ballooning the wealth of the owners of the assets, as long as inflation is

near-zero.

Indeed,

the Federal Reserve claims it must print money to counter low

inflation.

Meanwhile, in the real economy, those exposed to the real costs of college tuition, healthcare, childcare, etc. are seeing their purchasing power evaporate like a puddle of water in Death Valley. The Fed needs low inflation to justify its continuing enrichment of the financial elite, and the Federal government needs low inflation to keep its COLAs and borrowing costs low.

There are

two ways to mask real-world reductions of purchasing power: 1) skew the CPI by

distorting the component percentages, hedonics and how costs are measured, and

2) protect enough of the populace from real-world increases so they no longer

care. Seniors, who famously vote in droves, have no idea what their Medicare

benefits actually cost. As a result, they have no experience of healthcare

inflation /reduction of purchasing power.

This works

in all sorts of industries. As I have often mentioned here, the F-35 Lightning

fighter aircraft costs in excess of $200 million each, roughly four times the

cost of the F-18F it replaces. This extraordinary inflation is not experienced

directly by the taxpayer who is paying for the boondoggle, as the Federal

government borrows trillions of dollars to pay for such boondoggles, effectively

passing the inflated costs on to future generations.

These costs are hidden by the low cost of borrowing trillions to pay

for boondoggles. If real-world inflation is (say) 5%, then interest rates

would typically adjust to a few points above that rate, to compensate capital

for the erosion of purchasing power. If the Treasury had to pay 7% to borrow

money, the interest cost would soon cripple Federal spending. People would be

forced to focus on how all those trillions of dollars are being spent, and to

whose benefit.

But with

borrowing costs so low, nobody cares.

The solution? One, abolish the Fed and let the market discover

interest rates, and two, abandon the simplistic notion that one number of

inflation has any meaning in a complex economy with numerous subsets of

exposure to market costs and the loss or gain of purchasing power.

Will we

muster the will to look past failed models and metrics? Sadly, the answer is no.

Why?

As I noted

yesterday in What's the Difference Between Fascism, Communism and

Crony-Capitalism? Nothing, a system set up to enrich political

and financial elites is incapable of reform. the only way the CPI will ever

be replaced is when the Status Quo collapses in a heap of lies and insolvency.

Until then, propaganda and gaming the system to protect vested interests will

rule.

No comments:

Post a Comment