values, with the need to do post crisis damage control as the cover. For instance, after the initial round of QE, Brazil and India complained vociferously about the dual impact of a weaker dollar and higher commodity prices (yes, Virginia, some economists do think financial speculation can influence commodity prices) on their economies. If Europe contracts while growth in the US and China are also decelerating, it isn’t hard to imagine that the currency front will heat up even more.

values, with the need to do post crisis damage control as the cover. For instance, after the initial round of QE, Brazil and India complained vociferously about the dual impact of a weaker dollar and higher commodity prices (yes, Virginia, some economists do think financial speculation can influence commodity prices) on their economies. If Europe contracts while growth in the US and China are also decelerating, it isn’t hard to imagine that the currency front will heat up even more.This piece by Daniel Gros illustrates, surprisingly, that one currency manipulator has managed to operate under the radar so far. It will be interesting to see if his analysis gets traction in Europe

.By Daniel Gros Director of the Centre for European Policy Studies, Brussels. Cross posted from VoxEU

Switzerland has pegged its currency to the euro at a level that helps it sustain a 12% current-account surplus and one of the lowest unemployment rates in Europe. This column argues that the Swiss peg involves currency manipulation that is, as far as Europe is concerned, the same order of magnitude as China’s intervention. It has had a significant impact on the euro exchange rate and a non-negligible effect on the EZ economy.

A current-account surplus is the mirror image of a capital export. A country that is running persistent current-account surpluses is thus persistently exporting capital. An important question to consider is which sector is investing abroad, the private or the public sector? If it is the public sector which invests abroad, in particular if it is done by the central bank via the accumulation of foreign-exchange reserves, this is often called ‘currency manipulation’.

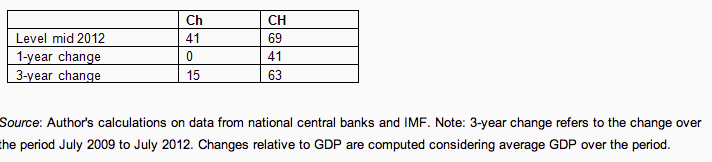

A commonly used indicator of the degree to which a country manipulates its currency is the accumulated stock of foreign-exchange reserves relative to GDP.

The table below shows the degree of foreign exchange intervention for two countries, which we will call “CH” and “Ch”.

The degree of influence on the domestic currency can be measured in two ways:

• The stock of foreign-exchange reserves as over GDP, or;Table 1 shows that on all measures CH emerges as the greater ‘manipulator’ than Ch. At the middle of 2012 the value of the foreign-exchange reserves (largely held in euro) of CH amounted to close to 70% of GDP; almost twice as much as the roughly 40% of GDP for Ch. Over the last 12 months Ch has actually stopped intervening, but this might be due to transitional factors. The three year perspective might thus be more appropriate. But even over this longer period, one finds that CH manipulates more than Ch.

• The change in foreign-exchange reserves accumulated over the recent past, again relative to GDP.

Table 1. Foreign-exchange reserves, stocks and flows, as % GDP

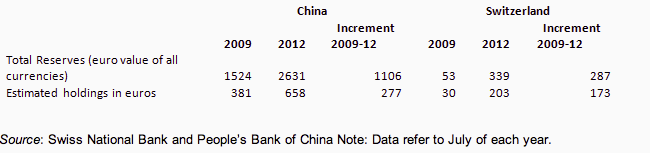

In reality Ch(ina) is a much larger country and the total amount of its interventions are much larger than CH (Confoederatio Helvetica). China has accumulated over €2630 billion ($3 trillion) worth of reserves, about seven times more (‘only’ seven times given the difference in the size of the economy, which is almost 12 to 1) than the about €340 billion ($400 billion) of Switzerland. But this latter amount is not insignificant at the scale of Europe. Moreover most of China’s foreign-exchange reserves are invested in dollars, whereas Switzerland has invested mainly in euros.

In the absence of data disclosure, one can only guess the currency composition of China’s reserves. According to various estimates, about 20-25% of China’s total foreign reserves are held in euro-denominated assets. This implies that over the last three years the People’s Bank of China has purchased about €270 billion, while Switzerland has done it for about €170 billion, somewhat less but fundamentally of a similar order of magnitude.

Table 2. Estimated reserves holdings in euros

Source: Swiss National Bank and People’s Bank of China Note: Data refer to July of each year.

The importance of the Swiss National Bank’s foreign currency interventions for the exchange rate of the euro can also be illustrated in the following way. The Swiss National Bank has intervened in the euro market to the tune of €173 billion over the last three years. If the ECB wanted to neutralise the impact on the euro’s exchange rate, it should have bought an equivalent amount of a foreign currency, say dollars. It is clear that if the ECB had bought $210 billion (€173 billion), the euro would presumably be much weaker today against the dollar. An intervention of the ECB of this scale would surely have been qualified as a real ‘currency war’ and would have led to significant conflicts among the major monetary powers. By contrast, the Swiss intervention caused barely a ripple.

The upshot is that over the last few years the Swiss National Bank has bought a large amount of euros to keep the Swiss franc artificially weak and since September 2011 it has set an official lower bound against the euro. However, this fact has attracted not even a cursory comment by policymakers anywhere whereas the Chinese interventions, which amounted to much less as a proportion of GDP (and which have stopped over the last 12 months) are almost universally condemned on both sides of the Atlantic. The differential treatment is even more surprising if one keeps in mind that Switzerland is running a current account equivalent to over 12% of GDP against less than 3% of GDP for China.

The Swiss Side of the Story

The official version of the Swiss story is simple. For over a decade the country had run large and rising current-account surpluses and kept a stable exchange rate (against the euro) without the need for any intervention, proving that these surpluses constituted market equilibrium. However, with the outbreak of the financial crisis ‘speculators’ started to consider the Swiss franc a safe haven, driving the currency to a level at which the Swiss export sector could not compete any longer. Under this view, the Swiss National Bank’s intervening heavily and then fixing the exchange rate against the euro was entirely justified.

However, this apologetic view does not take into account that the stability without intervention until 2008 was underpinned by a combination of factors that is unlikely to return i.e. Austrian local governments and households all over the new eastern member countries of the EU were willing to indebt themselves in Swiss francs because of its lower interest rates. Moreover, the global credit boom had made investment outside Switzerland appear as safe as a domestic investment. This illusion has now been shattered and private investors have understandably rushed to offload their exchange-rate risk on the Swiss National Bank. The official position is quite simple in its asymmetry.

Capital outflows are considered an equilibrium phenomenon during the upswing of a credit cycle, but capital inflows during the downswing are ‘speculative’ and must thus be neutralised.

The complaint that flows are ‘speculative’ and thus had to be countered does not ring true if one takes into account that even today the foreign-exchange reserves of the Swiss National Bank amount to ‘only’ two thirds of the sum of current account surpluses the country has accumulated over the last twenty years. It is also often argued that an excessive appreciation of the Swiss franc would damage export industries and tourism. Even leaving aside that Switzerland has one of the lowest unemployment rates in Europe, this argument does not make sense. It is clear that a decade of large current-account surpluses leads to an economic structure which cannot survive when capital flows turn around. An exchange-rate policy which seeks to cement an industrial structure which can survive only at an exchange rate which produces a double-digit current-account surplus is clearly beggar thy neighbour.

All in all it is clear that the actions of the Swiss National Bank to keep the Swiss franc low, and thus to perpetuate a current-account surplus of over 12% of GDP, have had a significant impact on the euro exchange rate and hence a non-negligible effect on the EZ economy.

The Swiss franc-euro exchange rate is important by itself given that exports of the EZ countries to Switzerland are about the same as exports to China (both around €90 billion in 2011). Moreover, the Swiss current-account surplus is relevant at the scale of the EZ, being equivalent to close to 1% of the EZ’s GDP, or the deficits of France and Italy combined. Switzerland’s peg to the euro has thus made the intra-EZ adjustment (elimination of current-account deficit in the south combined with lower surpluses in the North) significantly more difficult.

Moreover, most of the euro-denominated investments of the Swiss National Bank have presumably been in bank deposits and securities of the core countries. This means that its interventions have led to an even larger liquidity surplus within the German banking system and thus contributed materially to the huge claims accumulated by the Bundesbank within the TARGET 2 system.

Source

No comments:

Post a Comment